With increasing data available about how the programs were run, we are learning more about how about the financial system worked before the crisis, and how exactly it broke.

My last post gave some context for TSLF; this one uncovers more of the details. TSLF was about upgrading collateral: borrowers could swap bad collateral for good collateral (i.e. Treasuries) with the Fed.

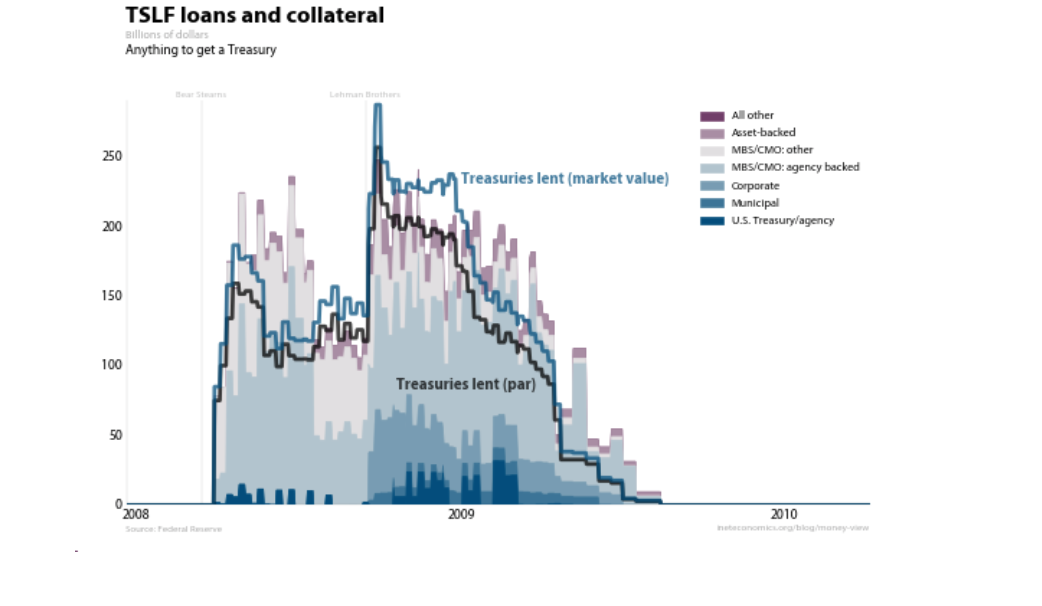

Most of the story is in this graph:

The blue line is the market value of Treasuries the Fed had lent; the black line is par (face value). The colored regions are the market values of collateral accepted.

What was going on here?

The repo market had come to doubt the value of anything less than U.S. government debt as collateral. So everyone needed Treasuries, and with TSLF, the Fed was providing them.

From Bear to Lehman, the program was taking mostly MBS, both agency (pale blue) and private-label (gray). After Lehman, collateral standards were widened, and corporate bonds were put up as well. By accepting low-quality and offering high-quality collateral, the Fed was effectively writing insurance. Indeed, it might have chosen to write credit-default swaps on the low-quality collateral and, perhaps, gotten the repo market working again just as well.

There’s a more subtle story here too. In the graph, the market value of Treasuries lent by TSLF (blue line) is above the par value (face value) of those same securities (black line)—because interest rates were so low (as they still are), they were worth more on the market than their face value. The Fed’s balance sheet from the period when TSLF was in force called the program “fully collateralized” (see Table 1A, note 3). From the graph above, this is only the case if you look at par value.

In other words, TSLF was supporting the financial system in a second, more obscure way: the securities it was lending were worth more to the borrowers than what the Fed was booking for them. Borrowers could take the Treasuries, which the Fed marked at face value, and turn around and use them to get further funding, at the higher market value.

Desperate times…

For the technically inclined

The graph is based on the TSLF transaction data, but it takes some work to extract it. Here’s what I did. Market values for all securities, and par values for Treasuries lent, are reported as total amounts outstanding, by borrower, on each transaction date. So to produce a total value for each category, for each date that the program was in effect, I

- find the most recent loan for each unique borrower

- if it is still outstanding on the date in question, add the reported value to the total for that date.

This means that my graph does not catch the change in market value between loan dates (not an issue for par), which is why it’s a step function rather than a daily series. Note that the data is not clear on how the collateral is being valued.