The scale of firm exposure to the coronavirus is unprecedented by earlier outbreaks, spans all major economies and is pervasive across all industries

When the World Health Organization declared the outbreak of the Covid-19 pandemic on March 11, 2020, the disease had already wreaked havoc in large swathes of China and in Northern Italy. At that point, 118,319 infections with the virus had been confirmed, and at least 4,292 people had died from the disease. What started as a new illness in a middling city in China had grown within a few months to a global public health crisis the likes of which had been unseen for a century. Stock markets around the world crashed. After an Oval Office address by US President Trump failed to calm markets on March 11, major stock indices fell another 10 percent on the following day. Even though governments rushed to stem the further spread of the virus, locking down entire regions and restricting (international) travel, and to support a suddenly wobbling economy, providing emergency relief measures and funding, it became quickly clear that the shock would leave few untouched. While the Covid-19 pandemic provides an extreme case, outbreaks of epidemic diseases are not without precedent in recent times and much can be learned about the resilience of the corporate sector from previous examples. However, given the extraordinary nature of the current crisis, these earlier experiences need to be carefully calibrated against the unique features of today’s challenge: existing models and policy remedies might no longer apply. In an effort to aid evidence-based policy responses, in our INET working paper we construct a time-varying, firm-level measure of exposure to epidemic diseases.

The measure we introduce is based on a general text-classification method and identifies the exposure of firms to an outbreak of an epidemic disease by counting the number of times the disease is mentioned in the quarterly earnings conference call that public listed firms host with financial analysts. Intuitively, the idea of constructing a measure of firm-level exposure to a particular shock from earnings call transcripts rests on the observation that these calls are a venue in which senior management has to respond directly to questions from market participants about the firm’s prospects. Not only are these disclosures therefore timely, but as they consist of a management presentation and, importantly, a Q&A session, they also require management to comment on matters they might not otherwise have voluntarily proffered. In most countries, earnings conference calls are held quarterly, which allows us to track changes in firm-level disease exposure over time. Indeed, we plan to continuously update our measures to reflect the impact of concurrent (Covid-19 related) events as they unfold. At the same time, we begin by using our approach to consider a given firm’s exposure to earlier significant epidemic diseases, namely SARS, MERS, H1N1, Ebola, and Zika. In addition to this exposure measure, we also construct measures of epidemic disease sentiment and risk. Doing so is important because it allows us to separate those firms which expect to gain from these events from those that expect to lose. While it might sound callous to talk about firms benefiting from a life-threatening disease as “winners,” we use these labels nevertheless for ease of exposition. Once we identify these winners and losers, we can then turn to the details of the conversation in their transcripts to systematically catalogue the reasons why they believe they can benefit from or are harmed by the outbreak.

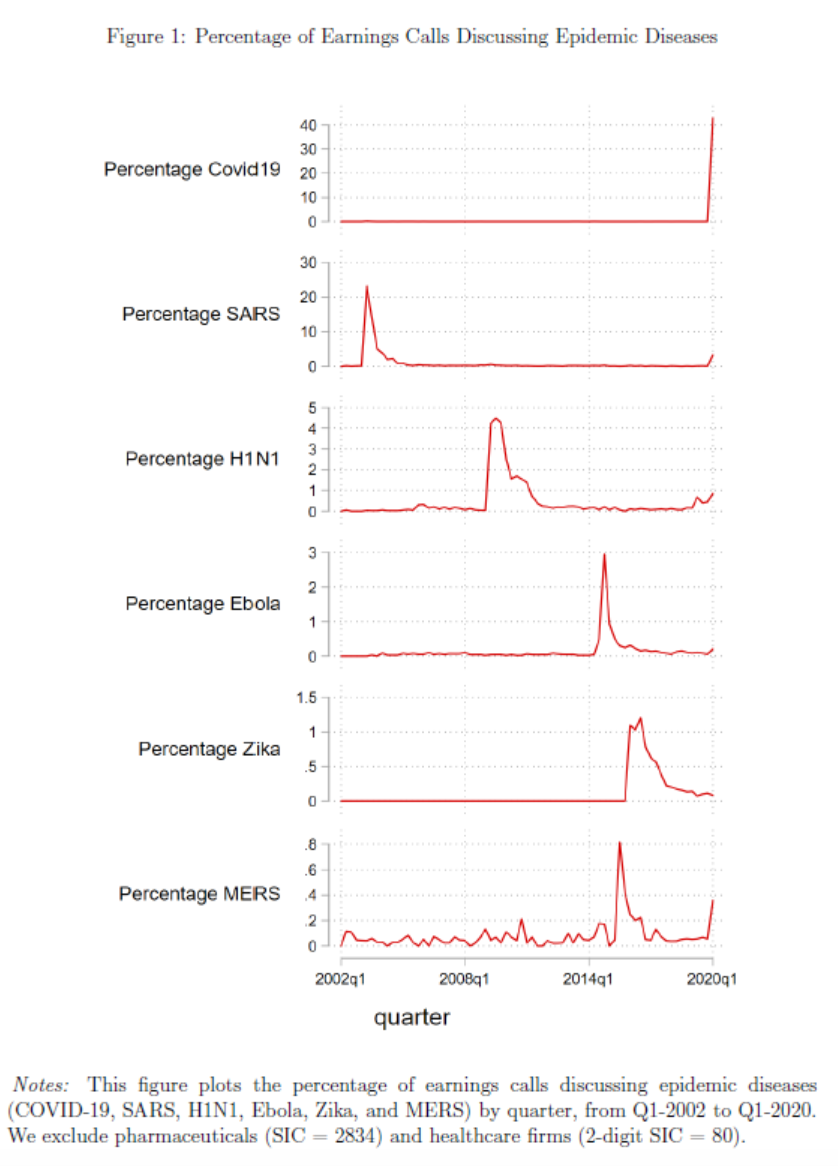

Having constructed these new firm-level epidemic disease exposure measures, we document a set of empirical findings for the impact of outbreaks on firms in 71 countries. We present findings that are not just of interest in their own right, but which also help to allay any potential concerns about the validity of our measures. For example, we show that the time-series pattern of exposure to certain diseases follows the infection rates in the population of these diseases, consistent with the idea that investors are most concerned about the firm’s exposure when an outbreak is most virulent. Figure 1 depicts the time-series of the percentage of transcripts in which a given disease is mentioned in a quarter separately for Covid-19, SARS, H1N1, Ebola, Zika, and MERS, respectively (moving from the top panel to the bottom).11 Reassuringly, these patterns closely follow the infection rates for each of the diseases in the population. For example, SARS, according to the WHO, was first recognized in February 2003 (although the outbreak was later traced back to November 2002), and the epidemic ended in July 2003. Accordingly, discussions of SARS in earnings conference calls peak in the first quarter of 2003 and quickly trail off after the epidemic ends. SARS, which is also a coronavirus disease, starts to become a subject in earnings calls again in the first quarter of 2020, when it becomes clear that Covid-19 shares much in common with the former outbreak.

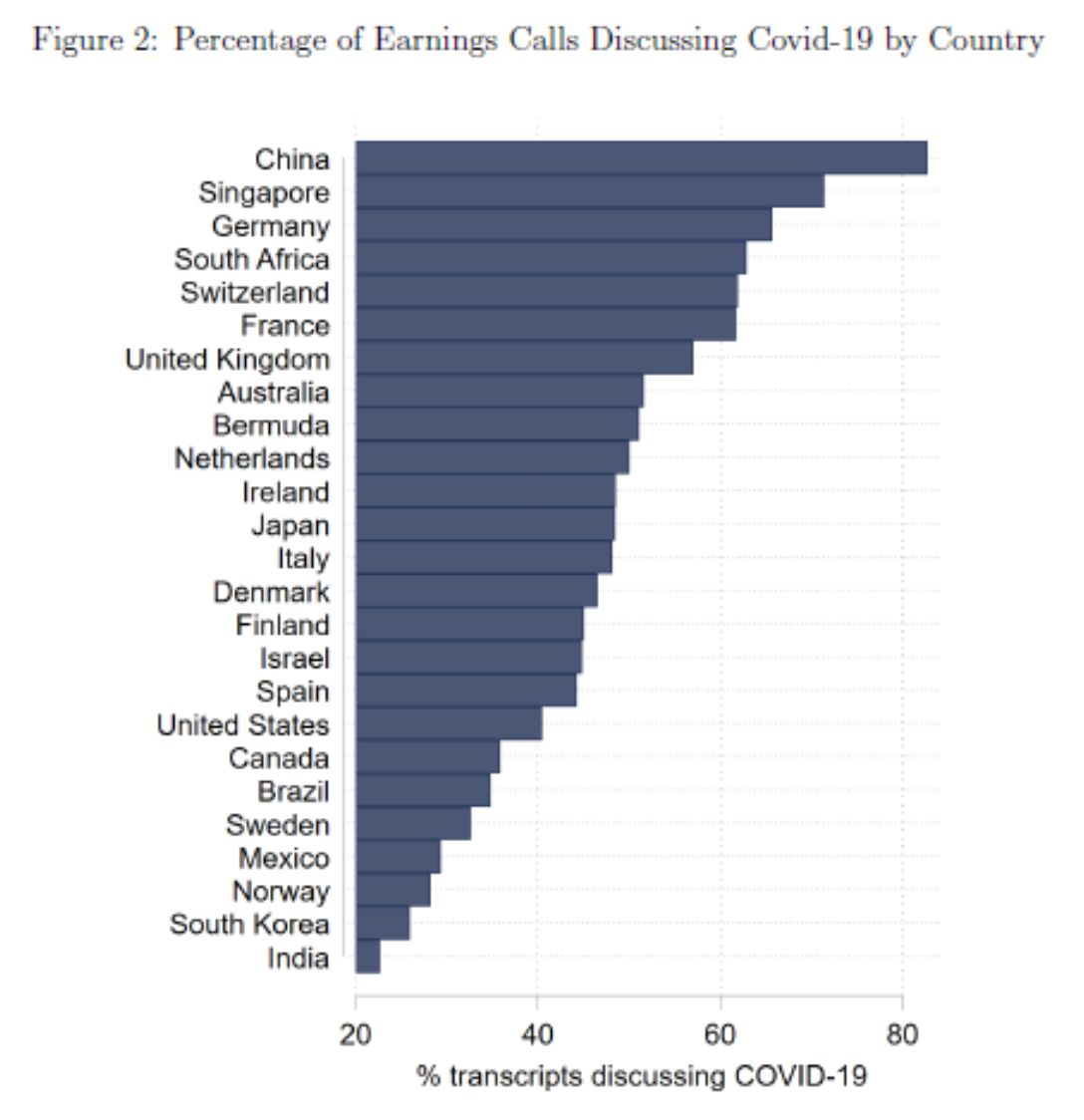

We not only document over-time patterns, but also show, by aggregating exposure scores geographically, how countries differ in the average impact of an outbreak. Figure 2 shows the percentage of transcripts by country in which Covid-19 is mentioned (provided that more than 25 transcripts are available for a given country). The figure excludes transcripts from firms in the healthcare industry and pharmaceuticals in an effort to highlight the country-level exposure in sectors other than health. Not surprisingly, China has the highest exposure (to date), with over 80 percent of the transcripts mentioning Covid-19; followed by Singapore and Germany. Perhaps more remarkable is the relatively low ranking of heavy-hit areas such as South Korea and Italy. About 40 percent of firms headquartered in the United States discuss the coronavirus in their earnings calls (again, this includes all earnings calls held through March 7, 2020).

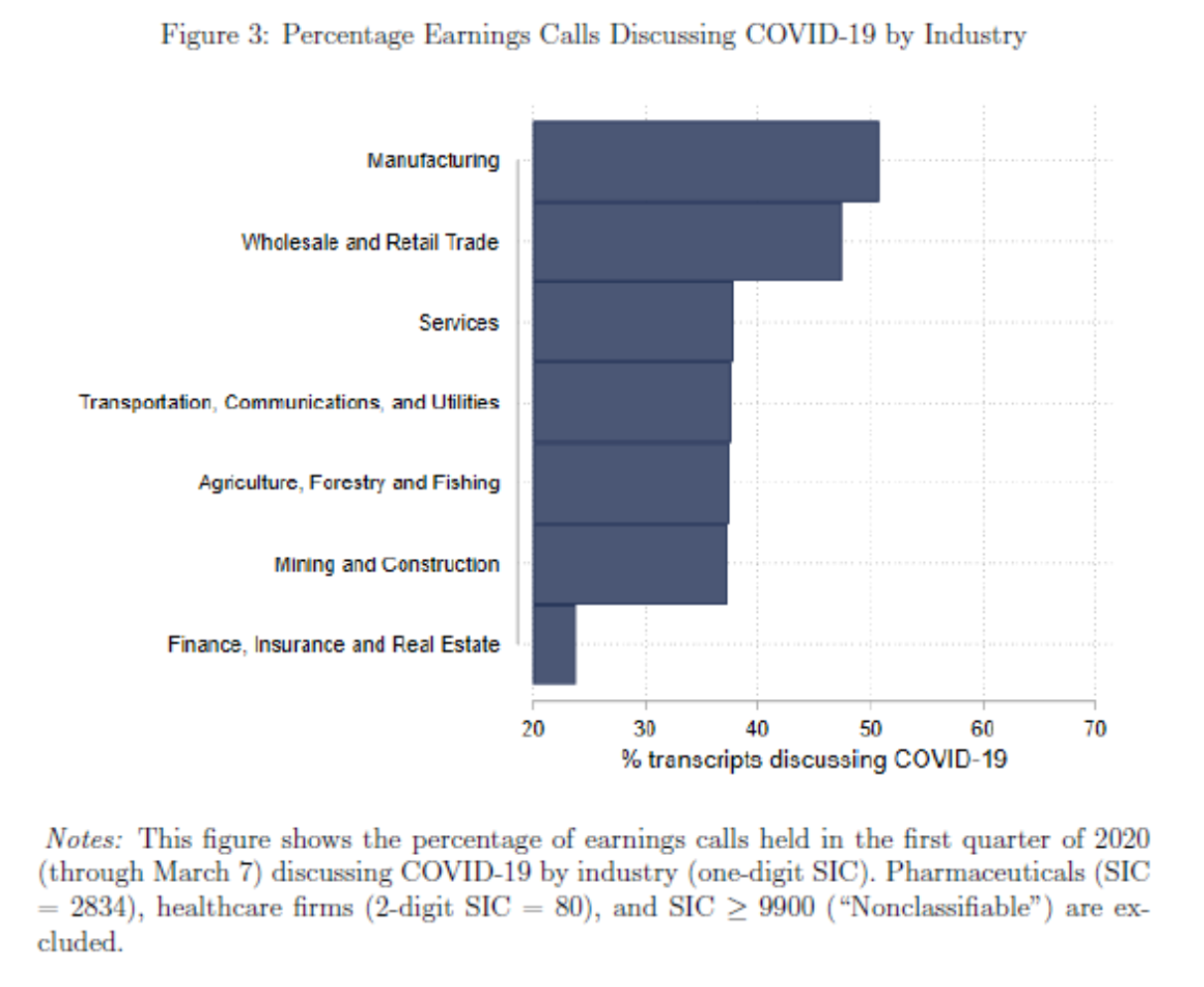

What is more, we show how sensitive different sectors in the economy are to epidemic diseases. The frequency of Covid-19 discussion in transcripts varies not only by country, but also by sector, as shown in Figure 3. One noteworthy finding, which is likely due to our sample period ending in the first week of March (i.e., before the extreme stock market volatility started), is that the Finance, Insurance and Real Estate sector has little discussion of the outbreak, whereas transcripts of earnings calls held by firms in the Manufacturing and the Wholesales and Retail trade sectors discuss Covid-19 in about half of the cases.

We then examine the resilience of the corporate world to the rise and spread of Covid-19. An emerging literature on the macroeconomic impact of pandemics emphasizes that the spread of the disease itself, and the policy responses attempting to mitigate it, may result in large shocks to supply, demand, and financing. At the firm level, these shocks may manifest in a variety of different ways. For example, the firm’s supply chain may be disrupted, it may suffer labor shortages, shutdowns of production facilities, a sudden drop in demand, or difficulty in accessing credit lines. We produce evidence on which of these potential concerns are current for firms around the globe during the coronavirus outbreak. Based on a detailed reading of the conversations in the transcripts, we document that concerns as of the first quarter in 2020 concentrate on (1) decreasing demand, (2) disruption of the supply chain and closure of production facilities, and (3) increased uncertainty. By contrast, as of the first quarter in 2020, relatively few firms appear concerned with their financing position. For a smaller subset of firms we find that they see opportunities arising from the disruption of competition in their markets. For this group of firms, the shock to demand can even be positive rather than negative, for example because they sell medical supplies or believe that the competitor’s brand is tainted by association with regions stricken by the virus. We also document the extent to which firms (especially early on in the pandemic) argue that their business is not affected by the disease. Having a deeper understanding of the various ways in which epidemics affect firms, is a sound starting point for developing effective government and/or corporate intervention policies. Clearly, supply-side disruptions should be met with a substantially different toolkit than is appropriate for demand-related shocks. We also show that firms which previously experienced an epidemic disease generally have higher (more positive) sentiment; i.e., their expectations about how the disease will affect their future cash flows are more positive than firms without such experience. These more optimistic expectations are also reflected in subsequent stock market tests. In these analyses, we show that short-window earnings-call returns, capturing the information released during the earnings call, as well as first-quarter cumulative returns, are generally lower for firms with higher measured exposure, negative sentiment, and risk related to the Covid-19 outbreak.

In sum, we provide novel data and first evidence on the extent to which epidemic diseases (and in particular the Covid-19 outbreak) affects the corporate world. The data show that the scale of exposure to the coronavirus is unprecedented by earlier outbreaks, spans all major economies and is pervasive across all industries. It also highlights the variety of issues firms and markets worry about amid the coronavirus outbreak; while uncertainty about the consequences of the outbreak is prevalent, it is foremost the firms’ expectations about reductions in future cash flows that catch the limelight in earnings calls and explain the stock market’s response