Modern Monetary Theory (MMT) became the macroeconomic topic du jour after it was invoked in support of a progressive stimulus package including, inter alia, a Green New Deal, elimination of college tuition, and Medicare For All. Whether such a package is feasible in macroeconomic terms is a question addressed below. First it makes sense to examine MMT as a doctrine, and then describe earlier macroeconomic shocks—the Great Recession and the Trump tax cut—as points of comparison to the stimulus.

Doctrine

Doctrinally, MMT is a tasty soup based on short-run demand-driven macroeconomic analysis blended with the Keynesian economist Abba Lerner’s “functional finance” (1943) and a legalistic German view of money from the early 20th century called Chartalism.[1] It says that money is legally a creature of the state, incorporating a modern central bank. The state can tax and spend to regulate employment generated by aggregate demand. It can create money by boosting spending or reducing taxes, or annihilate it by raising taxes or redeeming debt.

Money has taken many forms. MMT is one more member of the state-supported “fiat money” tribe. Its elder cousins included paper notes in 7th century China and 17th century Europe. Nowadays “money” is a number inhabiting a particular cell in a double entry macroeconomic spreadsheet for financial claims and counter-claims. It is created from “credit” whenever a bank or other financial institution makes a loan. MMT emphasizes state control over “narrow” money although it recognizes other channels for making payments. Money mostly comprises liabilities of banks and other financial institutions. The amount varies with the flux and reflux of credits extended.

Standard economics maintains an institutional distinction between the treasury and an “independent” central bank (at times folded de facto into the treasury as in the USA during WWII). The separation is blurred in much MMT discourse. A standard interpretation also emphasizes that the treasury issues bonds to finance an excess of expenditure over tax revenue. For the USA at least there is a huge market for treasury paper, in which the central bank intervenes to manage bond prices and therefore interest rates. Foreign and domestic investors each hold around 40% of American public debt. The Fed holds 15%. It can regulate interest rates because it is operating against a big buffer of privately held debt.

Doctrinal flavors aside, MMT is said to support the idea that within limits the Federal government together with the Federal Reserve can pursue expansionary policy without ill effects. But how big an expansion would result from a progressive stimulus package? Would the expansion provoke inflation? What about fiscal debt? Or foreign complications? It makes sense to work through the possibilities against the background of recent macroeconomic shocks.

Aggregate Demand

A useful way to think about fiscal expansion is in terms of “net borrowing,” or flows of investment minus saving for broad economic groupings such as the government, private, and foreign sectors. (The relevant flows for the latter are domestic exports minus imports). Thinking in terms of net borrowing or lending was promoted by the late British economist Wynne Godley. Despite their distaste for calling a fiscal deficit “borrowing,” MMT economists view Godley as a founding father.[2]

Macroeconomic accounting balance makes sure that the sum of borrowing levels across sectors must equal zero. If a sector’s net borrowing is greater than zero, it is contributing positively to aggregate demand. If its borrowing is negative, it is a net lender reducing aggregate demand. Changes in sectoral borrowings can shift the volume of economic activity.

A simple accounting scheme or toy model to determine real output X takes the form

(1) (I – sX) + (G – tX) + (E – mX) = 0

This equation says that demand “injections” minus “leakages” must sum to zero. Injections are real private investment I, government spending on consumption and capital formation G, and exports E. Leakages are private saving sX, fiscal receipts from taxes net of transfers tX, and import mX. As will be seen, the leakage rates s, t, and m may or may not be stable over time.

It is easy to solve (1) to get

(2) X = (I + G + E) / (s + t +m)

The leakage rates enter into a multiplier 1 / (s + t + m). Output emerges in (2) as total injections times the multiplier. Sectoral net borrowing shares of output are Bp = 1/X – s, Bg = G/X – t, and Bf = E/X – m. Equation (1) can be restated as

(3) Bp + Bg + Bf = 0

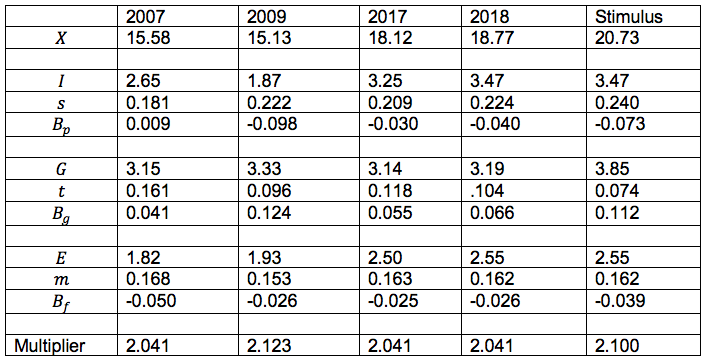

It makes sense to see how net borrowing fits into the US economy. Table 1 presents the numbers for 2007, 2009, 2017, and 2018. The level variables (output and injections) are in trillions of dollars in prices of 2012. Leakage rates and net borrowing shares are proportional to output as in the algebra just above.

Table 1: Net borrowing behavior in the USA for selected years and a progressive stimulus package (levels are in trillions of dollars at prices of 2012) Source: National income and product accounts and own calculation.

The first two years illustrate how changes in net borrowing affected the system during the Great Recession. The latter two show impacts of the Trump tax cut. Both episodes embody visible shocks to the system. A progressive stimulus package would be significantly stronger than Trump’s package.

The data show that the private sector swings between being a net borrower and lender. Its saving rate normally varies in the vicinity of 20%, and recently its level of investment has been comparable to government spending on goods and services. The government’s tax-minus-transfer coefficient has varied significantly, and it is a consistent net borrower. The import coefficient is around 15%. The external deficit or net lending from the rest of the world has been in the range of 2.5% of GDP recently.

Recession and the Trump Tax Cut

The 2007-09 recession was precipitated by private sector retrenchment in the wake of the financial crisis. Household consumption was flat, while investment fell by 30%. In turn, business retained earnings went up, meaning that the overall private saving rate rose from 18% to 22%. Output went down by 3%. It would have dropped much more if the net government tax rate had been stable. But in fact it fell from 16% to less than 10% due to automatic stabilizers (lower tax collections, and higher fiscal transfer payments built into existing practices) and the Obama stimulus package of around 5% of GDP. The overall impact was that private net borrowing fell by 10.7% of output while government borrowing went up by 8.3%. A smaller external deficit of 2.4% made up the difference. For reasons discussed below the fiscal deficit of 12.4% of GDP was probably unsustainable, but it dropped to around six percent by 2013.

In sum, the recession was not a disaster because of a major fiscal realignment. Causality ran from a private sector shock to a government response. It went the other way for the more modest Trump tax cut. The tax-minus-transfer rate fell from 11.8% to 10.4% of output, or about $250 billion. Output did go up by 3.5%, but the increase would have been greater if there had been a strong private sector investment boom instead of a smallish $220 billion increase. Lower business taxes were in part distributed via dividends and share buybacks to households at the top of the income ladder with high saving rates. In terms of demand leakages, higher private saving fully offset lower taxes.

Progressive Stimulus

During the 2007-09 recession a jump in private saving plus lower investment generated a contractionary shock amounting to 9% of GDP, or $1.4 trillion. In the opposite direction, a progressive stimulus package would generate a fiscal demand expansion. After guessing at the magnitude of a minimalist version in the “Stimulus” column of Table 1, we can consider possible consequences. Three of them—inflation, a rise in government debt, and foreign complications—could threaten the program. Known risks may not be extreme, but they certainly exist. (Of course, unknown unknowns can always arise.)

A very low-end estimate of the scale of interventions needed to mitigate global warming is two percent of GDP (Rezai, et. al. 2018). If in the USA that took the form of higher government spending then the 2018 level of G would rise from $3.19 in to $3.85 trillion dollars.

Medicare is basically a fiscal transfer program. Free college tuition could be another. If enhanced Medicare brings 20 million people into the health care system at $15,000 each, the cost would be about 1.5% of GDP. Reduced tuition might cost roughly the same. The total would be three percent of GDP.

Raising transfers by that amount would cut the 2018 tax rate (net of transfers) t from 10.4% to 7.4% of GDP. Offsetting factors which cut into an increase in demand should also be considered. Reductions in borrowing now paying for medical services and tuition could conceivably boost the private saving rate s from 22.4% to 24%.

Other things remaining equal, demand injections from the package would sum to $9.87 trillion dollars and the multiplier would be 2.1. The upshot would be an output level of $20.73 trillion dollars, an increase of 10.4% over 2018. Government net borrowing as a share of output would increase from 6.6% (post-Trump) to 11.2%, a fiscal deficit big enough to set off alarm bells. More government borrowing would have to be balanced by greater net lending of 7.3% of output from the private sector and 3.9% from abroad (a 50% increase in the external deficit). The expansionary shock would be close to five percent of output, not as large as in the 2007-09 recession but in the opposite direction.

In the short run, such a large demand surge by the government will not happen. One can ask, however, about possible effects of a big expansionary package on inflation, the fiscal position, and external balance.

Inflation

In macroeconomics the price level P, computed using an “appropriate” index, is the sum of labor and import costs multiplied by a mark-up or margin at rate M. For a large part of the economy the relationship of price to cost can be expressed as

(4) P = M(wl + em)

with w as the nominal or money wage, l the labor/output ratio (the inverse of labor productivity), e the exchange rate, and m the import coefficient used above. In the USA the mark-up rate M has been trending upward at 0.4% per year for 50 years (an overall increase of about 20%). Year-on-year, however, it is relatively stable. Some sectors (energy, agriculture, foreign transactions,….) may of course have volatile prices and margins, a complication discussed below.

Inflation is a dynamic process involving exponential growth of price and money wage levels. For it to occur there has to be positive feedback between the two. Suppose that over a period of months or a few years, real GDP (in prices of 2012) rises to $20.73 trillion due to higher demand as in Table 1. What would happen to P and w?

Much MMT discussion seems to say that they would enter into continued growth because output exceeds “full capacity.” The assertion makes no sense. An economy-wide upper bound on X does not exist. Even if it did, an increase in output to that level would make the price level jump to limit demand, but there would be no inflationary process. For inflation to kick in, the higher P would have to feed back into growth of w to set off price inflation from (4).

Besides full capacity, there are many rationales for an increase in P if X goes up. Three are worth mentioning. All require some sort of price-to-wage feedback to generate inflation, as discussed below.

One is based on the “Phillips curve” (1958), originally proposed as an empirical relationship between the growth rate of money wages and the unemployment rate. It is now more commonly applied to price inflation. A scatter plot of observed levels of unemployment on the horizontal axis and price inflation on the vertical gives a big blob of points. A regression line through them has a shallow negative slope—an increase of one percentage point in the unemployment rate maybe reduces the inflation rate by one-third of a point. The relationship may hold more tightly in recession when unemployment is rising, inflation is slowing, and the mark-up rate is tailing off. This scenario is not informative about impacts of expansion on rising wages and prices.

Second, an increase in the money supply may drive up the price level, an idea tracing back before the turn of the last century. The treasury/central bank can “print money” by emitting credit to buy goods, pushing up effective demand. If output is at full employment (Say’s Law applies), the price level will jump. The real wage w / P will be forced downward, restraining demand. If labor can push up the money wage in response, an inflationary process can get underway. The MMT emphasis on inflation at full capacity is not far from this proto-monetarist reasoning. [3]

Finally, the price of some key commodity could trend upward due to limited supply. The classic example is the price of food in Latin America (Sunkel, 1960). Energy could be a contemporary version (look at the gilets jaune movement in France). If other prices are stable, the real wage would fall, and could stoke inflation.

The key to all three models of inflation is social conflict. If labor can push up money wages in response to stagnant or lower real income, then inflation can take off. The question for the USA today is whether labor wields sufficient market power. The answer is that probably it does not. As already noted, the overall mark-up and the profit share of income have been moving upward for five decades, meaning that money wages have not kept up with prices. As a consequence, inflation has been slow. Under the circumstances, strongly expansionary policy might not run a big inflationary risk.

Debt

It is just an illustrative number, but in many circles, the 11.2% ratio of the fiscal deficit to GDP in Table 1 would be considered excessive. It would cumulate into debt. Whether the debt would be sustainable is the immediate question. Domar (1944) pioneered government deficit and debt accounting. There is a “Domar condition” for sustainability which states that the ratio of debt to GDP will not explode if the output growth rate (g) exceeds the real interest rate (j).[4] The “growth factor” g has to exceed the “leakage factor” j for the dynamics to be stable. Recently, the US growth rate has been in the vicinity of 2.5%. The real medium-term borrowing rate on Treasury securities is around 0.5% so the Domar condition is satisfied.[5] But there can be pretty rapid debt expansion involved.

In algebra, let δ be the ratio of fiscal debt to GDP. Its increase over time is

(5) d δ / dt = δ ̇ = Bg – (g – j) δ

The debt ratio is now around 1.05, up from 0.63 in 2007, in wake of the financial crisis.

With the current numbers,

δ ̇ = 0.112 – 0.02 x 1.05 ≈ 0.09

so the ratio is rising at 9% per year, fast enough to reach 1.6 in five years and 5.6 in the long run.

Just who is to absorb such rapid expansion of Treasury securities? As noted above, the Fed now holds only 15% of the total—private bondholders take up the rest. They would not tolerate nine percent growth indefinitely. Perhaps the Table 1 stimulus could be maintained for a few years, but it would sooner or later have to be dialed back. As the late conservative economist Herbert Stein once told Congress, “If something cannot go on forever, it will stop.”

It is also true that contemporary low interest rates are a consequence of low inflation. Greater labor militancy could drive up the inflation and real interest rates and cause the Domar inequality to be weakened or violated, with dire consequences.

External Balance

Somewhat similar considerations apply to the external deficit in Table 1 of 3.9% of GDP or $808 billion. Outstanding Treasury debt held abroad is $6.4 trillion. A potential run against the dollar could not change this total by very much because there is no alternative global asset. MMT emphasizes how the American economy is protected from shocks because it can borrow from the rest of the world in terms of its own currency.

This protection, however, is not invincible. A visible downward shift in demand for Treasury debt would have to be met in one of two ways (or a combination). If the interest rate is held constant, the exchange rate expressed as dollars per euro or renminbi would have to depreciate. The resulting jump in the price of imports could result in wage conflict and inflation. The US import coefficient is only 16%, but if prices of key consumer commodities were to jump upward, the impact could be significant.[6]

On the other hand, if the Fed intervened to stabilize the exchange rate, then the interest rate would have to increase to draw in foreign funds, potentially cutting effective demand. Either reaction would be a threat to the stimulus in Table 1.

Bottom Line

The program in Table 1 is at the low end of alternatives being discussed. It might be economically, if not politically, feasible in the short run. But it would amount to skating on thin ice—in several directions.

References

- Aukrust, Odd (1977) “Inflation in the Open Economy: A Norwegian Model,” Oslo: Statistisk Sentralbyrå

- Domar, Evsey D.(1944) “The ‘Burden of Debt’ and the National Income,” American Economic Review, 34: 798-827

- Lerner, Abba P. (1943) “Functional Finance and the Federal Debt,” Social Research, 10: 38-51

- Phillips, A. W. (1958) “The Relationship between Unemployment and the Rate of Change of Money Wages in the United Kingdom, 1861-1957,” Economica, 25: 283-289

- Rezai, Armon, Lance Taylor, and Duncan K. Foley (2018) “Economic Growth, Income Distribution, and Climate Change Ecological Economics, 146: 164-172

- Sunkel, Osvaldo (1960) “Inflation in Chile: An Unorthodox Approach,” International Economic Papers, 10: 107-131

- Taylor, Lance (2008) “A foxy hedgehog: Wynne Godley and macroeconomic modeling,” Cambridge Journal of Economics, 32: 639-663

- Taylor, Lance, and Özlem Ömer (2018) “Race to the Bottom: Low Productivity, Market Power, and Lagging Wages,” https://www.ineteconomics.org/uploads/papers/Lance-Taylor-Race-to-Bottom.pdf

Acknowledgements

Support from INET and comments (some contradicting the others) from Thomas Ferguson, Stephanie Kelton, Perry Mehrling, Mario Seccareccia, Servaas Storm, and Philip Pilkington are gratefully acknowledged.

Notes

- From the Latin word charta meaning paper. Paper money can represent debt.

- Godley’s ideas including net borrowing are reviewed in Taylor (2008).

- MMT literature at times argues that inflation could be attacked by raising taxes to cut into aggregate demand. Aside from practical difficulties (recall how hard it was for the Obama administration to get its stimulus package through Congress!) the tax increase would work against the rationale for the Table 1 stimulus.

- In fact, the condition was first noted in the 1950s by World Bank staffers applying Domar’s accounting.

- If under MMT rules fiscal policy is being used to regulate aggregate demand, then presumably the Fed could adjust the interest rate to assure that the Domar condition is well and truly satisfied.

- The Scandinavian inflation model (Aukrust,1977) was set up for an economy with a high productivity sector (in terms of both level and growth) and another with low productivity. The terms of trade would trend toward the latter. An inflationary shock, say from continued devaluation, in the former could generate price inflation between the two. A wage inflation response could then set off a cumulative process. The US economy can increasingly be described in terms of this model (Taylor and Ömer, 2018), but at the moment with weak labor power.