Introduction

More than ten years have passed since the outbreak of the Great Financial Crisis. This shock should have led to a fundamental rethink in economics. But how little has changed is illustrated by N. Gregory Mankiw’s textbook on macroeconomics published in its 10th edition in 2019. For the presentation of the financial system, it still relies on the classical model for a corn economy. In the very first paragraph of the General Theory, Keynes criticizes this approach as follows:

“I shall argue that the postulates of the classical theory are applicable to a special case only and not to the general case. […] The characteristics of the special case assumed by the classical theory happen not to be those of the economic society in which we actually live, with the result that its teaching is misleading and disastrous if we attempt to apply it to the facts of experience.” (Keynes 1936, p. 3)

Mankiw’s textbook provides a perfect example of this critique. In the following, we discuss how the book describes the financial system. We use the presentation of “crowding out” to illustrate its economic policy implications. Finally, we discuss Mankiw’s model of the “small open economy.” It is flawed as the author tries to build a monetary superstructure on a model with no role for prices and money.

In line with Schumpeter (1954, p. 264), we will use the term “real analysis” for the classical model and “monetary analysis” for the Keynesian model (Bofinger 2020).

Mankiw’s presentation of the financial system

Mankiw (2019, p. 520) describes the functioning of the financial system with the so-called loanable funds model. It is the prototype of the “real analysis.” Its core assumption is an all-purpose good (APG), which can be used interchangeably as a consumption good, an investment good, and a financial asset. This critical assumption is not made explicit for the readers.

With the APG as the only financial asset, the saving of households provides the supply of “funds” on the capital market. If the households decide not to consume the APG, they make it available as a financial asset that can be supplied on the financial market and used as an investment good. Mankiw (2019, p. 520) describes the financial system as follows:

“The financial system is the term for institutions in the economy that facilitate the flow of funds between savers and investors.”

In this world, the role of financial intermediaries is limited. Banks and the capital market serve both as mere conduits for the transfer of “funds” from savers to investors.

“(…) a financial intermediary stands between the two sides of the market and helps move financial resources towards their best use. Commercial banks (…) take deposits from savers and use these deposits to make loans to those who have investment projects they need to finance.” (Mankiw 2019, p. 521)

This model world has nothing to with reality where “funds” are deposits held with banks (money stock M1). In the monetary analysis, which is represented by the IS/LM-model, the saving of households does not create funds. The decision of a household to consume less, e.g., not to buy a new laptop, increases the money stock of the household sector but decreases the money stock of the corporate sector. Thus, household saving redistributes the existing money stock. Accordingly, in the IS/LM-model, household saving affects the IS-curve (i.e.,, the goods market), but not the LM-curve (i.e., the financial market).

In the monetary analysis, new funds, i.e., bank deposits, are created by banks. Banks do not need to collect deposits for new loans. Instead, new loans create deposits. In this world, the capital market is different from banks as it redistributes the existing money stock between

- investors that want to exchange deposits for bonds, and

- investors with a demand for bank deposits to buy not only new but also existing real and financial assets.

The Bank of England has very well described the role of banks as originators of funds in 2014 (McLeay et al.). A modern macroeconomics textbook should not neglect these mechanisms.[1] Above all, the corn economy model is unable to discuss the excessive credit creation by banks that led to the Great Financial Crisis.

[1] Mankiw (2019, p. 91-93) gives a short presentation of the equally out-dated multiplier model. In this model, an autonomous credit creation of the banking system is possible if the central bank supplies the required reserves. But in Mankiw’s book, the source for the multiplier process is not reserves supplied by the central bank but households that deposit money with a bank.

Crowding-out in the world of real analysis

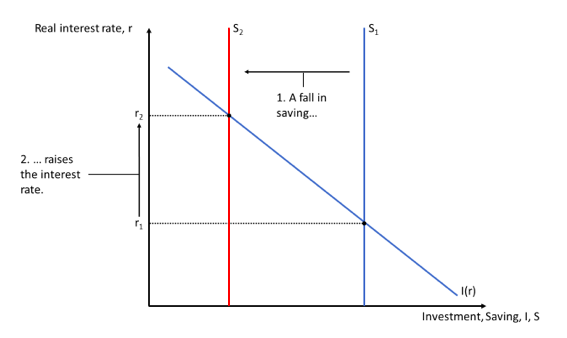

The presentation of the financial system as a corn economy has important implications for the discussion of macroeconomic policy. Mankiw (2019, p. 70) describes the effects of government deficits as follows (Figure 1):

If the government finances additional spending by borrowing, it reduces public saving. With private saving unchanged, the government deficit reduces national saving. The saving schedule in the saving-investment diagram shifts to the right. With an unchanged investment schedule, the interest rate rises, which crowds out private investment.

Figure 1: Crowding out Figure 3-8 in Mankiw 2019

The presentation raises the question of why additional government spending reduces public and national saving. E.g., if the government decides to run a deficit for investing in public buildings, its saving, i.e., the increase of its total net worth, remains unchanged. There is no shift of the S-curve. Mankiw is only right if the government uses the deficit for consumption.

The more fundamental problem is again the corn model of the financial system. In this model, with the decision of the government to borrow the APG, it is no longer available for private investment. Thus, government borrowing should be modeled as an increase in the demand for funds, not as a decline in the supply of funds. But independently of this, the interest rate increases, which leads to a financial and real crowding-out of private investors.

In the “monetary analysis,” the chain of effects is different. First of all, one must differentiate between the forms of financing. The government can borrow from the central bank, from commercial banks, and non-banks on the capital market. The corn economy does not require such differentiation, as banks and the capital market are unable to produce the AGP.

If the central bank finances the government directly by purchasing government bonds on the primary market, the government receives a credit on its account with the central bank. By making payments to non-banks, the bank deposits of non-banks increase. Thus, with the government deficit, the money stock M1 and the reserves of commercial banks increase. Instead of a financial crowding-out of private investors, additional more money is made available for investment in the capital market.

The effects are not different if the central bank follows the policy of “quantitative easing,” i.e. if it purchases of government bonds on the secondary market. E.g., in Japan for many years now, high government deficits go hand in hand with massive bond purchases by the Bank of Japan. When the government sells bonds to commercial banks, it receives bank deposits, and the money stock M1 increases. When the banks, in turn, sell the bonds to the central bank, their reserves increase.

If the government borrows from commercial banks, the money stock M1 also increases. Again no financial crowding-out takes place, as banks can create loans out of nothing. Capital regulations do not limit bank lending since banks do not have to maintain capital for government bonds and loans. While an increased money stock requires higher bank reserves, central banks typically control short-term interest rates and passively provide the necessary monetary base.

If the government borrows money from private investors on the capital market, it typically uses the funds immediately for payments to the private sector. Thus, the money stock of private non-banks is not reduced by government deficits. Government lending redistributes money within the private sector. While a quantitative “crowding out” does not take place, a qualitative crowdíng out cannot be ruled out. This is the case, if households or firms that receive payments from the government are not willing to lend these funds on the capital market.

Without a monetary analysis, it is not possible to explain why in Japan of very low interest rates go hand in hand with very high government deficits.

The confusing world of the small open economy

The presentation of the “small open economy” (SOE) in Chapter 6 is an example of Keynes’ statement that the teachings of the classical theory are “misleading and disastrous.”

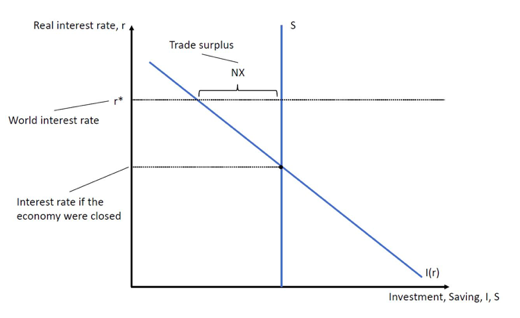

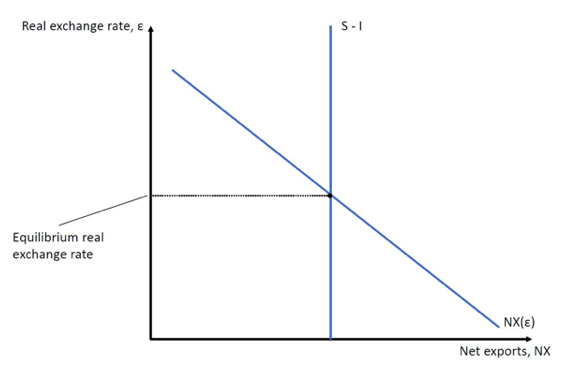

Again Mankiw does not make the critical assumption of the all-purpose good explicit.[1] He assumes that domestic saving is constant, i.e., independent of the real interest rate and the real exchange rate. The world real interest rate determines investment. Thus, depending on the world real interest rate, the SOE has a current account surplus (S>I) or a current account deficit (I>S) (Figure 1)

[1] This is different, e.g. in the textbook by Obstfeld and Rogoff (1996, p.1): “We assume throughout that only one good exists on each date, the better to focus attention on aggregate international resource flows without introducing considerations related to changing intratemporal prices.”

Figure 2: Saving and Investment in a Small Open Economy Figure 6-2 in Mankiw 2019

When the SOE is a net-exporter, the all-purpose good in its dual nature as a commodity and as “capital” flows from the SOE to the rest of the world (ROW). The model consistently describes the intertemporal and the international exchange for the all-purpose good. The real interest rate balances the global demand of and the supply for the APG.

Problems start when Mankiw tries to use the model for the determination of the real exchange rate. For this purpose, he introduces a monetary superstructure with an equation that explains net exports (NX) with the real exchange rate:

NX= NX (€).

This is surprising as NX is identical with S-I, which Mankiw explains in Figure 6-2 (here Figure 2) with the real interest rate. Thus in Figure 6-8 (here Figure 3), he presents

- NX aka S-I as a vertical line which is determined by the real interest rate and

- NX aka net exports as a downward sloping curve which is determined by the real exchange raze.

As a next step, Mankiw goes even further and describes

- NX aka S – I, as the net capital outflow and thus the supply of dollars to be exchanged into foreign currency and invested abroad, and

- NX aka net exports as the net demand for dollars coming from foreigners who want dollars to buy goods from this country.

With this stylized foreign exchange market Mankiw explains the determination of the real exchange rate of the SOE.

The attempt to create a monetary superstructure for a corn model creates severe inconsistencies:

- Net exports (NX) and S-I, which are identical by definition, are explained independently from each other by the real interest rate and the real exchange rate.

- In a model world with a single all-purpose good, there are no prices and no price level. The only price is the real interest rate. Therefore, one cannot define a real exchange rate (PS/P*) with P and P* being the price level and S the nominal exchange rate. And the real exchange rate cannot determine net exports.

- In a corn economy, there is no room for a foreign exchange market where money-stocks denominated in different currencies are traded. With only one all-purpose good, there are no dollar balances that could be exchanged into foreign currencies. The only international exchange is the intertemporal exchange of the APG.

Figure 3: How the real exchange rate is determined Figure 6-8 in Mankiw 2019

- Finally, it is not clear which country is represented by this SOE. Mankiw (2019, p. 141) defines the SOE as an economy, which is “a small part of the world market.” In this case, it is not clear why its capital exports are identical with a supply of dollars and why foreigners need dollars if they want to buy goods from the SOE. If one regards, e.g., Mexico, as the SOE and assumes that it has excess saving that it uses for capital exports to the United States, why should these funds be denominated in US-dollar? Furthermore, if US-citizens want to buy goods from Mexico, then why do they have to exchange “foreign currency” into US-dollars? The only way to avoid these inconsistencies is to assume that the United States is the SOE. In this case, the capital exports are in US-dollar, and the foreigners need dollars to buy US products.

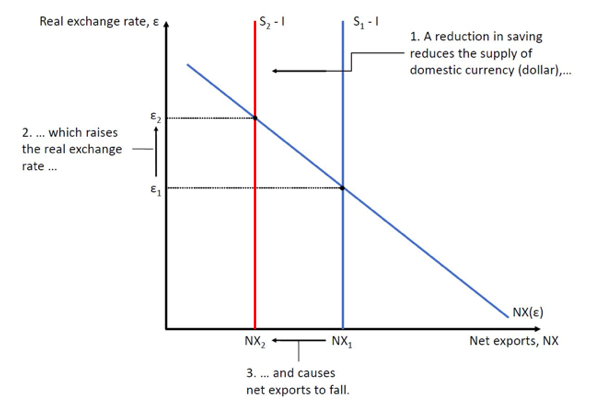

The problems of this approach become evident in the attempt to analyze the effects of an expansionary fiscal policy on the exchange rate. In Mankiw’s world, a fiscal deficit of the SOE reduces domestic saving, which shifts the S-I curve to the left (Figure 4). With a lower supply of the domestic currency (which according to Figure 3) is a supply of dollars, the real exchange rate of the SOE (the dollar) appreciates.

Figure 4: The impact of expansionary fiscal policy at home on the real exchange rate Figure 6-9 in Mankiw 2019

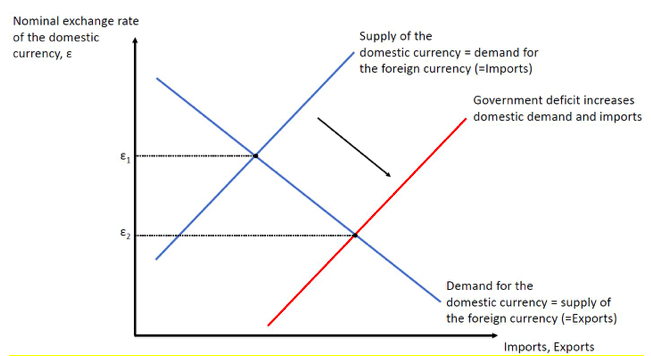

This outcome is not very plausible. Typically small economies that embark on an expansionary fiscal policy have to cope with a depreciating currency. In a world with money, the exchange rate of the SOE is determined as follows. The demand for domestic currency (in exchange for dollars) is downward sloping in a diagram with the nominal exchange rate of the domestic currency in quantity notation (Figure 4). The demand for domestic currency is identical to the exports of the country. The supply of the domestic currency (in exchange for dollars) is upward sloping and identical to the imports of the country. In this setting, a fiscal deficit leads to a higher domestic demand and – with a given propensity to import – to higher imports. Higher imports require a higher demand for dollars, which is identical to a higher supply of the domestic currency. The supply curve shifts downwards and causes a depreciation of the domestic currency.

Figure 5: The impact of expansionary fiscal policy in a world with money

In sum, the SOE model presented by Mankiw suffers from the attempt to create a monetary superstructure for a model world without money. In a corn economy, the world real interest rate perfectly organizes the international and intertemporal exchange of the APG. There is no room for the real exchange rate as a determinant of net exports.

In other words, Mankiw combines two incompatible settings:

- The intertemporal (and international) allocation of the all-purpose good by the real interest rate (real analysis) with

- the intratemporal allocation of commodities by the real exchange rate in a world with money (monetary analysis).

Summary

After more than a decade since the outbreak of the financial crisis, leading textbooks still present the financial system with the classical model of a corn economy. As Keynes realized already in 1936, such a model is unsuitable to describe the complex processes of the modern financial system. Mankiw’s Macroeconomics is a perfect example of the “misleading and disastrous” effects of teaching macroeconomics using the classical model. It is high time for a thorough reform of the macroeconomic curriculum, which has hardly changed for decades.

References

Bofinger, Peter (2020), Reviving Keynesianism: the modeling of the financial system makes the difference, Review of Keynesian Economics, Vol. 8 No. 1, Spring 2020, pp. 61–83

Keynes, J.M. (1936 [1973]), The General Theory of Employment, Interest and Money, in The Collected Writings of John Maynard Keynes, Vol. 7, London and Basingstoke, UK: Macmillan.

Mankiw, N. Gregory (2019), Macroeconomics, 10th edition, Worth Publishers, New York, NY.

McLeay, Michael, Amar Radia and Ryland Thoma (2014), Money creation in the modern economy, Bank of England, Quarterly Bulletin, Q1 2014, 14-27

Obstfeld, Maurice and Kenneth Rogoff (1996), Foundations of International Macroeconomics, The MIT Press, Cambridge, Massachusetts and London.

Schumpeter, Joseph A. (1954), History of economic analysis, Allen Unwin, London.