Wage Repression, Asset Price Inflation, and Structural Change Caused Rising Macroeconomic Inequality for Fifty Years from before Reagan through Trump.

This is a summary of a new book that is being published as part of a new book series with Cambridge University Press.

Over half a century – from before Reagan though Trump — American economic inequality worsened. Macroeconomic Inequality from Reagan to Trump (Taylor with Ömer, 2020) analyzes how and why. At least three macroeconomic developments mattered.

The principle driving force was wage repression. The share of primary income from production going to income from capital rose by eight percentage points. The bulk of this windfall went to the richest one percent of American households. Many more households, by contrast, are dependent on wages. With the wage share falling by eight points, the middle class was hit twice. At the top of the size distribution, the one percent raked in higher labor income, interest, dividends, business proprietors’ income, and capital gains created by corporate profits. At the bottom, low income households received stable wages if they were employed – a big “if” – and rising fiscal transfers. In terms of income shares, households in the middle got the squeeze.

On the side of wealth, capital gains due to rising asset prices are a major contributor to top incomes. High saving rates of prosperous households feed into more wealth. Capital gains expand in response to higher business profits and lower interest rates. Even with a rising profit share, wages still make up more than half of costs. Lower money wage growth means that current price inflation slows down. Driven in part by monetary policy, interest rates came down along with slow inflation, pushing up asset prices in tandem with higher profits.

A dual economic structure emerged, with jobs destroyed in manufacturing and other activities in which high wages combine with rising profits and productivity. More and more labor was shunted to low end occupations. Between 1990 and 2016, one-seventh of total employment moved into education and health, business services, accommodation and food, and other low paying sectors. In the 21st century, shares of Black and Hispanic workers in employment in these sectors were relatively high and growing steadily.

These trends resulted from the ways in which micro level changes interacted to produce macro outcomes. In his General Theory, Keynes (1936) recognized (without using the word) that macroeconomics “emerges” from that fact that all market transactions must net out across the system. Micro details – monopoly power, “superstar” firms, fissured labor markets, etc. etc. – all claim much attention by analysts convinced that one or the other is the real main cause of inequality, but none by themselves can determine macro outcomes. We look at examples below.

Distribution macroeconomics

Across business cycles, the share of profits in national income (profits plus wages) began to rise after 1970 at 0.4% per year. Four-tenths of a percent growth does not look very impressive but it increased the profit share by a factor of 1.2 or eight percentage points over 50 years.

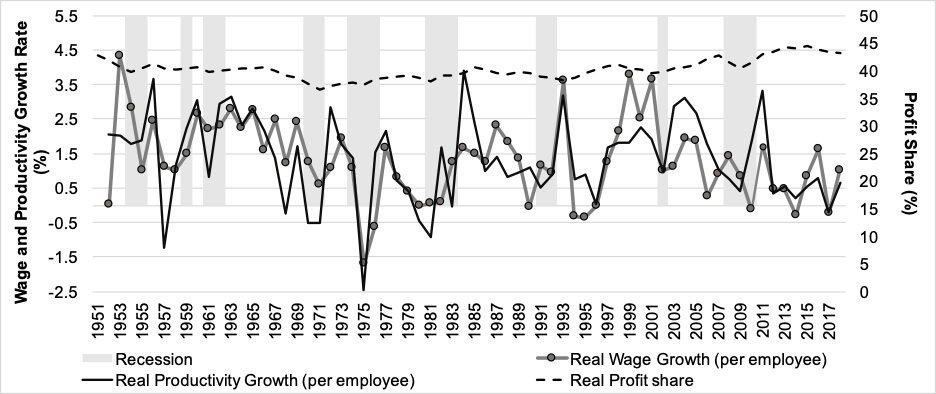

Figure 1 shows how the profit share and growth rates of real wages and labor productivity varied over time. After 1970, the bargaining power of workers fell off. From the side of labor, a dynamic process is involved. The real wage (money wage divided by a producer price index) grew less rapidly than productivity (real output divided by employment). Unless they increase over decades, micro interventions such as tax-transfer policies, minimum wage increases, etc. will not reverse this trend. The only way the wage share can recover fully is for the real wage to grow faster than productivity for a long time.

Functional distribution vs. size distribution

How does a big shift in the functional income distribution (that is, income paid as wages plus supplements, and non-wage income including corporate profits, proprietors’ incomes, and rents) map onto the disaggregated household size distribution? To trace the linkages, we constructed consistent accounting relationships between the well-known Congressional Budget Office (2018) data on levels and sources of incomes for seven household quantiles and the National Income and Product Accounts of the Bureau of Economic Analysis (themselves elaborate data constructions).

Figure 1: Real wage and productivity growth rates and profit share

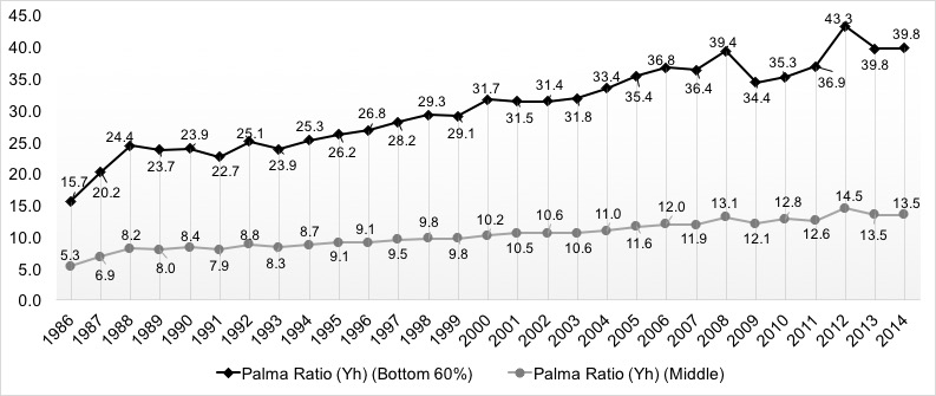

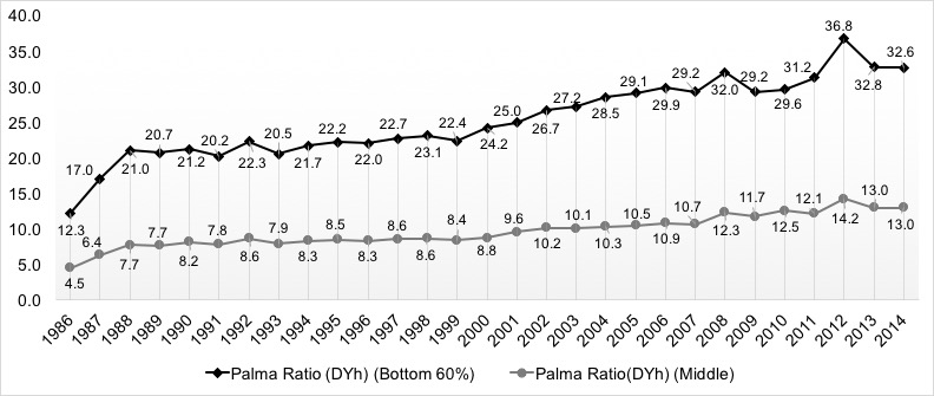

The CBO data can be aggregated into three income classes mentioned above, the top one percent, the bottom sixty percent, and a “middle class” in between. The Gini coefficient (the standard distribution metric) captures central tendency in the size distribution but is not sensitive to changes in the extremes. The “Palma Ratio” (2009) between income per household at the top vs. incomes of the two lower classes is more revealing. Beginning in the mid-1980s, growth rates of the Palmas were in the range of three percent per year – an astonishingly high number for any macroeconomic ratio over such a long period. Figure 2 shows the trends for both total and disposable incomes per household. The very high ratios at the end of the period did not materialize overnight. It took decades of unequal economic growth to make them appear.

Figure 2: Palma ratios for top 1% vs 61-99%-ile households and lower 60%

Based on total Income per household (Yh)

Based on disposable income per household (DYh)

Sources of top one percent incomes

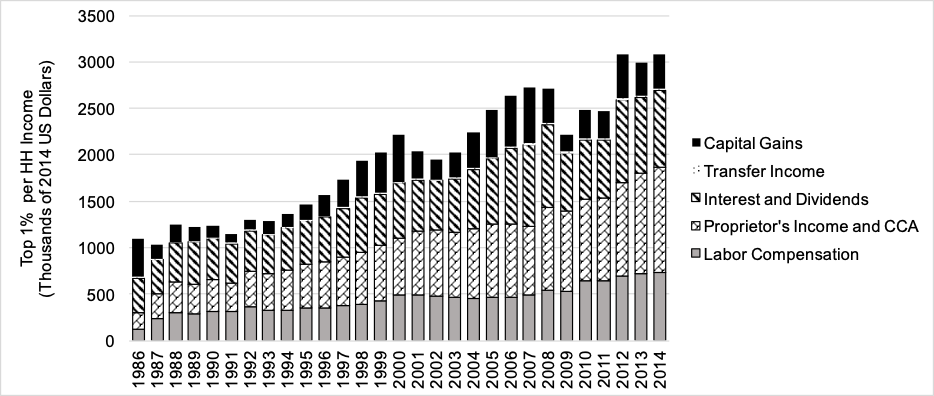

Surging non-wage income is striking for households in the top one percent. These people generate most personal saving and hold substantial wealth, including equity and real estate, which produce capital gains. Figure 3 shows how their average (mean) income along with its sources went up over time – late in the period rich households took in more than $2 million per year.[1]

Figure 3: Real per household incomes top 1% (2014 dollars)

The bottom segments of the bars show that they received substantial labor compensation. These payments include income from bonuses and stock options, which look more like payments to capital than labor. “Workers” such as executives at the top of large non-financial and financial corporations drive up the earnings numbers.

Average earnings are indeed large, ranging upwards of $500,000 per year at the end of the period. They more than doubled over a generation. On the other hand,

rich households take in only about seven percent of total labor income (four percent of GDP) economy-wide. Most of their money comes from other sources. “Proprietors’ incomes” along with rents and depreciation (capital consumption allowances or CCA, included for consistency with the double entry bookkeeping of the national accounts) exceeded labor income. Depending on the year in question, interest and dividends tended to be the same as or larger than earnings from employment. Capital gains on equity and real estate usually ranged in the hundreds of thousands per household per year.

A final striking feature of Figure 3 is that apart from the miniscule transfers, all forms of income received by rich households grew steadily over time. The steep slopes of the Palma Ratios in Figure 2 were supported by diverse streams of payments, which increased steadily. Reversing such trends will not be easy.

It is not quite accurate to call the top one percent “capitalists” or “rentiers” in the traditional senses of the words since so many do some form of “work,” but they are not far removed. Their rapid income growth mostly came from financial transfers and management, not from laboring on production or direct provision of useful services.

Middle class and low income households

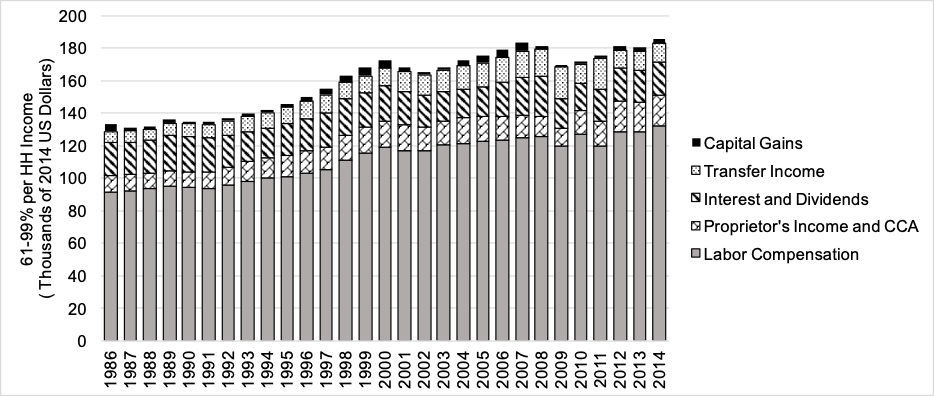

Simply put, members of the middle class look like “workers.” Their income sources are presented in Figure 4. Note the difference in the scales of the vertical axes

Figure 4: Real per household incomes 61-99%

in Figure 3 (zero to 3500 in thousands of 2014 US dollars) and Figure 4 (zero to 200 in the same units). The top one percent’s income is a factor of ten higher than the middle class’s. It simply does not compare with flows to the other 99% of households.

The bars show that labor compensation makes up almost 70% of middle incomes. In the USA, around seven percent of total compensation including direct payments and employer “contributions” to insurance and pension funds is immediately removed by taxes for Social Security and Medicare (flowing via FICA, Federal Insurance and Contributions) so the numbers are less rosy than they look.

The real mean pre-tax compensation average for middle class households increased from around $95,000 in 1986 to $130,000 in 2014 – a modest growth rate of one percent per year. Other significant, though secondary, middle class income sources are interest and dividends, and proprietors’ incomes. There are also government transfers. The main components are medical (Medicare, Medicaid, and other) at about six percent of GDP and Social Security (pensions and disability) at about five percent. Almost 60 other programs add up to another three percent. Total transfers exceed FICA taxes. As will be seen, the net income flow benefits the bottom sixty percent, not the middle class.

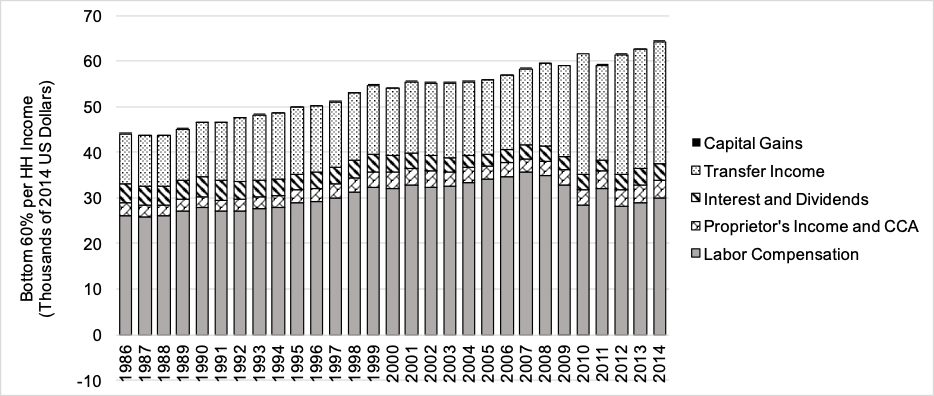

Households in the bottom 60% of the income distribution are far more dependent on government transfers, as shown in Figure 5. Even with $25,000 of transfer support coming in, relatively poor households had a mean income of $55,000 or one-third of the middle class level (as reflected in the different vertical scales of Figures 4 and 5). Despite increases during the period, real wages in 2014 were scarcely higher than in the mid-1980s. Annual wage income per household was around $30,000. Average hours worked per year in the US are around 1800,

Figure 5: Real per household incomes bottom 60%

so employed people in a household with two full-time earners were getting about $8.30 per hour before paying FICA. (The corresponding figure for the middle class is $30.40.) They received only a few thousand dollars in the form of financial, rental, and proprietors’ incomes.

Inflation and interest

Conflict between wages and profits was the main force driving rising income inequality. Via capital gains, wage repression also contributed to increasing concentration of wealth.

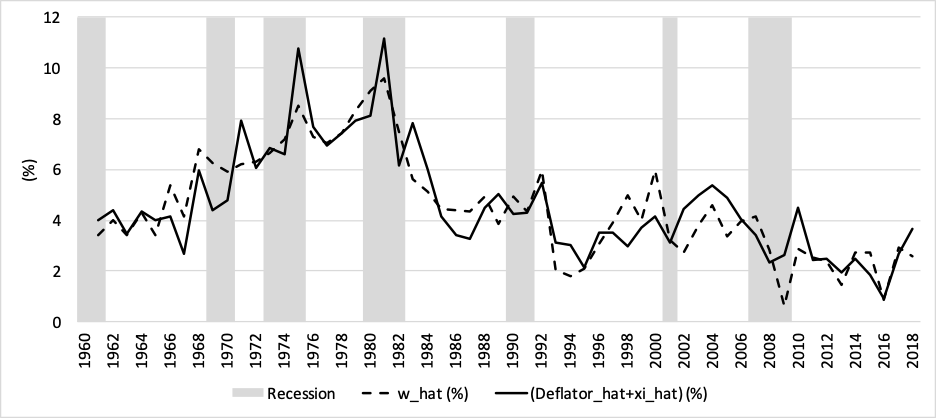

The long-term reduction in the wage share set up a slowdown in inflation across business cycles. The growth rate of the labor share can be expressed as the growth rate of the money wage minus the sum of the growth rates of price inflation and productivity. Figure 6 illustrates, using the GDP deflator as a broad price index. Typically, prices and productivity (solid line) have risen more rapidly than money wages (dashed), forcing down the wage share and raising the profit share in Figure 1.

Figure 6: Money wage growth vs. price growth plus productivity growth

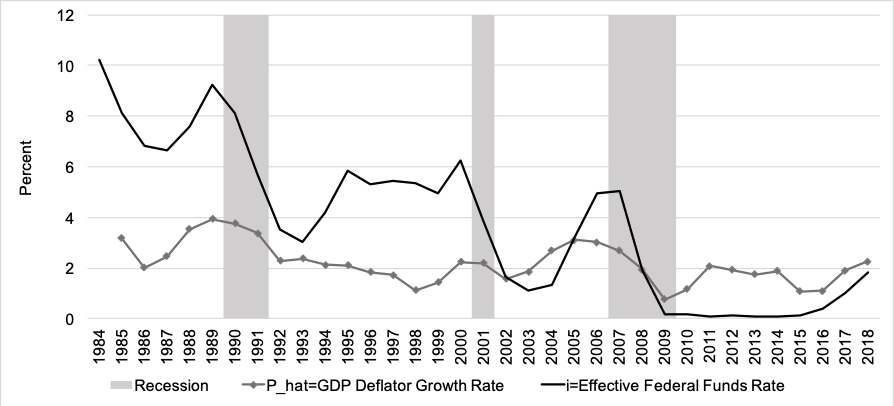

Figure 1 also shows that even though their share declined, wages still account for more than half the cost of producing GDP. As a consequence, the slow-down in money wage growth over time pulled down growth rate of the price level, from over ten percent in 1980 to around two percent now.

Since the mid-1980s slower inflation of prices of goods and services has been associated with a downward shift in interest rates, both nominal and “real” (that is, the nominal rate minus the rate of inflation). Figure 7 illustrates for inflation of the GDP deflator and the short-term interest rate controlled by the Federal Reserve.

Various explanations can be advanced for falling rates. One is that since 1987-2006 with Alan Greenspan as Governor, whenever there was a wobble in the stock market, the Fed consistently reduced rates to support prices of assets such as corporate shares and real estate. A complementary “rational actor” justification is that

Figure 7: Inflation vs. short-term Fed funds interest rate

quiescent inflation prompted bond-holders to accept lower returns. Whatever the reason, the mainstream “Fisher arbitrage” notion that the real interest rate should equal the corporate profit rate has not been observed – the former has dropped while the latter has gone up.

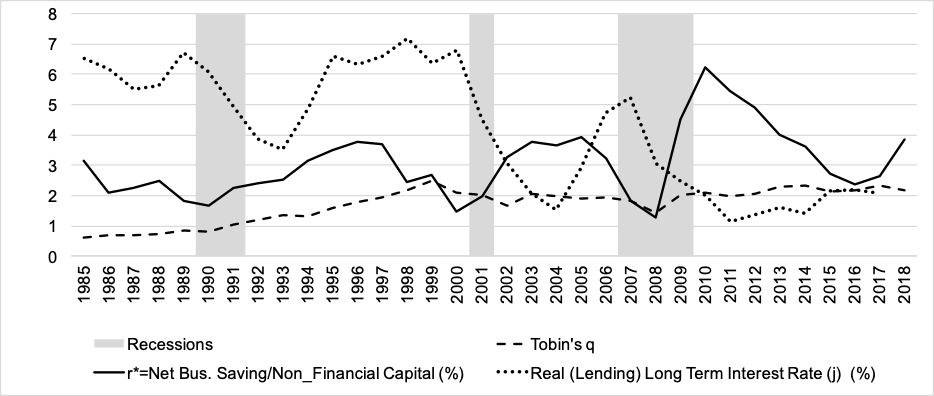

Interest and asset prices

The asset price connection is important for income distribution – rising prices or capital gains are important contributors to growing inequality. A useful metric is the valuation ratio or “Tobin’s q” (1969). At the macro level, it is defined as the ratio of the market value of corporate shares to the replacement value of the capital stock. In principle, q should follow from long-term relationships between profit and real interest rates. A quick and dirty approach called capitalization simply assumes that r* or the expected return per unit time generated by business capital (net of depreciation, taxes, and interest) will stay constant as will an “appropriate” real interest rate j (presumably provided by the market). High school algebra shows that r* discounted over time by j generates a value of the capital goods collection given by q = r* / j .

Until the 1980s, the levels of business fixed capital at current prices and the market value of corporate equities tracked fairly closely together, with equity a bit below capital. Since then, equities have risen sharply, with a couple of booms and crashes. The valuation ratio followed a similar pattern, rising from less than 0.5 in the 1970s to levels close to 2.0 in the late 1990s and 2010s.

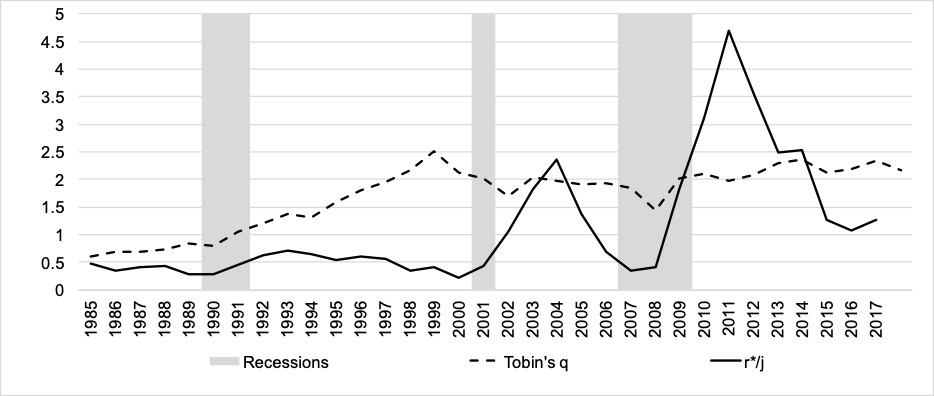

The upper chart in Figure 8 shows a decline in the real interest rate over nearly 35 years, accompanied by upward swings in the observed net profit rate. The lower chart compares observed q with r* / j. The fit is by no means perfect, but both variables show a clear upward drift, interrupted by recessions. Despite the rough-and-ready nature of capitalization and the vagaries of the stock market, it seems clear that growing profits and a falling interest rate contributed to rising asset prices. In the mainstream literature, Eggertsson et. al. (2019) throw around a lot of MIT or Caltech sophomore control theory math to arrive at much the same conclusion. They also recognize the wealth transfer from business to households discussed below, but they don’t take in the fact that these capital gains flow largely to the top one percent.

Figure 8: Net profit rate r*, real lending rate j, and Tobin’s q

Income, saving, and wealth

Tracing saving and investment flows helps clarify how rising profits and capital gains fit into accumulation of wealth. Investment is a key source of demand. Saving is the part of income that does not generate demand. When summed across sectors, the twain must be equal in macroeconomic balance.

In 2014, from the high to low income households, the three groups respectively saved 1.17, 0.68, and -0.93 trillion dollars, for a total of 0.92. In the data, total household saving is constrained by independent estimates of flows from business, government, and the rest of the world. Regardless of unrecorded transfers between the middle and poor classes which may help explain negative saving at the bottom, most household saving comes from the top one percent, adding to their accumulation of wealth.[2]

Total household capital formation (mostly residential) was 0.6, so their “net lending” (or saving minus investment) to the rest of the economy was 0.32. Similarly, levels of net lending by business (saving minus investment) and the rest of the world (exports minus imports) were 0.15 and 0.41 respectively. Unsurprisingly, government had negative net lending (positive borrowing) of -0.88 trillion, balancing the accounts.

There is another twist for the top one percent in comparison to business. For any group or sector holding physical and financial assets, the increase in their net worth is equal to saving minus depreciation (capital consumption allowance or CCA) of their physical assets plus capital gains on both.

The numbers for business are 2.42 of saving, and 1.78 of CCA so apparently the sector’s net worth should be increasing by 0.64 trillion. But look back at Figure 3. Toward the end of the period, roughly a million households in the top one percent were on average taking in about $400 thousand each in capital gains. The total was more than 0.4 trillion. That is, through “holding losses” on its outstanding shares (the Fed’s term in its data), business transferred a substantial portion of its growth in wealth to households in the form of “holding gains.” Figures 3-5 show that the recipients were mostly in the top one percent.

The takeaway from all this accounting is that households absorb almost all wealth accumulation, with the top one percent getting a big share of profits and the lower classes relying mostly on labor payments and fiscal transfers. Almost 60 years ago, these simplifying assumptions were built into economic growth models by Pasinetti (1962) and Meade (1964). One key conclusion is that the top group cannot control all wealth because they do not have full access to the non-profit income from which the middle class saves. Nevertheless, they can end up with a big share of net worth.[3]

Historically, the share in wealth of rich households was around 50% just prior to the Great Depression, fell to 25% in the 1960s, and is now in the vicinity of 35-40% (estimates vary). By around 1980 high New Deal taxes had been defanged and the stock market began the long upswing shown in Figure 8. Along with higher distributed profits these developments generated pleasantly rising net worth at the top while the rest of the population got left behind. Model simulations suggest that if there is no serious intervention the wealth share of the top one percent might rise to well over 50% in the not too distant future.

Pasinetti’s model also shows that Thomas Piketty’s (2014) famous “r > g” explanation for wealth inequality is an implication of proper macroeconomic accounting rather than some newly discovered fundamental law of capitalism.

Households with high incomes receive the bulk of profits, and have relatively high saving rates. To a good approximation the macro savings-investment balance takes the form

(Saving rate from profits) x (Ratio of profits to capital)

= (Ratio of investment to capital)

or

srr = g.

The ratio of investment to capital sets the growth rate of capital which on average will be the growth rate of output (the capital-output ratio is quite stable). Although it is high, the saving rate from profits is less than one. Hence the profit rate will exceed the investment rate over time.[4]

Sectoral structural change

In any economy, the structure of production across sectors changes over time. The traditional pattern in development economic “success stories” (say in East Asia) was for labor to move from low wage, low productivity “subsistence” activities in agriculture and elsewhere to high wage sectors with sustained productivity growth (Lewis, 1954). In this “dual economy” narrative, manufacturing is the salient leading sector. A striking feature of the American economy over at least the past quarter century is that this development pattern has run in reverse. On the whole, labor moved from high productivity sectors toward low end jobs. Meanwhile, profits rose in response to productivity growth in manufacturing, information, and a few other sectors.

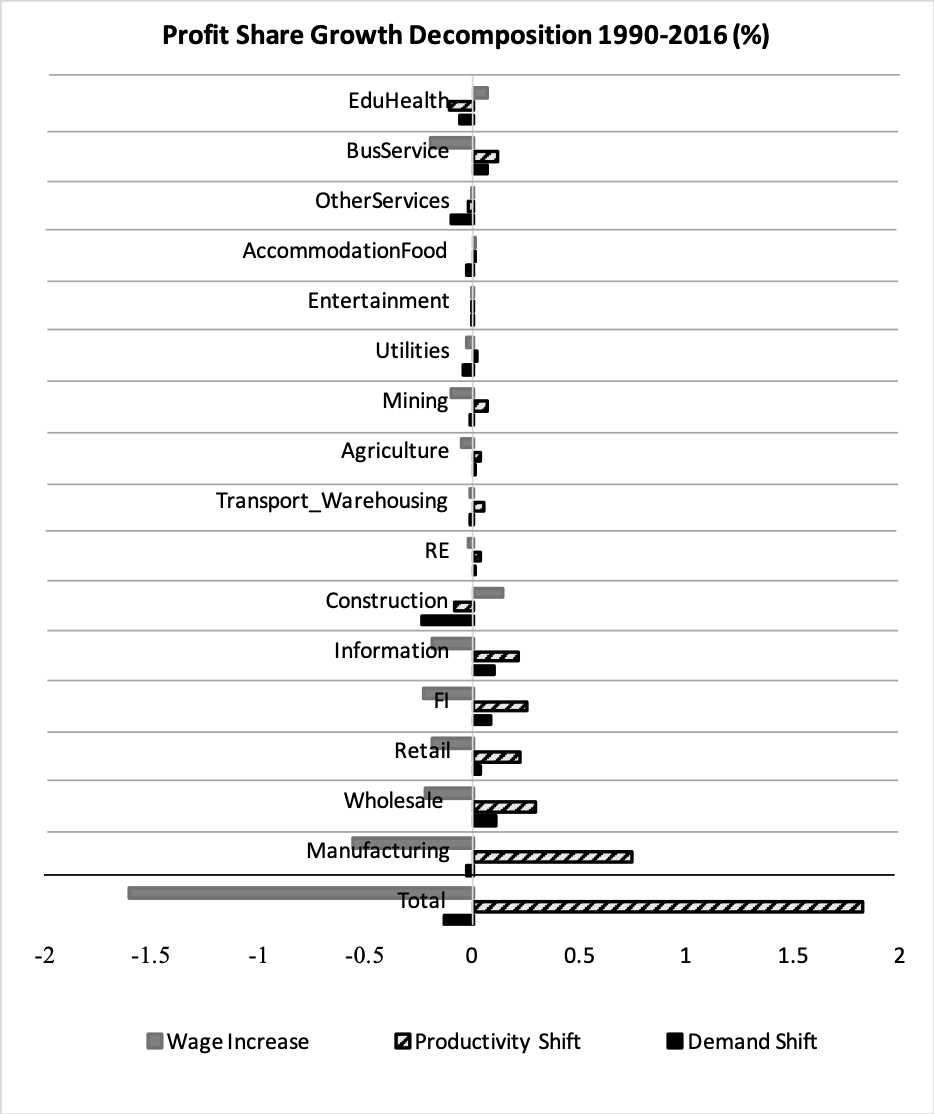

To begin with profits, the wage share increases with the real wage and decreases with productivity. Restating this linkage in terms of the profit share implies that it will increase with productivity and decrease with the real wage. Setting up this relationship in terms of rates of change of the relevant variables and working through the algebra across sectors shows that the growth rate of the overall profit share is a weighted average rising with sectoral productivity growth, falling with real wage growth, and also responding to shifts in sectoral shares of total real output. Figure 9 presents the results for 1990-2016.

At the bottom, the economy-wide increase in productivity outweighs real wage growth, generating the pattern in Figure 1. Sectoral effects of demand shifts were relatively minor, but they did stimulate profit growth in information, wholesale and retail trade, and finance-insurance. Along with manufacturing (strong productivity growth and visibly lagging wages), these sectors played the major roles in driving economy-wide profit increases. As demonstrated below, sectors contributing significantly to profit share growth also destroyed jobs.

Among minor contributions, construction suffered from a demand shift and falling productivity, but benefitted from falling real wages. Business services had relatively strong wage increases and also created jobs. Despite having high levels of profits and productivity the contribution of the real estate sector to profit share growth was negligible.

Figure 9: Profit share growth decomposition

Job growth can be analyzed in terms of the rate of change of the ratio of employment to the (economically active) population. It is easy to show that this ratio is equal to output per capita divided by labor productivity. Over time, its growth rate is a

weighted average of sectors’ growth rates of output minus their growth rates of productivity. The weights are sectoral employment shares. Figure 10 illustrates the

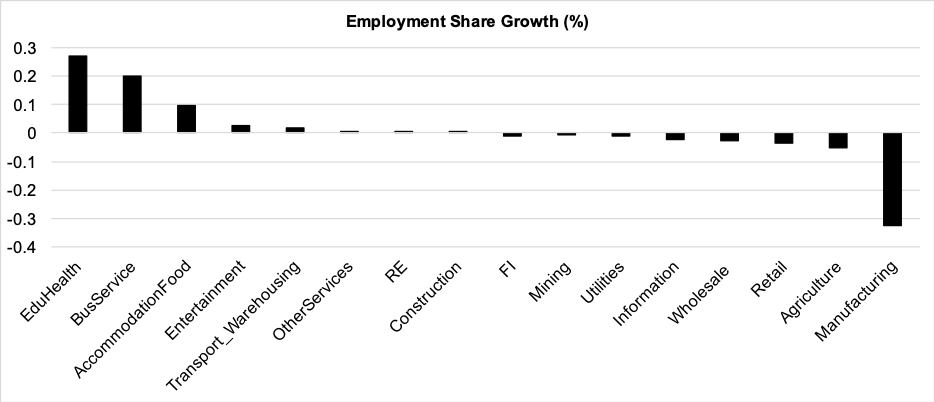

Figure 10: Employment share growth based on demand growth and Productivity growth

results of this decomposition. The bulk of job creation took place in seven sectors –education and health, business services, accommodation and food, entertainment, construction, other services, and transportation and warehousing. In increasing order, job annihilation took place in information, wholesale, retail, agriculture, and especially manufacturing.

In sum, “reverse Lewis” dynamics applies. Workers have been pushed into low wage, low productivity sectors, contributing to an overall productivity slowdown. Both static and dynamic sectors had lagging wage growth. Demand growth for manufacturing, information, and a few other dynamic sectors was offset by rising productivity so they shed labor although their wages are relatively high. Jobs trickled down to low-wage low-productivity education- health, business services, and accommodation-food sectors with rising demand but slow productivity growth. A natural interpretation along dual economy lines is that a productivity slowdown became a means to absorb surplus labor. Or, more baldly stated, business models adjusted to take advantage of ever growing masses of workers with no prospects for good jobs.

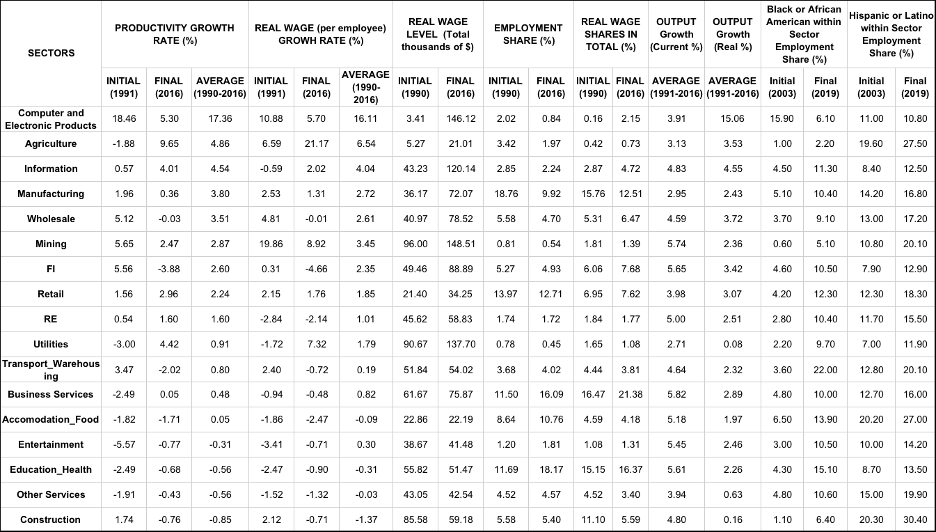

Table 1 summarizes the data underlying Figures 9 and 10, with the lagging sectors grouped toward the bottom. Besides the observations just made, the columns at the right show, unsurprisingly, that dualism is extensively racial. The share of Black employment in the total is 12.7%. The Hispanic/Latino share is 16.6%. Between 2003 and 2019, shares of the two groups in lagging sector employment grew rapidly. End-of-period sectoral shares generally exceeded the corresponding levels economy-wide. In sum, employment of the groups most subject to discrimination is skewed toward low wage/low productivity sectors (along with agriculture for Hispanics).

Structural inequality

This essay’s title is not facetious. The two Presidents mentioned – Reagan and Trump –- embody the breakdown of the New Deal’s social consensus. Wage repression, booming asset prices, and structural change have their entwined macroeconomic dynamics, supported by social forces that supplanted egalitarianism (even the mild American variety).

In part, these developments emerged macroeconomically. Reverse Lewis changes in the structure of production came from shifts in consumption patterns away from manufactures toward services, dynamics of productivity growth across sectors,

Table 1: Summary data for the sectors

and increasing business bargaining power in labor markets. Any individual asset price responds to profitability in relevant markets but is also driven by the economy-wide levels of interest rates determined by conscious Federal Reserve policy. Conflicts between labor and capital take place locally but add up across the whole economy. If labor mostly loses while rising profits are directed toward the top of the size distribution, the process has to be supported by institutions and financial policy pandering to the upper classes. It cannot possibly result from growth of monopoly in one or two sectors, such as the information sector.

Microeconomic details certainly matter but what matters for the whole economy is how they interact subject to market balance constraints.

References

Congressional Budget Office (2018) “The Distribution of Household Income, 2014” https://www.cbo.gov/publicatio…

Eggertsson, Gauti, Jacob A. Robbins, and Ella Getz Wold (2019), “Kaldor and Piketty’s Facts: The Rise of Monopoly Power in the United States,” https://www.nber.org/papers/w24287

Keynes, John Maynard (1936) The General Theory of Employment, Interest, and Money, London: Macmillan

Lewis, W. Arthur (1954) “Economic Development with Unlimited Supplies of Labor,” Manchester School, 22: 139-19.

Meade, James E. (1964) Efficiency, Equality, and the Ownership of Property, London: George Allen & Unwin

Palma, José Gabriel (2009) “The Revenge of the Market on the Rentiers: Why Neo-Liberal Reports of the End of History Turned Out to be Premature,” Cambridge Journal of Economics, 33: 829-869

Pasinetti, Luigi L. (1962) “Income Distribution and Rate of Profit in Relation to the Rate of Economic Growth, Review of Economic Studies, 29: 267-279

Piketty, Thomas (2014) Capital in the Twenty-First Century, Cambridge MA: Belknap Press

Taylor, Lance, Duncan K. Foley, and Armon Rezai (2019) “Demand Drives Growth All the Way,” Cambridge Journal of Economics, 43: 1333-1352

Taylor, Lance, with Özlem Ömer (2020) Macroeconomic Inequality from Reagan to Trump: Market Power, Wage Repression, Asset Price Inflation, and Industrial Decline, New York: Cambridge University Press

Tobin, James (1969) “A General Equilibrium Approach to Monetary Theory,” Journal of Money, Credit, and Banking, 1: 15-29

Notes

[1] The CBO distributional data only allow analysis of mean (“average”) incomes by group. Especially for the top one percent, the mean will exceed the median because the distribution within this group is skewed to the right or has a “fat tail” including billionaires at the far end of the curve. In other words, when Bill Gates walks into a bar, he brings the average income way up. But the income of the person who used to be exactly in the middle of the distribution doesn’t change; moving one step right or left won’t matter, either.

[2] Negative saving from the bottom deciles of the size distribution shows up consistently in consumer expenditure surveys of economies in the OECD. In part it represents unrecorded cash payments, perhaps 8-10% of GDP. If so, the payments are a transfer between income classes which do not affect overall household saving.

[3] The algebra is in Taylor, et. al. (2019) and Taylor (2020).

[4] Piketty justifies his result by assuming that a parameter called the elasticity of substitution in an aggregate production function is greater than one. A copious literature demonstrates that firm-level production relationships cannot be used to build up a macroeconomic aggregate function. Even if this spurious construct is accepted, most econometrics shows that the elasticity parameter is less than one. On both counts, Piketty is wrong.