Servaas Storm calls my narrative of the Eurozone Crises (EZ) which was published in VoxEU on 30 November 2015, “worrisome” for two reasons:

- “by focusing on the real economy (…) the financial sector disappears from the scene, (…) which means the real origins of the imbalances and the crisis are left undebated.”

- the “single-minded emphasis on the importance of relative unit labor cost competitiveness is misguided.”

The first point is obviously a misunderstanding. In my paper I have explicitly stated that the consensus narrative is correct, as far as it regards large intra-EZ capital flows that emerged in the decade before the crisis as the real culprits for the crisis. The intention of my paper is to emphasize that this narrative, while correct, is incomplete as it neglects the role of wage developments in the EZ.

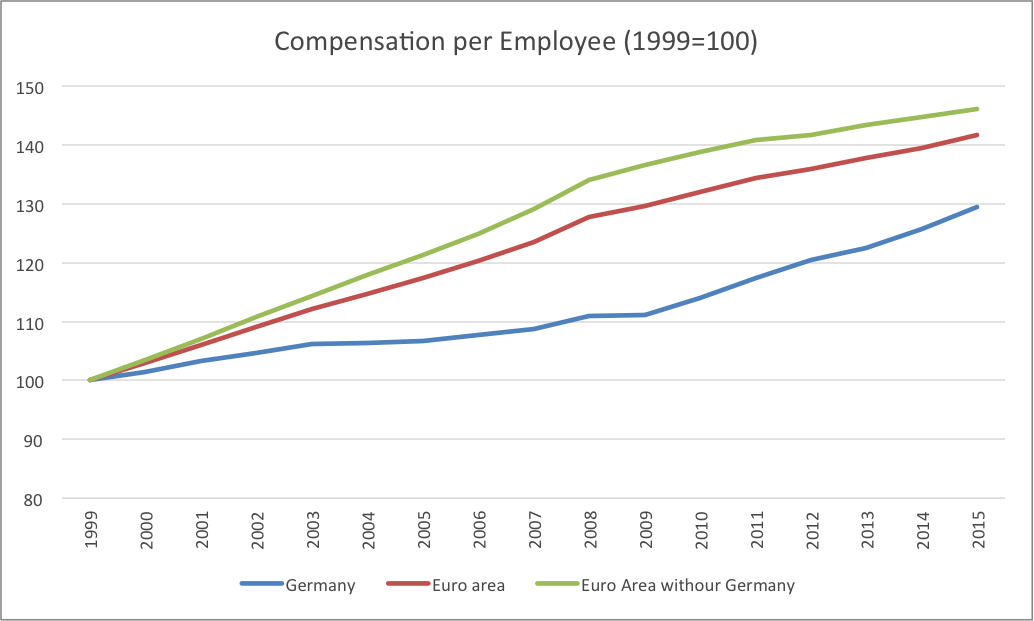

As far as the second point is concerned, Storm argues that “any talk of Germany deliberately undercutting its European neighbours is (…) beside the point.” This is an astonishing statement. “Wage moderation” is an important element of the narrative provided by most German economists explaining the successful economic performance of the German economy in the last decade. In fact, since the year 2000 the increase of the compensation per employee in Germany was much lower than in the rest of the EZ (Chart 1). The “nominal wage squeeze” which is disputed by Storm is rather obvious.

Chart 1: Compensation per employee (1999=100)

Source: OECD, Economic Outlook 98 Database

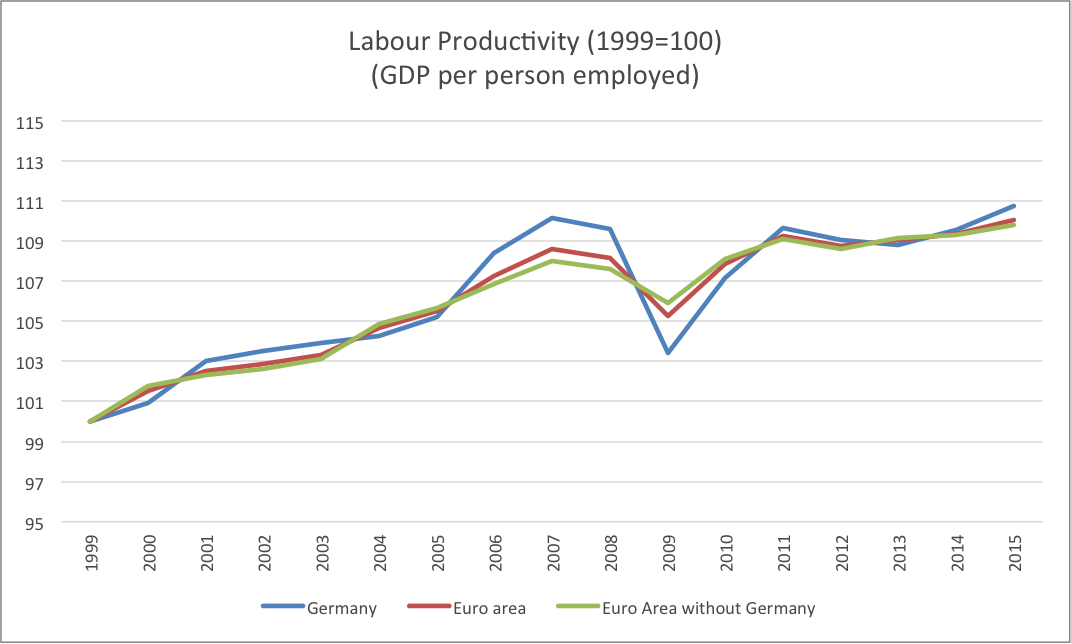

In contrast the “outstanding productivity performance”, which Storm also diagnoses, is not visible in the data. German labor productivity (GDP per person employed) was more or less in line with the developments in the rest of the EZ (Chart 2).

Chart 2: Labor productivity (1999=100)

Source: OECD, Economic Outlook 98 Database

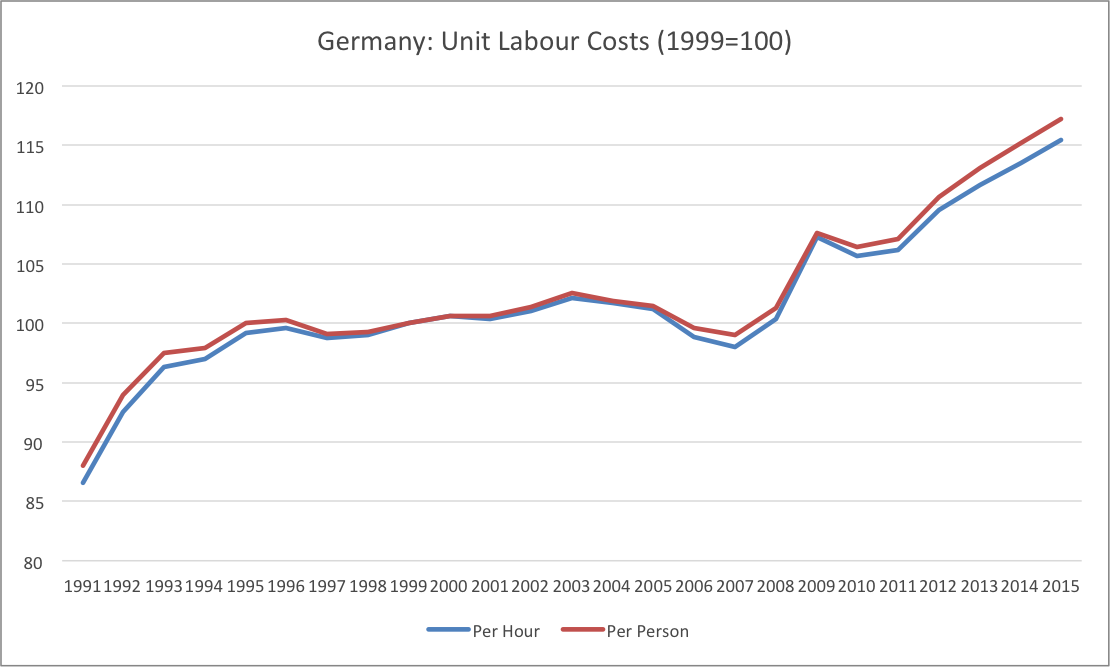

For this diagnosis the difference between unit labor costs per person and unit labor costs per hour makes no difference.

Chart 4: Germany: Unit Labor Costs (1999=100)

Source: Destatis

This does not mean that Germany’s export performance is solely driven by price competitiveness. Of course, non-price competitiveness also plays an important role. But low wage increases mean additional profits for successful firms, which allow them to improve their non-price competitiveness even further.

A narrative which emphasizes the role of price competiveness does also not imply that the current account deficits in Southern Europe were initially caused by this factor. The story of a “debt-led growth boom”, which then led to higher capital inflows leading only after a lag of many quarters to lower unemployment and higher wage growth in excess of labor productivity growth (Storm, 2016), is fully compatible with my narrative. Contradictions only arise if one tries to find a one-dimensional narrative. If one regards the EZ crisis as a multidimensional event, the debt led-boom and divergences in unit labor costs trends are not mutually exclusive.

This also applies to Storm’s analysis according to which:

“the role of German wage moderation is very different from conventional wisdom. It mattered a lot, not through its supposed impact on cost competitiveness, but via its negative impacts on demand or, more specifically, (wage-led) German growth and inflation, which in turn prompted the ECB to lower the interest rate excessively for the Eurozone as a whole.”

In fact, in my VoxEU contribution I made exactly this point. And again, one has to think in more than one dimension. German wage-moderation affected the EZ via two distinct channels: It made German exports more competitive, but at the same time it dampened domestic demand in Germany.

Finally, Storm argues:

” Confusing ‘simultaneity’ with ‘causality’, Bofinger then suggests that the higher corporate profits were used to finance the (net) outflow of German savings to the rest of world, as indicated by its current account surplus.”

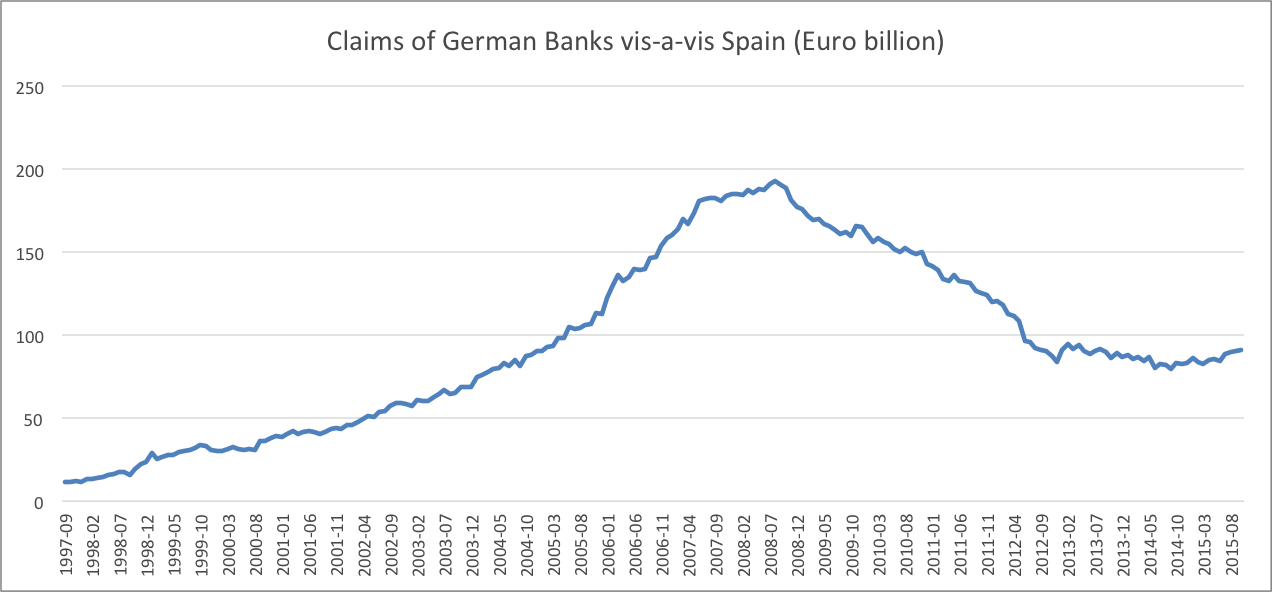

This is not my view and I did not make a statement along these lines. Higher profits were the result of the lower wages and strong exports to the rest of the EZ. They are by no means a vehicle to finance the surplus. The surplus was financed by the German banking system lending to Spanish or Irish banks (Chart 5).

Chart 5: Claims of German Banks vis-à-vis Spain

Source: Deutsche Bundesbank

But in spite of these differences, I fully agree with Storm’s final statement that “policies of internal devaluation” can be “self-destructive”. However, this does not mean that unit labor costs are irrelevant for the international division of labor. But based on the diagnosis of excessive German wage moderation the solution is a symmetric and not an asymmetric adjustment. It would imply, above all, increases of unit labor costs in Germany that exceed the ECB’s inflation target of “below, but close to 2%” for several years. Thus, all in all Storm’s criticism can be regarded as “friendly fire”.