Author’s note: This post is largely based on part of a chapter in a forthcoming book in honor of Marc Lavoie and Mario Seccareccia, edited by Hassan Bougrine and Louis-Philippe Rochon.

The U.S. Federal Reserve’s low interest rate policy has not delivered the relief most borrowers had wished for, and conditions remain especially daunting for those that Keynes would call the “less powerful.”

To understand why, we need to look at the long-term consequences of monetary policies and regulatory decisions of the past, and to analyze the macroeconomic impact of the current structure of interest rates and its interaction with productivity and wages. What emerges is a cautionary tale that suggests we need to rethink the U.S.’ current economic policy approach—stepping away from interest rate interventionism and focusing instead on a range of more effective tools, from regulation to fiscal policy.

Who Gets Squeezed Last?

After the 1960s, fiscal policy became increasingly controversial in the U.S., subject to political battles in Congress and debates around welfare cuts. Monetary policy then emerged as the easiest and direct way to deal with pressing economic problems outside normal political channels. Prevailing economic theory supported that solution.

In the late 1970s, then-Fed president Paul Volker led a restrictive monetary policy conceived to break inflation, raising interest rates dramatically. That policy had one problem: It reduced the profitability of financial institutions lending to households, which were subject to nominal interest rate caps set by anti-usury laws, or whose business was limited to long-term fixed rate loans and mortgages, like the Savings and Loans industry.

This squeeze encouraged a series of reforms, which de facto abolished anti-usury laws, and allowed financial institutions to charge much higher interest rates (and fees).

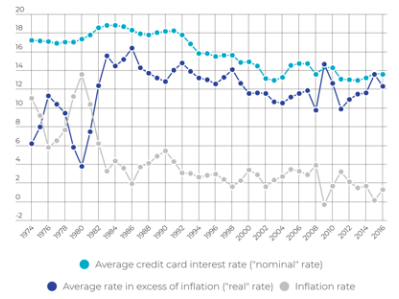

After the recession of 1990, Alan Greenspan’s Fed introduced a low interest rate policy, which continued throughout the early 2000s. But the growing cost of consumer credit, which had skyrocketed in the previous period, failed to reverse the trend once Fed Fund rates started falling (see figures 1 and 2).

As Keynes stated:

“Although it is easy for the central bank to raise the level of the complete vector of interest rates, it is much more difficult to get back to previous low levels, especially for long term-rates. In short, the upward trend cannot easily be reversed” (cited in Lavoie and Seccareccia 1988, 149).

Interestingly, today, short-term consumer rates, like credit card rates, are more rigid than long-term rates on, say, mortgages.

Moreover, with the new technologies available to companies for storing and analyzing data, the phenomenon affected households differently (Livshits et al. 2008, 16). In fact, applying different rates depending on credit scores, lenders could hedge off the losses from lending to low-quality borrowers, thus earning by reducing credit standards (Ellis 1998, and figure 1).

This adds an additional layer to what Keynes said about the asymmetric effects of monetary policy: “Restrictive monetary policy negatively affects mainly those that are not powerful, have not yet established long-term relations of confidence with bankers or happen to be in short-run liquidity squeeze rather than those who are inefficient producers” (cited in Lavoie and Seccareccia 1988, 149).

When the daunting conditions of debt became unbearable to many, and bankruptcy filings increased dramatically, the crisis inspired the 2005 bankruptcy reform, which represented a sharp change of direction from previous modifications (in 1978 and 1994), that had increased asset protection. To be fair, bankruptcy law in the U.S. remains more pro-debtor than that in most, if not all, other countries. Yet, it is curious that, just when the rules for the credit institutions and the market of new loans loosened dramatically, those for borrowers became stricter.

Figure 1 Credit card interest rate and inflation rate. Graphic from NerdWallet.com from Federal Reserve Statistical Release.

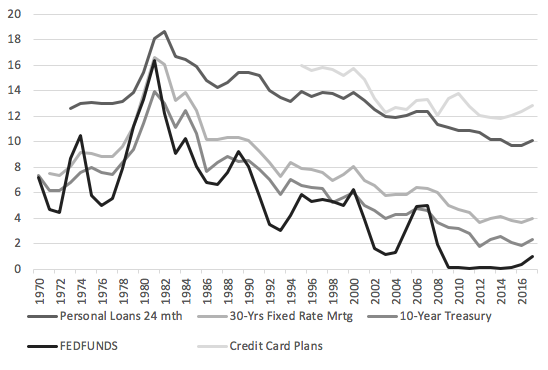

Figure 2 Interest rates. Fred series: TERMCBPER24NS, MORTGAGE30US, DGS10, FEDFUNDS, TERMCBCCALLNS

Consequences for Distribution

Interest rates have a direct and an indirect effect. The direct effect derives from interest payments being an actual transfer of income away from the non-financial (or active earning sector) to the financial sector. Indirectly, interest rates affect growth and distribution through their impact on investments and employment. In fact, while Keynes was skeptical about the positive influence of low interest rates on the inducement to invest, he was certain about the negative impact of high rates, which “put a brake” to investment and consumption, effectively putting a barrier to full employment. In addition to being harmful, they do not serve their assumed function well: they are not guaranteed to curb inflation, which to Keynes was a real and not a monetary phenomenon. Keynes recommended that rates should be set to a level compatible with full employment.

Following up on this recommendation and on the normative presupposition that interest rates should be neutral with regards to their broad impact on the distribution of income between interest income earners (or rentiers) and the rest of the economy, Luigi Pasinetti (1981, chapter 8) developed the idea that everybody who is involved in the credit market should obtain over time a constant amount of purchasing power in terms of labor (1981, 174). The idea is that the interest rate should compensate for changes in the purchasing power of a sum of money due to movements in prices and productivity. Lavoie and Seccareccia in 1999 dubbed the concept as a fair interest rate.

Since any deviation from it implies a transfer in favor of either lenders or borrowers, they also developed an index to allow for estimating the sign and size of those transfers over long periods of time.

This Pasinetti index compares real interest rates with productivity. When the gap between these two rates is positive, the index shows that the rentier sector obtained on average a transfer that was higher than their contribution to the economic system in terms of labor.

To obtain an aggregate estimate of the distributional consequences of any such deviation, we must apply some simplifying hypotheses. But the exercise can still provide an indication of how two factors contributed to the rentier share of income: the growth of productivity on the one hand, and the heterogeneity of interest rates associated with each sectors’ liabilities on the other.

In order to do so I compare an index constructed as the difference between productivity and a 10-years Treasury bill rate benchmark (Lavoie and Seccareccia 1988, Seccareccia and Lavoie 2016), and one that accounts for the outstanding debt of three sectors (government, households, and the non-financial corporate sector) and 5 types of liabilities (credit cards, personal loans, mortgages, corporate bonds, and treasury bills). The household sector of the economy has held the largest share of the liabilities between 2004 and 2011. In addition, figure 2 above shows that rates are normally much higher for short term personal loans than they are for other types of loans. Hence, we can anticipate that the household sector borrowing has contributed to turning the distribution in favor of the rentiers.

It is important to mention that the possible account for heterogeneity is limited due to data availability. Since I chose the interest rates charged to top quality borrowers, the weighted interest rate is underestimated.

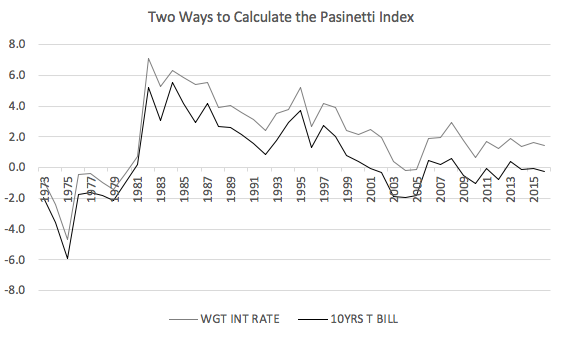

Based on this conservative calculation, the weighted Pasinetti index has been positive since 1981, with the exception of two years, 2004 and 2005. Comparing it to the benchmark index, in figure 4, we notice two things: first, since the turn of the 1980s the difference between the two became larger, with the weighted interest version being much higher than the other.

Second, the post-2008 period of low Federal Funds rates did not affect much the rentiers’ margin, except perhaps in 2010.

Figure 4 Pasinetti index with effective interest rate and with 10-years Treasury Bill

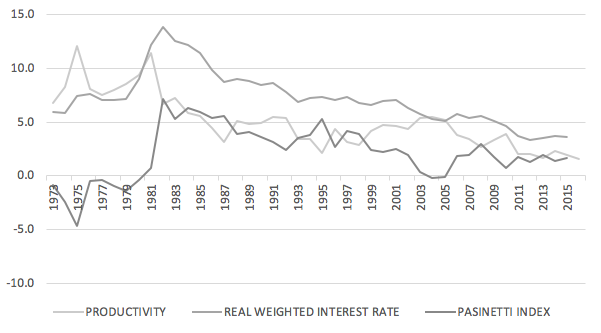

From figure 5, we see that in the early 1980s the rise of the rentier’s share was mostly due to the sudden extraordinary rise of the interest rates by Paul Volcker. At that time, the margins between Federal Fund rates and those on other loans fell, because of the different durations of the contracted loans and the legislative ceilings.

Figure 5 Pasinetti Index and components

Then, the interest rates kept dropping steadily after the 1980s, but not all of them at the same rate. We can see that, in many instances, rates tend to follow the hikes of the Fed Funds more than they accompany its descent. This is particularly true for the personal loans and credit card debt. In any case, since 1987, the effect of the fall in interest rates was offset by the fall in the productivity growth rate.

Optimal Policies

One of the staunchest opponents of rates fluctuation is John Smithin, who sees activism in that realm as detrimental to the economy and to the stability of the financial system (1994, 199, Rochon and Setterfield 2008). Interestingly, Smithin worries about high interest rates, but also against their sudden decreases, which would cause positive effects on the price of assets, favoring the rentiers and encouraging a financial bubble. The impact on liquidity preference and hence on the yield curve would be ambiguous, depending on expectations about the future; but the most likely outcome, in his view, is an inverted yield curve, deriving from the reluctance of rentiers to engage in long-term investments.

Sudden and prolonged low interest rates would also impact the balance sheets of banks which, depending on their portfolio composition, might suffer significant losses (for instance, if they hold large amounts of public debt). Insurance companies would see their earnings significantly squeezed.

In addition to Smithin’s list of perils, we should add the problems related to households, whose balance sheets have been very much affected by interest rates that tend—at least in the case of consumer credit—to be downwardly rigid but flexible upwards.

The “Smithin rule” is based on the idea of interest rates as a way to “preserve or enhance the value of accumulated financial capital.” Accordingly, Smithin suggests pursuing a policy of low but positive nominal rates—moderately favoring rentiers. The alternative, which would amount to a mere preservation of the financial capital, is to set real interests to zero, as suggested by Keynes (2003 [1936], 140).

Pasinetti’s fair interest rate has the clear advantage that it explicitly links rentiers’ income with production and employment. In fact, at any level of the real interest rate (with inflation being a monetary phenomenon), the share of income of the rentiers depends on the growth of labor productivity, which in turn depends on effective demand. If productivity growth were very low, as it is these days, regardless of rising inflation, interest rates should remain low too.

Yet an implementation of Pasinetti’s construction faces practical difficulties: for instance, inside the industrial sector we find many different levels of productivity and wages.

The Smithin rule, accompanied by a reinstatement of anti-usury laws, seems perhaps to be the most appropriate to apply. One could assign the task of influencing the distribution of income to other types of labor-market policies that would bring wage increases more closely in line with productivity growth, including stronger labor market regulations that increase the rigidity of wages and maintain their steady growth, such as a higher minimum wage policy, and tighter financial regulation.

Ellis, Diane (1998), “The Effect of Consumer Interest Rate Deregulation on Credit Card Volumes, Charge-Offs, and the Personal Bankruptcy Rate.” Federal Deposit Insurance Company, Bank Trends, No. 98-05

Keynes, John M. (2003[1936]), The General Theory of Employment, Interest and Money, The University of Adelaide Library Electronic Texts Collection: https://cas2.umkc.edu/economics/people/facultypages/kregel/courses/econ645/winter2011/generaltheory.pdf

Lavoie, Marc and Mario Seccareccia (1988), “Money, Interest and Rentiers: The Twilight of Rentier Capitalism in Keynes’s General Theory,” in Hamouda Omar and John N. Smithin (eds), Keynes and Public Policy after Fifty Years, Vol. 2, Aldershot, UK: Edward Elgar Publishing: pp. 145-58.

Lavoie, Marc and Mario Seccareccia (1999), “Fair Interest Rates,” in O’Hara Philip A. (ed.), Encyclopedia of Political Economy, Vol. 1, London/New York: Routledge: pp. 543-45.

Livshits, Igor, James MacGee and Michèle Tertilt (2008), “Costly Contracts and Consumer Credit” National Bureau of Economic Research NBER Working Papers 17448.

Pasinetti, Luigi L. (1981), Structural Change and Economic Growth, Cambridge: Cambridge University Press.

Rochon Louis-Philip and Marc Setterfield (2008), “The Political Economy of Interest-Rate Setting, Inflation, and Income Distribution,” International Journal of Political Economy, 37(2): 5-25.

Seccareccia, Mario and Marc Lavoie (2016), “Income Distribution, Rentiers, and Their Role in a Capitalist Economy” International Journal of Political Economy, 45(3), pp. 200-223.

Smithin, John (1994), Controversies in Monetary Economics: Ideas, Issues and Policy, Aldershot, UK and Brookfield, VT, USA: Edward Elgar.