Despite disparate policy beliefs, MMT and orthodox macro rely on many of the same theoretical foundations

An increasingly visible school of heterodox macroeconomics, Modern Monetary Theory (MMT), makes the case for functional finance—the view that governments should set their fiscal position at whatever level is consistent with price stability and full employment, regardless of current debt or deficits. Functional finance is widely understood, by both supporters and opponents, as a departure from orthodox macroeconomics. We argue that this perception is mistaken: While MMT’s policy proposals are unorthodox, the analysis underlying them is entirely orthodox. A central bank able to control domestic interest rates is a sufficient condition to allow a government to freely pursue countercyclical fiscal policy with no danger of a runaway increase in the debt ratio. The difference between MMT and orthodox policy can be thought of as a different assignment of the two instruments of fiscal position and interest rate to the two targets of price stability and debt stability. As such, the debate between them hinges not on any fundamental difference of analysis, but rather on different practical judgements—in particular what kinds of errors are most likely from policymakers.

Anyone who has followed debates on macroeconomic policy in recent years will be familiar with Modern Monetary Theory (MMT). While MMT is an evolving school of thought that combines a number of distinct elements, its most visible claim is that for the United States federal government (and others similarly situated), there is no financial constraint on fiscal policy. If a government seeks to adjust the budget position to bring output to potential, it can do so regardless of the current budget deficit, debt-GDP ratio, or similar measures of fiscal space. The goal of this short paper, by a pair of economists who are outside of but sympathetic to MMT, is to clarify where its analysis of fiscal policy departs from the views of the majority of macroeconomists and where it overlaps with with them.

Modern Monetary Theory is perceived, both by outsiders and many of its adherents, as a radical departure from the views held by most policymakers and academic economists. Its policy argument is supposed to rest on a distinct and different understanding of the financial system and macroeconomy—a perception reinforced by the tendency of many MMT texts to begin with a historical account of the development of money, the mechanics of fiscal operations, and so on. We believe that this perception is mistaken. The economic analysis behind MMT’s fiscal-policy argument is essentially the same as that used by orthodox policymakers and in undergraduate textbooks. The different conclusions drawn by MMT and the mainstream in policy do not come from a different understanding of the economy, but from a different view of the capacities of policymakers, and in particular, of what kinds of policy errors are likely to be most costly. More precisely, the difference between MMT and the mainstream should be seen as a different view of the preferred assignment of policy instruments to policy targets.

To be clear, MMT does not constitute a settled body of thought with fixed premises and conclusions, nor of course does “mainstream” macroeconomics. Recent incarnations of MMT pool several distinct elements—a theory of money (what could be called neo-chartalism), a discussion of current monetary operations, a political program (typically a job guarantee), an exercise in national income accounting (sectoral balances) and a program for macroeconomic policy. For many of its supporters these elements cohere together in a broader vision; but it is logically possible, and useful, to distinguish them. Here we are interested in the macroeconomic policy component: the argument that fiscal policy can and should be used to close an output gap regardless of the current debt-GDP ratio and fiscal position. Following Abba Lerner’s influential formulation, this component is often referred to as functional finance (Lerner 1943). Our goal here is not to make an assessment of MMT as a whole, but to ask what is the relationship between the functional finance approach to government budgets and conventional economic analysis. Because we are interested in the logic of the functional-finance position rather than in MMT as a body of thought, we make only limited references to MMT literature here.1 Our primary interest is in the merits of the functional finance position in the abstract. On the mainstream side, we are focused on what might be called “orthodox policy macroeconomics”—the practical heuristics that guide policy makers and are reflected in undergraduate textbooks, as opposed to DSGE and related models of intertemporal optimization that are the basis of most current macroeconomic theory. The relevant question is not whether MMT is consistent with models of this type, but whether it is consistent with the simpler, more reduced form models that are (explicitly or implicitly) drawn on by public officials and public and private-sector forecasters, as well as by academic economists when engaged in public discussions.2 On both sides, in other words, we are interested in the logic of the policy positions themselves.

Both orthodox policy macroeconomics and functional finance start from the same key assumptions:

1. In the short run, output is determined by the total desired spending of units in the economy (aggregate demand).

2. In the short run, unemployment is a decreasing function of the level of output, and inflation is an increasing function of the level of output.

3. There is a level of output such that the behavior of both inflation and unemployment is acceptable. We can describe this equivalently as output at potential, full employment or price stability. Output below this level implies unacceptably high unemployment and perhaps deflation; output above this level implies unacceptably high and/or rising inflation. This assumption can be represented as a Phillips curve, the same general form of which is used by MMT as in conventional textbook presentations. A corollary is that policy affects inflation only via the level of output.3

4. Economy-wide spending (aggregate demand) depends on, among other things, the interest rate set by the central bank and the budget position of the central government. Lower interest rates and larger fiscal deficits (or smaller surpluses) are associated with higher levels of demand and therefore of output, while higher interest rates and smaller deficits are associated with lower levels of demand and output. Note that while MMT and mainstream economists share this premise, they may have different priors about the relative size of the parameters involved.

5. The evolution of the government debt-GDP ratio over time depends on the current fiscal position (the primary balance), the interest rate on outstanding public debt, and on the nominal growth rate of GDP. This last assumption is not usually stated explicitly, but it is entirely uncontroversial – it is close to an accounting identity—and it is important for what follows.

These assumptions can be formalized as a system of equations:

Equation 1 says that inflation is a positive function of the current level of output, along with its own past or expected values and other variables. P is the inflation rate, PE is the expected inflation rate, Y is output as measured by GDP or a similar variable, and Y* is potential output. In modern macroeconomic models, it is normally assumed that there can be no persistent deviations of expected from realized inflation, so that the long-run Phillips curve is vertical, with Y = Y* the unique level of output at which inflation is stable. In the opposite case, if expected inflation is fixed, there is a unique level of inflation associated with each output gap. For our purposes, it doesn’t matter which of these one believes—in either case an output gap of zero is necessary and sufficient to keep inflation constant at the expected level.

Equation 2 says that output is a negative function of the interest rate, and a negative function of the fiscal balance (or positive function of the government deficit) via the multiplier.4 A is autonomous spending, here defined as the level of output when both the interest rate and fiscal balance are zero. i is the average inflation-adjusted (“real”) interest rate on government debt. η is the percentage increase in output resulting from a point reduction in the interest rate. Note that the value of η reflects both the responsiveness of real activity to changes in interest rates, and how closely the interest rate facing private borrowers changes with the rate on public debt. So no special assumption is needed about whether all interest rates move one for one with the policy rate. If we think they respond less than proportionately, we simply use a lower value of η. b is the primary balance of the government, with positive values indicating a primary surplus and negative values a primary deficit. γ is the multiplier on whatever mix of tax and spending changes are used to adjust the government fiscal balance.

Finally, Equation 3 simply says that the end of period debt is equal to the start of period debt plus the accumulated primary deficits and interest payments. This is the law of motion of government debt, “the least controversial equation in macroeconomics” (Hall and Sargent 2011). Here i, d, and b are again the interest rate, the current debt-GDP ratio, the fiscal balance; and g is the growth rate of output, again net of inflation.

Note that if a significant fraction of the government debt is foreign denominated, Equation 3 would also require an exchange-rate term. There is no problem abstracting from this here, since MMT advocates are clear that their arguments do not apply to a government that borrows in a foreign currency. Borrowing in the currency issued by one’s own central bank is usually the operational definition of “currency sovereignty”, which defines the universe of governments to which MMT’s analysis is supposed to apply.5

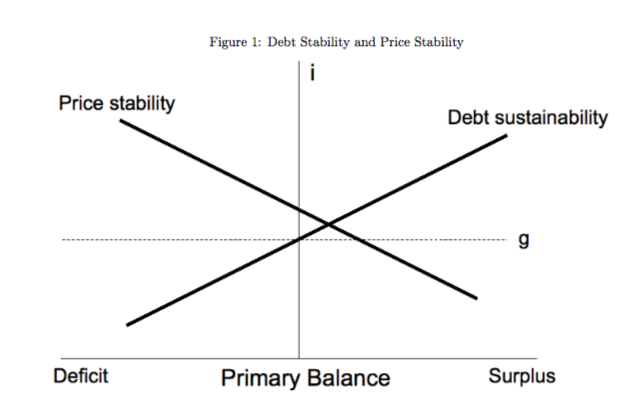

MMT and mainstream macroeconomics agree that the central target for macroeconomic policy is a zero output gap, and they agree on the operational meaning of this—a level of output such that unemployment is low and inflation is low and stable. From Equation 2, we know there is a set of fiscal positions and interest rates that are consistent with a zero output gap. As long as we have two instruments and only one target, any point in this set is equivalent. These combinations are shown as the “price stability” locus in Figure 1.

For the mainstream policy world, a second target is debt sustainability. There is not, however, a clear consensus on the meaning of this target. The weakest form requires only that the debt-GDP ratio converge to a finite value, rather than rising indefinitely. The next strongest is that the ratio remain at or below its current level. The strongest version requires that the ratio remain at or below some exogenously given level. The latter two conditions may be framed as equalities or inequalities; a budget position that implies that the debt fall to zero, or that the government ends up with a positive asset position, may or may not be considered sustainable. For simplicity here, we use the middle condition, that the debt ratio remain at its current level.6 This can easily be extended to the stronger case by setting the required change in the debt ratio to some negative (or positive) value rather than zero, without changing any of the analysis here. MMT does not generally regard the debt ratio as a target, with implications discussed below. At the same time, most MMT advocates would probably agree that the debt ratio should not be allowed to rise without limit. In any case, the question here is whether MMT’s core policy position is consistent with achieving the orthodox debt-sustainability target.

From this point of view, orthodox policy macroeconomics and MMT (or functional finance) can be seen as two routes to the same goal: a combination of monetary and fiscal policy that will achieve full employment levels of output while preventing the debt ratio from rising indefinitely. This is shown graphically in Figure 1.

The “price stability” locus shows those combinations of interest rate and fiscal balance for which the output gap is zero, meaning that inflation is stable at the expected value. The “debt sustainability” locus shows those combinations of interest rate and fiscal balance for which there is zero change in the debt-GDP ratio (if debt sustainability is defined so as to require a reduction in the debt ratio, that would simply mean shifting the debt sustainability locus downward—the logic of the figure would be unchanged). At points above and to the right of the price stability locus, the economy is experiencing high unemployment; at points below and to the left of it, it is experiencing high inflation. Similarly, at points to below and to the right of the debt sustainability locus, the debt-GDP ratio is falling; at points above and to the left of it, the debt ratio is rising.

Since both the the output gap and the change in the debt ratio are jointly determined by the primary balance and the interest rate, we have two instruments and two targets. In the language of Tinbergen (1952), the debate between MMT and mainstream macro can be thought of as a debate over which instrument should be assigned to which target. The consensus assignment is that the interest rate, under the control of an independent central bank, should be assigned to the output gap target, while the fiscal position, under control of the elected budget authorities, should be assigned to the debt sustainability target. In the 25 years before 2008, this assignment was mostly respected in practice, at least in the developed countries. The functional finance assignment is the reverse—the fiscal balance under the budget authorities is assigned to the output target, while any concerns about debt sustainability are the responsibility of the monetary authority.

With two targets, there is a uniquely defined point in the fiscal balance-interest rate space consistent with achieving both, as is visible in Figure 1. An important implication of this is that it does not matter which target is assigned to which instrument—there is only one combination of fiscal position and interest rate that achieves both. If both authorities take into account the effect of their choices on the other authority, they will arrive at the same unique solution regardless of which of them is assigned to each target. While MMT is often seen as a radical departure from current policy, it is in fact consistent with the exact same policy outcomes as orthodox macro. Indeed, with perfect implementation, there would be no way for an outside observer to know if the orthodox or MMT instrument assignment was in effect.

This may seem surprising—if the fiscal authority puts a zero weight on stabilizing the debt ratio, what stops the ratio from rising (or falling) without limit? The point to remember here is that the path of the debt ratio, like the output gap, is jointly determined by the actions of the budget authority and the monetary authority. By taking responsibility for price stability, the fiscal authority frees the monetary authority to take responsibility for debt stability. With respect to MMT, the critical thing to remember is that functional finance does not mean that budget authorities pursue any fiscal balance they choose, only that they pursue the fiscal balance consistent with price stability without concern for financial constraints.7

We may ask whether the central bank can, in fact, control the interest rate faced by the central government. Historical experience suggests that in developed economies that borrow in their own currency, it can indeed do so—the sharp fall in rates in crisis-hit EU countries in 2012 is one recent example. Still, the limits of a central bank’s ability to control interest rates remains an open question. But this question plays no role in the divide between MMT and the mainstream, because the assumption that the monetary authority controls the relevant interest rate is shared by both sides.8 The claim that the central bank can set the interest rate at whatever level is required to stabilize the debt ratio is exactly as strong as the claim that the central bank can set the interest rate at whatever level is needed to maintain price stability. Indeed, as noted above, in a functional finance context these two levels will be the same. There are cases where the central bank cannot be assumed to be able to set the interest rate, for instance in a currency union where the national government does not have its own central bank. In this case, an attempt to follow a functional finance rule may indeed place the debt ratio on an explosive path. But it is important to realize that this is equally a problem for the orthodox assignment, which relies on the central bank to keep output at potential. With the interest rate exogenously fixed, it is in general not possible to achieve the goals of both output at potential and a stable debt ratio, unless some other instrument is introduced.

We noted above that while MMT advocates would probably agree that the debt ratio should not rise without limit, in general, they do not see the debt ratio as an important target for policy. So while a simple swapping of instruments and targets is one way to think about functional finance, this does not describe the usual MMT view of how the policy interest rate should be set.9 What is generally called for, rather, is that the interest rate be permanently kept at a very low level, perhaps zero. In an orthodox policy framework, of course, this would create the risk of runaway inflation; but keep in mind that in the functional framework, the fiscal balance is set to whatever level is consistent with price stability. Rising inflation therefore requires the fiscal balance to shift toward surplus. So a permanently low interest rate implies not rising inflation, but a more contractionary fiscal position (to offset stimulus of low rates) and a declining debt trajectory (In terms of Figure 1, MMT policymakers will probably choose a point on the price-stability locus below its intersection with the debt-stability locus). So contrary to many perceptions, a consistent MMT policy would probably involve larger fiscal surpluses and a lower path for the debt ratio than an orthodox policy in which the budget authorities are expected to maintain a stable debt ratio.

It is no doubt true that, compared with economists in general, MMT advocates place little weight on the dangers of high levels of public debt. But this difference is not relevant for the concrete policy debate. There is no consensus within the “mainstream” about the costs of public debt, or how those costs vary with the level of debt. The idea that there is a sharp cutoff where high public debt ratios reduce growth, or otherwise impose large costs, is less widely believed than it was a decade ago (Pescatori, Sandri, and Simon 2014). More important for present purposes, outside of the special conditions of the zero lower bound, there is no reason to expect an MMT-type policy rule to be associated with higher public debt in the first place.

Given all this, it might be puzzling why there is a debate at all. Why should one care about assignment of instruments to targets if the implied policy is the same in any case? We believe there are good reasons why one might prefer one assignment to another—but these involve practical judgement about policy execution rather than any fundamental difference about how policy works in principle.

In general, the assignment of instruments will matter in any case where implementation is less than perfect. If policy is subject to error, then our choice of assignment will be guided by various considerations:

1. We want to minimize cross effects. Ideally, each instrument should affect mainly its own target. So insofar as we think that demand is highly sensitive to interest rates while fiscal multipliers are small, we will favor the orthodox instrument assignment, and insofar as we think that demand is relatively insensitive to interest rates and fiscal multipliers are large, we will favor the functional finance assignment. On the other side, the effect of interest on the debt grows with the current debt ratio. So the higher the debt ratio, the stronger is the case for assigning the interest rate instrument to it, and the fiscal instrument to the output target. In this sense, the metaphor of “fiscal space” is exactly backward—the case for active fiscal policy gets stronger as the debt ratio rises. This is counterintuitive, but it fits historical experience. In response to the very high debt ratio in the immediate post World War II-period US, for instance, the Fed explicitly committed itself to holding down federal borrowing costs, while the fiscal balance was used to stabilize demand.10

2. Given simple policy rules, the stability of the two assignments may vary. If policymakers are uncertain about the effects of their actions, they are likely to adjust instruments in an iterative fashion, making a small adjustment, observing the behavior of their target, and then making further adjustments. In general, this procedure will converge to the equilibrium only if the effect of the instrument on its assigned instrument are larger than the effects on the other target. In a simple model of this process—in which the instrument is adjusted a fixed fraction of the way toward its own target each period—convergence properties depend on the parameters and current debt ratio. At low debt ratios, both rules converge, at speeds that depend on the relative sensitivity of output to the policy interest rate and the fiscal balance. At high debt ratios only the functional finance assignment converges.11 So if policy is adjusted in an iterative, trial and error way, the choice of assignment determines how quickly, or whether, it approaches the shared equilibrium,

3. Demand conditions are more subject to fluctuations than the debt ratio is. Modern economies are subject to exogenous shocks to output, but not normally to the debt ratio, which moves slowly and predictably. This implies that the instrument that adjusts more quickly should be assigned to output. Historically, this consideration was thought to favor monetary policy, because of the lags in the budget process. But the case is not clear-cut: The greater speed of decision-making by the monetary authority must be weighed against the slower transmission of monetary policy changes through the financial system and the broader economy. In particular, if policy operates only through the shortest rates but it is long rates that are most important for real activity, then policy changes may have to be sustained for a number of years to have a significant effect, making them too slow to respond to business cycle-frequency fluctuations. On the other hand, insofar as output is assigned to fiscal policy, concerns about delays in the policymaking process become an argument for relying more on “automatic stabilizers” rather than on discretionary changes in spending or taxes. This last judgement is generally shared by MMT advocates.12

4. The assignment determines which target is missed in a setting where both cannot be hit. As noted above, if the interest rate cannot be adjusted, then it will not be possible to hit both targets. One important case of this is the zero lower bound (ZLB) on interest rates. Insofar as nominal rates cannot go below zero, then it will be impossible to hit both targets when the intersection of the two lines in Figure 1 lies below a line equal to negative the inflation rate. Since the fiscal position can still be adjusted at the zero lower bound, it is the target assigned to the interest rate that will be missed in this situation. Thus in the context of the ZLB, but only there, it is true that MMT implies a higher path of debt ratio compared with the orthodox assignment. It is not clear that this actually represents a difference with conventional macroeconomics, however – many non-MMT economists would likely agree that in ZLB conditions, active fiscal policy is desirable and stabilizing output is more important than stabilizing the debt ratio.

5. Public authorities cannot always be trusted to follow the stated rules. While theoretical discussions of macroeconomic policy focus on the implications of particular policy rules, real-world policy debates cannot ignore the possibility that the policy rule will be violated by actual decisionmakers, for a variety of reasons. If we think of macroeconomic policy as a principal-agent problem, then one consideration in assigning instruments to targets is how easy it is monitor the actions of the relevant authorities. In general, the fiscal position is easier to monitor than demand policy—the level of public debt, unlike the output gap, can be directly observed, and the law of motion of government debt (Equation 3) is a near-identity while the parameters affecting demand (Equation 2) are subject to a great deal of uncertainty. So it is much easier to tell if the authorities assigned to the debt ratio are following their stated rule, than it is for the authorities assigned to the output gap. If for whatever reason we are not confident in the ability of elected government to pursue a socially optimal output gap, this becomes an argument for assigning this target to an independent body—assuming, of course, that this body can be designed to avoid the institutional problems the budget authorities are subject to.

These considerations reflect judgement calls about policy execution, rather than fundamental differences in analytic framework. We suspect all of them play a role in shaping views on the orthodox versus the functional-finance instrument assignment. MMT advocates do in general believe that demand is less responsive to interest rate changes than mainstream policy economics does, both because most final expenditure decisions are not very sensitive to interest rates and because the financial system does not reliably transmit changes in the policy rate to rates facing ultimate borrowers. The “mainstream” itself contains a wide range of opinions on these questions, however, so MMT supporters are better seen as occupying a point on the continuum of established views rather than a position outside them.

The more fundamental difference may be on the last point. We suspect that most in the mainstream macroeconomic policy world reject a functional finance rule not because they believe that it would not work if followed, but because they believe it would not in fact be followed. There is a widely shared though not always explicitly theorized presumption in mainstream policy discussions that macroeconomic policy in democratic polities suffers from a systematic bias toward deficits and inflation (See for example Portes and Wren-Lewis 2015). The problem, in this view, is not that financial constraints mean that governments cannot achieve the fiscal balance consistent with a zero output gap, but rather that in the absence of (real or imagined) financial constraints they would move toward larger deficits, regardless of demand conditions. Even if one accepts the analysis in this paper and agrees that a functional finance rule need not imply a higher debt ratio, and even if one accepts that considerations 1-4 above on balance favor it, this “inflation bias” might be sufficient reason to prefer the conventional rule. Conversely, many MMT advocates believe that policymakers operating under a conventional assignment consistently err in the direction of accepting unemployment higher than required to maintain stable prices. This bias may be exacerbated by a central bank culture that places an excessive weight on the risks of runaway inflation, which MMT advocates (along with many mainstream economists) see as a very low probability danger in today’s conditions. These judgements about the most likely direction of policy error are quite important for evaluating alternative policy rules, but they do not depend on any difference in strictly economic analysis.

We do not take a position here one way or the other on whether elected governments today are generally subject to inflation bias, or to other biases. Our point is simply that this is the key point of contention. It is unfortunate, in our view, that many MMT texts begin with discussions of endogenous money, chartalism, and the mechanics of government fiscal operations. These arguments are intended to make the case that modern states have the capacity to borrow without limit at an interest rate of their choosing, but there is no need to establish this. It is already implicit in the orthodox view that the central bank can set the interest rate. As a result, debates between MMT and mainstream economists get diverted onto side issues that are irrelevant to the central question of the feasibility of a functional finance rule for public budgets.

We have two concluding thoughts. In our view, it is a mistake for those on the mainstream side of the debate to dismiss MMT supporters as radicals or holders of outré beliefs. They should recognize that MMT is making unconventional policy arguments in a framework of conventional economic analysis. Moreover, the experience of the last decade during which higher levels of debt did not lead to runaway inflation or other obvious costs, and during which conventional monetary policy failed to quickly and reliably close output gaps, should make policy-oriented macroeconomists open to revising their views on the merits of the conventional instrument assignment.

For MMT by contrast, the challenge is to clarify the conditions that make it reasonable to expect a government unconcerned with financial constraints will consistently pursue a fiscal balance consistent with a zero output gap. In order to persuade people in the policy mainstream, MMT must address the real source of their objections, which is, we believe, found not in finance but in political economy. What reason do we have to believe that an elected government that is free to set the budget balance at whatever level is consistent with price stability and full employment would actually do so? This is where the real resistance lies.

We thank Arin Dube for helpful comments.

References

Bianchi, Francesco, and Leonardo Melosi. 2017. “The Dire Effects of the Lack of Monetary and Fiscal Coordination.” National Bureau of Economic Research Working Paper No. 23605.

Blanchard, Olivier. 2016. “The Phillips Curve: Back to the’60s?” American Economic Review 106 (5):31–34.

Fullwiler, Scott T. 2007. “Interest Rates and Fiscal Sustainability.” Journal of Economic Issues 41 (4): 1003-1042.

Furman, Jason. 2016. “The New View of Fiscal Policy and Its Application.” Obama White House Background Paper.

Hall, George J, and Thomas Sargent. 2011. “Interest Rate Risk and Other Determinants of Post-WWII US Government Debt/GDP Dynamics.” American Economic Journal: Macroeconomics 3 (3):192–214.

Kelton, Stephanie. 2017. “How We Think About the Deficit Is Mostly Wrong.” The New York Times, October 5.

Kirsanova, Tatiana, and Simon Wren-Lewis. 2012. “Optimal Fiscal Feedback on Debt in an Economy with Nominal Rigidities.” The Economic Journal 122 (559): 238–64.

Lavoie, Marc. 2013. “The Monetary and Fiscal Nexus of Neo-Chartalism: A Friendly Critique.” Journal of Economic Issues 47 (1): 1–32.

Lerner, Abba P. 1943. “Functional Finance and the Federal Debt.” Social Research 10: 38–51.

Mason, J.W., and Arjun Jayadev. 2018. “A Comparison of Monetary and Fiscal Policy Interaction Under ‘Sound’ and ‘Functional’ Finance Regimes.” Metroeconomica 69 (2): 488–508.

Mosler, Warren. 1995. “Soft Currency Economics.” West Palm Beach, Fl: Self Published.

Pescatori, Andrea, Damiano Sandri, and John Simon. 2014. Debt and Growth: Is There a Magic Threshold? International Monetary Fund Working Paper No. 14/34.

Portes, Jonathan, and Simon Wren-Lewis. 2015. “Issues in the Design of Fiscal Policy Rules.” The Manchester School 83: 56–86.

Tinbergen, Jan. 1952. On the Theory of Economic Policy. Amsterdam: North-Holland.

Woodford, Michael. 2001. “Fiscal Requirements for Price Stability.” National Bureau of Economic Research Working Paper No. 8072.

Wray, L Randall. 2015. Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems. Springer.

1 For a sympathetic but critical assessment of the MMT project as a whole, with a focus on the monetary-operations component, see Lavoie (2013).↩

2 Of course there is work within a modern theoretical framework that raises issues similar to those discussed here. For a discussion of the “current consensus assignment” (monetary policy for demand management, fiscal policy for debt stabilization) versus a functional finance assignment, see Kirsanova and Wren-Lewis (2012). The interaction of fiscal and monetary policy is discussed by Woodford (2001). The desirability of the alternative “functional finance” rule at the zero lower bound is derived within an New Keynesian theoretical framework by Bianchi and Melosi (2017). Models of the Fiscal Theory of the Price Level (FTPL) also bear a nontrivial resemblance to MMT.↩

3 One may doubt whether there is really a “divine coincidence” such that the targets for inflation and unemployment are achieved at the same level of output (Blanchard 2016). But this question is irrelevant here, since the assumption that stable inflation defines the output target is shared by both MMT and the mainstream. For example, Kelton (2017) writes: “Trying to spend too much will cause an inflation problem. … the risk of overspending is inflation…”↩

4 Modern macroeconomic models derive the path of output from a Euler equation, which is intended to capture a process of intertemporal optimization. However, in policy applications this equation is invariably linearized into a form similar to Equation 2.↩

5 See for example Wray (2015, p. 134–36).↩

6 It is sometimes argued that optimal fiscal policy implies that the debt ratio follows a random walk. (Portes and Wren-Lewis 2015) This is equivalent to our debt-sustainability condition that the authorities target the current debt ratio, whatever it may be.↩

7 Wray (2015, 193) give a typical statement of the MMT position: “Just because government can afford to spend does not mean government ought to spend more… Too much spending can cause inflation.”↩

8 One reasons that MMT advocates may perceive a deeper conflict with the mainstream is that MMT first cohered as a body of thought at a time when the monetarism played a larger role in mainstream economics, with a corresponding focus on central bank control over the stock of (high-powered) money as opposed to over the interest rate. When Mosler (1995) wrote that “the overnight rate of interest is the primary tool of monetary policy,” the claim was still somewhat controversial. Today it is a textbook truism.↩

9 Some MMT economists do frame the question in exactly this way, for example Fullwiler (2007).↩

10 The logic implying that fiscal policy is actually favored at high debt ratios has been recognized by some economists in the mainstream policy world, such as Furman (2016): “While the particular result that fiscal expansion by itself will reduce the debt-to-GDP ratio depends on particular parameters and assumptions, the fact that different models find similar results suggests that the idea that fiscal expansion can improve fiscal sustainability is worth taking seriously. … In some respects, this argument may be even more important for high-debt economies like Japan and Italy than for the United States. This is because changes in the debt-to-GDP ratio depend on two factors: (i) the difference between interest rates and the growth rate (strictly speaking, minus multiplied by the debt-to-GDP ratio) and (ii) the primary balance (the difference between revenue and non-interest spending). The larger the debt is, the more changes in dwarf the primary balance in the determination of debt dynamics.”↩

11 We analyze the stability properties of the two rules in Mason and Jayadev (2018).↩

12 It is one reason they favor a job guarantee. Of course there are many other possible solutions to the problem – John Maynard Keynes suggested having a set of public investment projects prepared, whose start dates could be moved forward or back depending on demand conditions.↩