As early as 1900, German sociologist Georg Simmel identified a central feature of wealth in his seminal work The Philosophy of Money. Simmel writes about the superadditum of wealth for the rich, namely that a great fortune is encircled by innumerable possibilities of use, as though by an astral body.

In 1926 Scott Fitzgerald published the short story “The Rich Boy.” The story begins with the sentences “Let me tell you about the very rich. They are different from you and me.” Ten years later, Ernest Hemingway — a friend of Fitzgerald — wrote in “The snow of Kilimanjaro”: “He remembered poor Scott Fitzgerald and his romantic awe of (the rich) and how he had started a story once that began ‘The rich are different from you and me. And how someone had said to Scott, yes they have more money.’”

The most popular contemporary form of analysis of wealth inequality takes this Fitzgeraldian view. It analyses wealth in a one-dimensional way: it separates a group of the rich from the rest, defined by having more wealth than the others. The “rich” are typically considered to be the group of the wealthiest top 10%, top 5%, or top 1%. The share of this group in total wealth is estimated and compared across countries and time.

This one-dimensional approach to analyzing wealth inequality follows a pure counting logic of more versus less. The simple counting approach is agnostic with regard to the fact that differences in quantities might imply qualitative changes with regard to the prospects that come with wealth. Further, the approach ignores the fact that the meaning of wealth levels and wealth shares also depend on the context in society at a certain point in time. In particular, pension systems and other institutions of welfare states are different over time and across countries.

The agnostic stance stands in contrast to normative interpretations of the statistical results. Interpretations are often based on implicitly assumed links to power and production relations; the OECD argues that higher inequality drags down economic growth and harms opportunities, and specifically that high wealth inequality limits investment opportunities and therefore growth (OECD 2015). Piketty (2013) argues for a tax on wealth to be implemented to slow down the process of wealth concentration for the sake of democracy. However, the share of a percentile itself does not allow normative interpretations, neither positive nor negative.

Piketty himself is aware of these problems and argued several times for a broader approach including social and economic relations between different groups in society. He has made strong claims (2013, 2017) in favor of a relational and multidimensional approach to the analysis of wealth inequality.

A multidimensional approach does not focus only on overall wealth (Stiglitz-Sen-Fitoussi Commission, 2009), but takes into account other related variables, such as income from wealth. A relational approach does not focus only on the rich or the poor, but instead on the whole society and the relations of different groups within society.

As early as 1900, German sociologist Georg Simmel identified a central feature of wealth in his seminal work The Philosophy of Money. Simmel writes about the superadditum of wealth for the rich, namely that a great fortune is encircled by innumerable possibilities of use, as though by an astral body.

In the spirit of Georg Simmel’s remarks on the huge possibilities that come with high wealth, we are currently engaged in developing such an approach to analyse wealth inequality. We introduce different functions of wealth right from the beginning into a class based analysis of wealth inequality (see our preliminary paper “The Functions of Wealth: Renters, Owners and Capitalists across Europe” presented at the WID conference in December 2017: http://wid.world/wp-content/uploads/2017/11/084-Functions_of_wealth-Fessler.pdf ). This allows us to base the analysis of wealth inequality in a setting which is both relational and multidimensional. We use household survey data, since register-based data — which are often used to estimate top shares — hardly allow for such an endeavor.

The work most closely related to ours – we are aware of – is a recently published book authored by the French sociologists Cédric Hugrée, Étienne Penissat, and Alexis Spire. Both approaches share the European-wide perspective on social classes (Hugrée et al 2017).

Towards the functions of wealth

Looking at the wealth distribution alone provides an incomplete picture of the social implications of wealth inequality. Additional insight can be gained by classifying households based on decisive functions of their wealth holdings. A focus on functions of wealth allows a coherent organization of the data justified by social stratification right from the outset. In other words, it makes implicit judgments explicit.

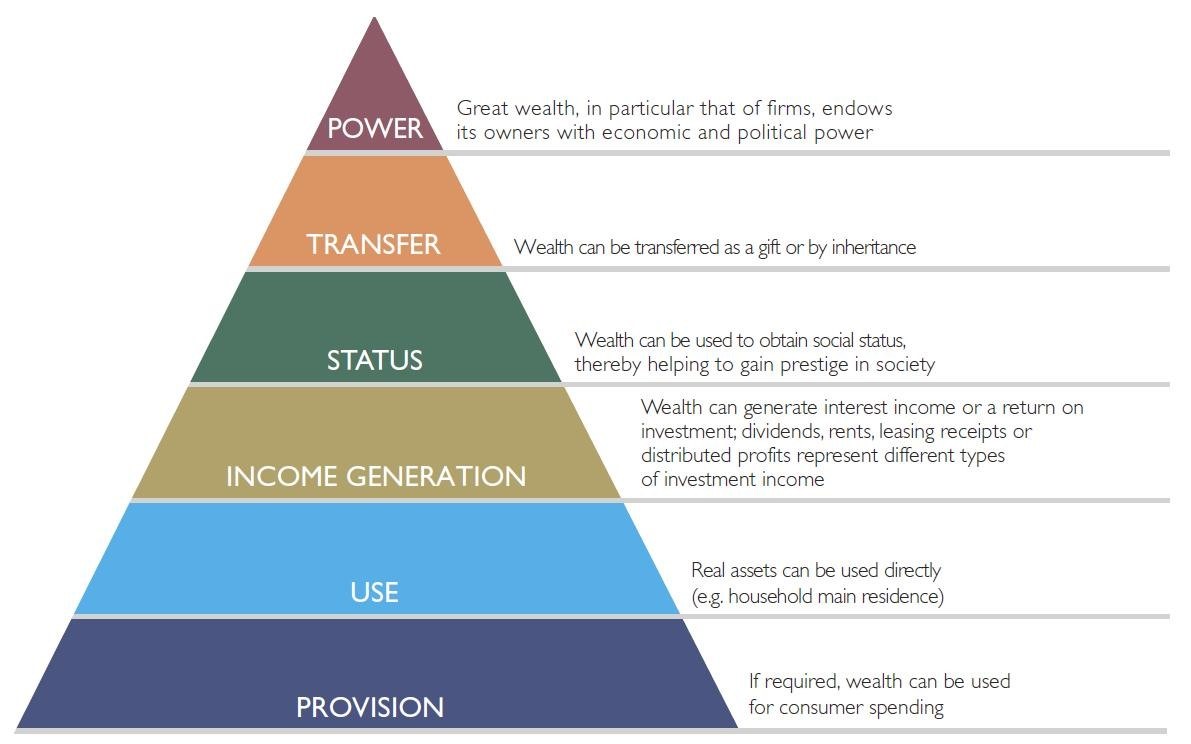

Figure 1 shows a schematic illustration of functions of wealth across the wealth distribution. The more wealth one holds, the more functions are potentially available to them.

Figure 1: Functions of wealth

At the very bottom, households save for all kinds of precautionary reasons, such as the necessary replacement of a washing machine, but also for unexpected unemployment, sickness, or for education. The necessity of this precautionary wealth accumulation depends heavily on existing welfare state policies and the degree to which these policies insure these contingencies of life in an organized way (Fessler & Schürz, 2015). With increasing wealth, the function of use becomes more prevalent. The main item in household wealth, home ownership, is used and therefore provides non-cash income. More wealth in real or financial wealth might allow households to generate substantial cash income. A subgroup of such households at the very top, households with very high wealth of a certain form might be able to exercise power. Recent research shows that especially at the very top of the distribution, the power to directly influence democratic outcomes is rather important (Ferguson et al 2016).

We start from those households whose wealth can fulfill all three main functions: they have resources for precaution, own their home to generate non-cash income, and have self-employed business and/or rent out further real estate to generate cash income. Because these households generate cash and non-cash income from their wealth holdings, we call this group the capitalists. A second group owns their main residence in addition to precautionary savings. They have non-cash income in the form of imputed rents from owning their home, but do not have substantial cash income. These we call the owners. Third, some people only have savings for precautionary reasons and have to pay rent to the capitalists who own their homes. For this third group, wealth mainly has a precautionary function. These are the renters.

Relational approach aligns well with the wealth distribution

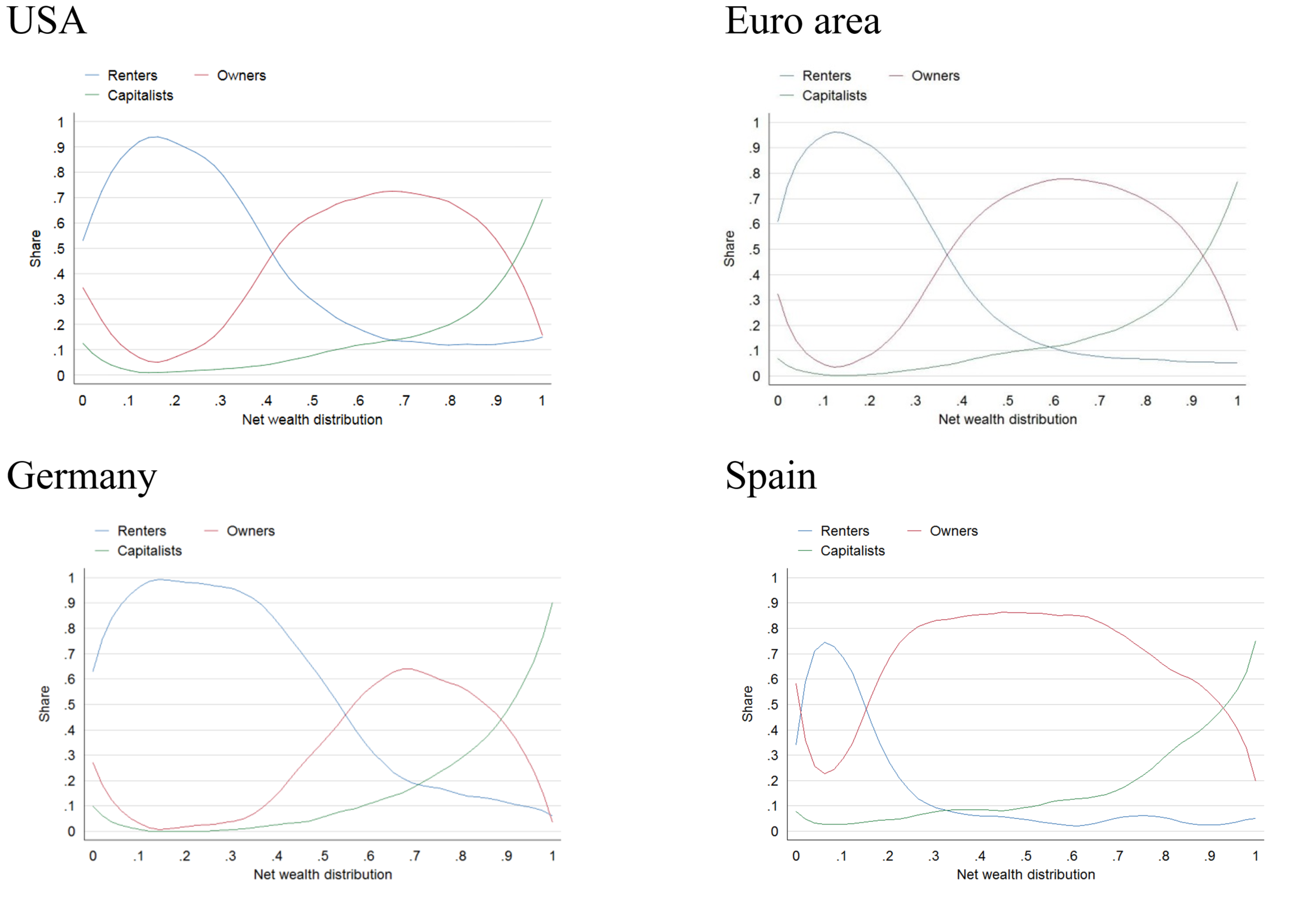

Bringing these definitions to the data, we find renters in the bottom, owners in the middle, and capitalists at the top of the wealth distribution. Theoretically, households should be indifferent between renting or owning a house under the standard assumptions in economic theory (strict life cycle preferences, no bequest motives, no credit constraints, rational behaviour etc.). In practice, however, all of the conditions of the standard model are violated. Households care about bequests (both as recipients and as givers), they face borrowing constraints (like downpayment requirements), they show less-than-fully-rational behaviour and in addition the tax system often favours ownership vis-a-vis renting. Figure 2 shows the resulting estimates for renters, owners, and capitalists in the US and the Euro area. Note that the figure for the US cannot be found in the paper presented at the WID but will be included in an extended version or the paper we are working on currently. The lines can be interpreted as the probability that a household at a certain point of the wealth distribution with a certain level of wealth is a renter, owner, or capitalist.

The same pattern emerges in all countries of the Euro area. In figure 2, we show Germany and Spain as rather extreme cases to illustrate how the general pattern holds while the points and the degree to which a certain class dominates a certain area of the wealth distribution can differ substantially.

Figure 2: Renters, owners and capitalists in US and the Euro area

The country patterns likely differ due to institutional settings, tax law, history, the welfare state, and many other conditions. As an example, different policies for owner-occupiers target different groups in different countries. The bottom 50 shares of wealth in one country can consist mostly of renters’ precautionary wealth while it can comprise mainly of the homes of owners in another country.

This demonstrates that percentile and top share analyses and comparisons might be misleading, as the functions of wealth and corresponding relations between social groups are different across the wealth distribution in different countries.

A multidimensional view of inequality

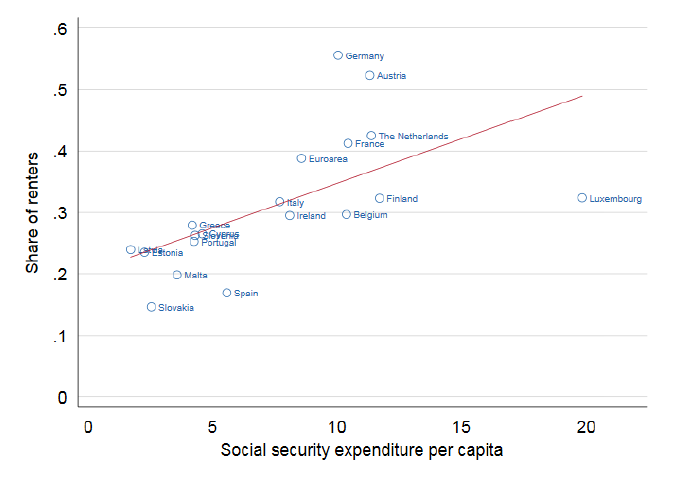

The welfare state strongly shapes the meaning of asset ownership for renters and owners. Figure 3 shows how the share of renters is positively correlated with social security expenditures across countries. In countries with higher social security expenditures, there are typically also larger degrees of state-organized pension systems, housing subsidies, social housing, and regulated rental markets. In turn, a larger share of renters often goes along with smaller household sizes, as it is easier for younger people to form their own households and easier for the elderly to sustain their households for a longer time.

Figure 3: Share of renters and social security expenditure

The form of income plays a major role in the definition of our typology. Capitalists use their capital via businesses to generate capital income. In addition, or alternatively, they use their real estate wealth to get rental income. Renters pay their rent from their labor income, whereas owners use their homes to live in, generating an imputed rent (which is not included in our definition of gross income). Income — and not wealth — is the decisive economic variable for renters. Thus, analyzing the wealth distribution has to be done in a multi-dimensional way. Instead of comparing capital-to-income ratios across countries and over time, it might be worthwhile to zoom in and find the common patterns inside contemporary societies.

Regardless of large country differences in the share of renters, renters’ median yearly gross income is (mostly substantially) larger than their median net wealth. In most cases, yearly income is about 2-5 times larger than net wealth, which translates to capital/income ratios of 0.2 to 0.5. For owners, that relationship is turned around. Capital-to-income ratios based on medians for owners are well above 5 — and they go up to 13 for capitalists.

Justification of wealth inequality

In economics, there seems to be a kind of consensus that an increase in wealth inequality might be bad. The OECD claims that it is bad for growth and (investment) opportunities; Piketty argues that it harms democracy.

There is a long tradition in philosophy starting with Plato and Aristotle of normative substance that deals with wealth explicitly. In Plato’s “Republic”, wealth is judged in moral terms. Plato claims that large levels of wealth have negative consequences for individuals and for \ society and that only moderate wealth enables a moral life. Otherwise, he explains, two parallel cities exist, “the city of the poor and the city of the rich” in one place.

In his later work “Laws,” Plato stresses that wealthy citizens feel that their wealth is more valuable than their virtue. Thus, they believe that they do not need to follow the laws that would create social harmony. Plato´s prescription is to cap wealth for the richest citizens at four times the wealth of the poorest ones.

In contemporary society, moral qualifications in support of and against entrepreneurs exist. Either their economic success is proof of being talented, risk-oriented, or innovative, or it is a sign of their greed and selfishness. Further, evaluations such as the concepts of earned and unearned wealth and the subsequent moral differentiation between self-made millionaires (working rich) and inheritors (trust-fund babies) point towards issues of justification.

Coherent justifications of wealth inequality need a focus on different wealth functions. The functions of precaution, use and power have to be distinguished. It is obvious that meritocratic justifications of the wealth of the rich has to be questioned. Statistical analyses show that there is even a privileged position of capitalists in the inheritance process (see our preliminary paper presented at the WID: http://wid.world/wp-content/uploads/2017/11/084-Functions_of_wealth-Fessler.pdf).

Capital versus wealth debate

A relational and multidimensional approach to wealth inequality contributes to recent theoretical debates on the roles of capital and wealth.

Already during the famous Cambridge (US vs. UK) capital controversy in the 1960s, the main question was one of aggregation. Joan Robinson, Piero Sraffa and others (Cambridge UK) basically argued that the jump from micro to macro, as done by capital aggregation in mainstream theory, ignores more complex economic structures based on power relations and class structures necessary to understand the production process at the level of the society (see Taylor 2015 and Garbellini 2018).

Our approach allows us to distinguish between private wealth as a substitute for public wealth (precautionary wealth), private wealth as a source for non-cash income (housing wealth used), and private wealth as a mean of production generating profit (business wealth and rental income from housing wealth beyond the home). These different forms of private wealth are tied to different classes and accompanying power relations.

As Lance Taylor recently discussed, inequality is driven by the power of capital in relation to workers and how this relationship was transformed over the past four decades (Taylor 2017a and Taylor 2015b). Private wealth must be interpreted in relation to different volumes of public wealth and different institutional settings over time and between countries. These are relevant factors and drivers of the power relations between renters, owners and capitalists. This conceptualization is easily overlooked when just analyzing top shares of private wealth. Today, the role of top incomes in this context is especially difficult to assess because of the role stock buy-backs play in raising executive compensations (see Lazonick and Hopkins 2016). How wealth is used to exercise political power at the very top of the distribution can also be studied by analyzing industry contributions to political campaigns. Ferguson et al. 2018 recently employed such data to analyze this process for the 2016 Presidential Campaign.

Conclusions

Wealth analyses often hide their normative considerations behind statistical presentations of percentiles and top shares. Those who focus on the wealth share of the rich will overlook the rest, missing society as a whole and what it means to be at the top of the wealth distribution.

The heterogeneity of wealth inequality cannot be reflected by a one-dimensional focus on net wealth. We should look instead at structured wealth inequality through the lens of social classes. Such a structure needs to link wealth to its functions, right from the start of the statistical analysis, and base the groups on social relations instead of arbitrary levels of wealth itself. The social structure concerning wealth can be characterized by roughly three classes which align well with the wealth distribution. This alignment holds even if one controls for socioeconomic characteristics used in class analysis such as education and occupation or main determinants of wealth accumulation such as age. A class-based approach has advantages with regard to the measurement and analysis of wealth. However, the main advantage is that implicitly assumed links to power and production relations – which are the foundation of contemporary interpretation of top shares (see OECD 2015 and Piketty 2013) – are made explicit. On top of that, such an approach can be directly linked to questions of justification of wealth inequality and allows us to distinguish between wealth as a means of capitalist production and other forms of wealth.

Literature

- An earlier version of this paper was presented at the World Income Database conference 2017.

- Alvaredo, Facundo, Anthony B. Atkinson, Thomas Piketty, and Emmanuel Saez.2013. The Top 1 Percent in International and Historical Perspective, Journal of Economic Perspectives, 27 (3), 3,20.

- Alvaredo, Facundo, Salvatore Morelli, and Anthony B. Atkinson. 2017. Top wealth shares in the UK over more than a century, Technical Report.

- Garbellini, Nadia. 2018. Inequality in the 21st century: A critical analysis of Piketty’s work. Institute for New Economic Thinking Working Paper No.69; https://www.ineteconomics.org/perspectives/blog/what-piketty-missed-in-measuring-wealth

- Ferguson, Thomas, Paul Jorgensen and Jie Chen. 2018. Industrial Structure and Party Competition in an Age of Hunger Games: Donald Trump and the 2018 Presidential Election. Institute for New Economic Thinking Working Paper No. 66. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3125217

- Ferguson, Thomas, Paul Jorgensen, and Jie Chen. 2016. How Money Drives US Congressional Elections. Institute for New Economic Thinking Working Paper No. 48. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2817705

- Fessler, Pirmin and Martin Schürz. 2015. Private wealth across European countries: the role of income, inheritance and the welfare state, Working Paper Series 1847, European Central Bank September.

- Hugrée, Cédric, Étienne Penissat, and Alexis Spire. 2017. Les classes sociales en Europe: Tableau des nouvelles inégaltés sur le vieux continent. Agone.

- OECD. 2015. In It Together: Why Less Inequality Benefits All, OECD.

- Piketty, Thomas. 2011. On the Long-Run Evolution of Inheritance: France 1820-2050, The Quarterly Journal of Economics, 126 (3), 1071-1131.

- Piketty, Thomas. 2013. Capital in the Twenty-First Century.

- Piketty, Thomas. 2014. Capital in the Twenty-First Century: a multidimensional approach to the history of capital and social classes, The British Journal of Sociology, 64.

- Stiglitz-Sen-Fitoussi Commission. 2009. Report by the Commission on the Measurement of Economic Performance and Social Progress. www.insee.fr/fr/publications-et-services/dossiers_web/stiglitz/doc-commission/RAPPORT_anglais.pdf.

- Taylor, Lance. 2017a. Why Stopping Tax “Reform” Won’t Stop Inequality. INET. https://www.ineteconomics.org/perspectives/blog/why-stopping-tax-reform-wont-stop-inequality

- Taylor, Lance, Özlem Ömer and Armon Rezai 2015b. Wealth Concentration, Income Distribution, and Alternatives for the USA. Institute for New Economic Thinking Working Paper, No. WP 17. https://www.ineteconomics.org/uploads/papers/WP17-Lance-Taylor-Income-dist-wealth-concentration-0915.pdf

- Taylor, Lance. 2015a. Veiled Repression: Mainstream Economics, Capital Theory, and the Distributions of Income and Wealth, Institute for New Economic Thinking Working Paper No. 32; https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2718708

- Lazonick, William and Matt Hopkins 2016. If CEO Pay Was Measured Properly, It Would Look Even More Outrageous. INET. https://www.ineteconomics.org/perspectives/blog/if-ceo-pay-was-measured-properly-it-would-look-even-more-outrageous