Ban buybacks to Build Back Better

With the election of Joseph R. Biden Jr. as president of the United States, Americans got a leader whose stated objective as a candidate was to put the nation back on a path to stable and equitable growth. Quite apart from the devastation wrought by the Covid-19 pandemic, that is a very tall order after four decades of income inequality and employment instability. But as vice president, Biden understood that a big part of the problem was “buybacks.” Look at how he concluded a Wall Street Journal op-ed on the subject in September 2016:

The federal government can help foster private enterprise by providing worker training, building world-class infrastructure, and supporting research and innovation. But government should also take a look at regulations that promote share buybacks, tax laws that discourage long-term investment and corporate reporting standards that fail to account for long-run growth. The future of the economy depends on it.

In an interview with the Las Vegas Sun on January 11, 2020, Biden, as a candidate for the Democratic nomination for president, criticized buybacks because they shortchange R&D investment and workers’ wages. As a remedy, he said: “I’m going to reinstate [the policy] that changed under the Reagan administration, when the SEC suggested there’s not a limitation on buybacks.” With the pandemic upon us, on March 20, 2020, candidate Biden tweeted: “I am calling on every CEO in America to publicly commit now to not buying back their company’s stock over the course of the next year. As workers face the physical and economic consequences of the coronavirus, our corporate leaders cannot cede responsibility for their employees.”

During the second quarter of 2020, buybacks by companies in the S&P 500 Index fell to about $90 billion from over $200 billion in the previous quarter. But by the second quarter of 2021, with President Biden in office, they bounced right back up to $200 million. By the third quarter of 2021 buybacks reached an all-time quarterly record of $235 billion, surpassing the previous peak of $220 billion in the fourth quarter of 2018, when share repurchases had been fueled by the Republican tax cuts. For all of 2021, at close to $850 billion, S&P 500 buybacks easily outstripped the previous annual record of $806 billion in 2018.

Yet, in the White House, President Biden has been silent on stock buybacks. In his first State of the Union Address, on March 1, 2022, there was absolutely no mention of them. Last September, there was a proposal from Sen. Sherrod Brown (D-OH) and Sen. Ron Wyden (D-OR) for buybacks to be taxed at two percent. In October, the White House’s Build Back Better Framework proposed a buybacks surcharge of one percent. There was the predictable business blowback about how even a small tax on buybacks would mean the end of the stock-market boom. Despite good intentions, however, whether at two or one percent, these surcharge proposals would only serve to legitimize buybacks, and the tax revenue raised from them would come nowhere near to offsetting the immense damage to the U.S. economy and U.S. households that buybacks cause.

A growing body of research, much of it carried out by my nonprofit organization, the Academic-Industry Research Network, in collaboration with the Institute for New Economic Thinking, shows why, in a range of industries, stock buybacks are toxic. They are a prime cause of extreme income inequality, the disappearance of stable employment opportunity, and sagging U.S. industrial productivity. If the Biden administration insists on taxing rather than banning buybacks, then it should set the surcharge at, say, 40 percent, with a mandatory warning banner on the corporate repurchaser’s website that reads: STOCK BUYBACKS DESTROY THE MIDDLE CLASS.

In a world without buybacks, corporations could instead use their profits to reward workers with higher pay and more employment security while increasing investment in their productive capabilities. The U.S. labor force would then be better positioned to contribute its skills and efforts to generating America’s next round of innovative products. Banning buybacks as open-market repurchases (as the vast majority of them are) would be a crucial step along a path toward stable and equitable growth in the United States, characterized by upward socioeconomic mobility rather than the downward slide that has afflicted a growing proportion of U.S. households since the 1980s.

One proposal that the Biden administration would do well to get behind is the Reward Work Act, introduced by Sen. Tammy Baldwin (D-WI) in March 2019. It would rescind Rule 10b-18, adopted by the Securities and Exchange Commission (SEC) in November 1982. This SEC rule gives a corporation a “safe harbor” against stock-price manipulation charges when doing buybacks as open-market repurchases. In many cases, as we show below, the safe-harbor “limit” can be hundreds of millions of dollars spent on stock buybacks per trading day. In a paper we are writing on the origins of Rule 10b-18, Ken Jacobson and I call SEC Rule 10b-18 “a license to loot,” while in a book that I published two years ago with Jang-Sup Shin, we call out buybacks for what they are: Predatory Value Extraction.

Apple: The biggest corporate looter of them all

The most egregious buybacks offender is Apple, which from October 2012 through December 2021 threw away $484 billion—92 percent of its enormous net income—on open-market repurchases, the sole purpose of which was to boost the company’s stock price. In addition, Apple funneled $118 billion in dividends to shareholders, sucking up another 23 percent of net income. For March 1, 2022, Apple’s safe-harbor daily “limit” for buybacks under Rule 10b-18 was $3.5 billion.

Apple calls these distributions to shareholders its “Capital Return Program.” But how can Apple “return” cash to those who have never given the company anything? The only money that Apple raised from the public stock market in its 46-year history was the $97 million realized from its initial public offering in 1980. When, in the summer of 2013, corporate predator Carl Icahn purchased $3.6 billion worth of Apple shares on NASDAQ and then, in the winter of 2016, sold that stake on NASDAQ for a $2-billion gain, not one cent went to fund investment in Apple’s productive capabilities. To the contrary, apparently succumbing to Icahn’s wealth, visibility, hype, and influence, Apple CEO Tim Cook and his board of directors helped the hedge-fund activist reap those financial gains by doing $45.0 billion in buybacks in its fiscal 2014 (ended September 27) and $35.3 billion in fiscal 2015—the two largest annual expenditures on buybacks ever executed by any company at that time.

Then, in the winter of 2016, as Icahn was dumping his Apple shares, Warren Buffett, using Berkshire Hathaway money, started buying Apple shares on NASDAQ until by September 2018 he had shelled out $36.3 billion, giving him 5.1 percent of Apple’s shares outstanding. In May 2018, Buffett enthused in an interview: “I’m delighted to see [Apple] repurchasing shares. I love the idea of having our 5 percent, or whatever it is, maybe grow to 6 or 7 percent without our laying out a dime.” After having repurchased $32.9 billion in 2017, Apple granted the Oracle of Omaha his wish, as the company’s buybacks were $72.7 billion in 2018, $66.9 billion in 2019, $72.4 billion in 2020, and $86.0 billion in 2021. Apple maintained the pace with $20.4 billion in buybacks in the first quarter of 2022 (ended December 25, 2021).

By January 2022, Buffett’s Apple shares were valued at $160 billion, even after he had sold 12 percent of his original stake for $13 billion and had raked in another $3 billion in dividends. He now held almost 5.6 percent of Apple’s stock outstanding, but that figure would have been 6.3 percent if Buffett had not sold some of his shares. While Buffett was remarkably candid in saying that he could increase his percentage held in Apple “without our laying out a dime,” he might have added, “and without one cent of the $36.3 billion that I paid to buy Apple’s shares flowing into the company to invest in its productive capabilities.”

With the help of $374 billion in Apple buybacks since the winter of 2016, when Buffett began accumulating Apple stock, Berkshire Hathaway has profited immensely from the greatest treasury robbery in U.S. corporate history. The looting has been perfectly legal (as far as we know) because of SEC Rule 10b-18, adopted (without public comment) on November 17, 1982—the real birth date, in historical retrospect, of the pernicious and flawed ideology that, for the sake of economic efficiency, a business corporation should be run to “maximize shareholder value” (MSV).

This is not the first time that Apple’s top management has been guided by MSV as its corporate goal. In 1985, after founder Steve Jobs was ousted from the company, Apple CEO John Scully sought to drive up the company’s stock price, and his own pay, with dividends and buybacks. By 1996 and 1997, Apple was taking huge losses and had to be bailed out by Microsoft in the form of a $150-million purchase of preferred shares. It was in this context that Jobs regained strategic control of Apple and reinstituted a “retain-and-reinvest” regime—eschewing distributions to shareholders in order to reinvest profits in Apple’s productive capabilities—culminating in the launch of the iPhone in 2007.

Jobs passed away in October 2011. During his tenure as Apple CEO from September 1997 to August 2011, the company’s share price had risen by 7,000 percent. Innovation had amply rewarded loyal Apple shareholders, in part because Jobs did not do buybacks to manipulate the company’s stock price. Tim Cook, Jobs’ successor as CEO, had previously been Apple’s chief supply-chain executive, with his most profound contribution to the company having been outsourcing its manufacturing to Foxconn in China. In the fourth quarter of fiscal 2012 (ended September 29), Apple paid dividends for the first time since 1996, and, in the first quarter of fiscal 2013, the current buybacks spree commenced.

In October 2014, as shareholder Icahn was pressuring CEO Cook to do $100 million in buybacks, I questioned Apple’s so-called “Capital Return Program,” which at that time included an announcement made in April 2014 that the Apple board had authorized a total of $90 billion in buybacks and $40 billion in dividends by December 2015. I also published an open letter to CEO Cook, suggesting ways in which, instead of doing buybacks, he could allocate Apple’s cash to innovative investments and support an equitable income distribution, including a) more compensation for tens of thousands of employees in Apple stores (not to mention hundreds of thousands of people working at companies in Apple’s global supply chain); b) more educational support to enhance the career opportunities for Apple employees, especially for those in dead-end jobs in Apple stores and call centers; c) collaboration with government agencies in social investments in knowledge and infrastructure; and d) collaboration with government agencies in social innovation to develop the technologies of the future to meet society’s needs.

Recently, Matt Hopkins and I published an INET working paper, “Why the Chips Are Down,” in which we ask why the U.S. federal government should provide the U.S. semiconductor industry with $52 billion in subsidies under the CHIPS for America Act, when the tech companies, including Apple, that are lobbying for its passage did about 17 times the requested subsidy in buybacks in 2011-2020. We also note that Apple’s decisions to outsource the fabrication of its iPhone chips, first to Samsung Electronics and then, exclusively from 2015, to Taiwan Semiconductor Manufacturing Company (TSMC), has enabled these two firms to become the world’s leading chip foundries.

In our paper, Hopkins and I reference a 2010 article entitled “Apple should build a fab,” addressed to Apple CEO Jobs, by a prominent electronics-industry journalist, Mark LaPedus. At the time, Apple was reliant for chip fabrication on its emerging smartphone competitor, Samsung Electronics. LaPedus recognized that “in an age when real men go fabless, I concede it’s an unconventional idea. You might think it’s absurd. But an Apple A4 fab today could keep the iProduct franchise in hay—and Samsung at bay.”

As Jobs passed the CEO torch to Cook, Apple investing in its own fab was a road not taken. Now, under pressure from U.S. trade negotiators, Samsung and TSMC have begun building new state-of-the-art fabs in the United States, at a projected cost of $17 billion and $12 billion, respectively. Those sums combined are just 34 percent of the $86 billion that Apple spent on buybacks in fiscal 2021 alone.

When, in May 2018, Cook was asked what he planned for Apple’s $285 billion in cash, which the company was repatriating from abroad as a result of tax breaks provided by the Republican Tax Cuts and Jobs Act of 2017, he replied: “We’re going to create a new site, a new campus within the United States. We’re going to hire 20,000 people. We’re going to spend $30 billion in capital expenditure over the next several years. Number one, we’re investing, and investing a ton, in this country. We’re also going to buy some of our stock, as we view our stock as a good value.” The buybacks that Cook called “some of our stock” amounted to $73 billion in 2018. And, we can ask: “Good value” for whom?

Apple’s board authorizes the company’s massive buybacks. The Apple director with the longest tenure is Arthur D. Levinson, who has been on the board since 2000 and its chair since late 2011. Levinson is a scientist who spent most of his career with the pioneering biopharmaceutical company Genentech, joining the firm in 1980 and becoming its CEO from 1995 to 2009 and chairman of its board from 1999 to 2014. From 1990, Levinson and other Genentech employees were protected from the pressures of predatory value extractors by the majority ownership of the company by F. Hoffmann-La Roche AG, a Swiss-based corporation, better known simply as Roche, that is both the least financialized and, currently, the most innovative of the global “Big Pharma” companies. Given his employment experience, Dr. Levinson could have advised Apple on how it might have invested a portion of the hundreds of billions of dollars that it has wasted on buybacks in supporting companies engaged in medicine innovation.

The Apple director with the second-longest tenure is Albert Arnold Gore Jr., who has been on its board since 2003. The former U.S. vice president and Democratic candidate for president in 2000 has been one of the world’s leading activists for social awareness of the threat of global warming to human existence. In 2006 Gore released his documentary An Inconvenient Truth, which went on to win an Oscar. Mr. Gore could have advised Apple on how it might have invested even a portion of the hundreds of billions of dollars that it has wasted on buybacks to combat climate change.

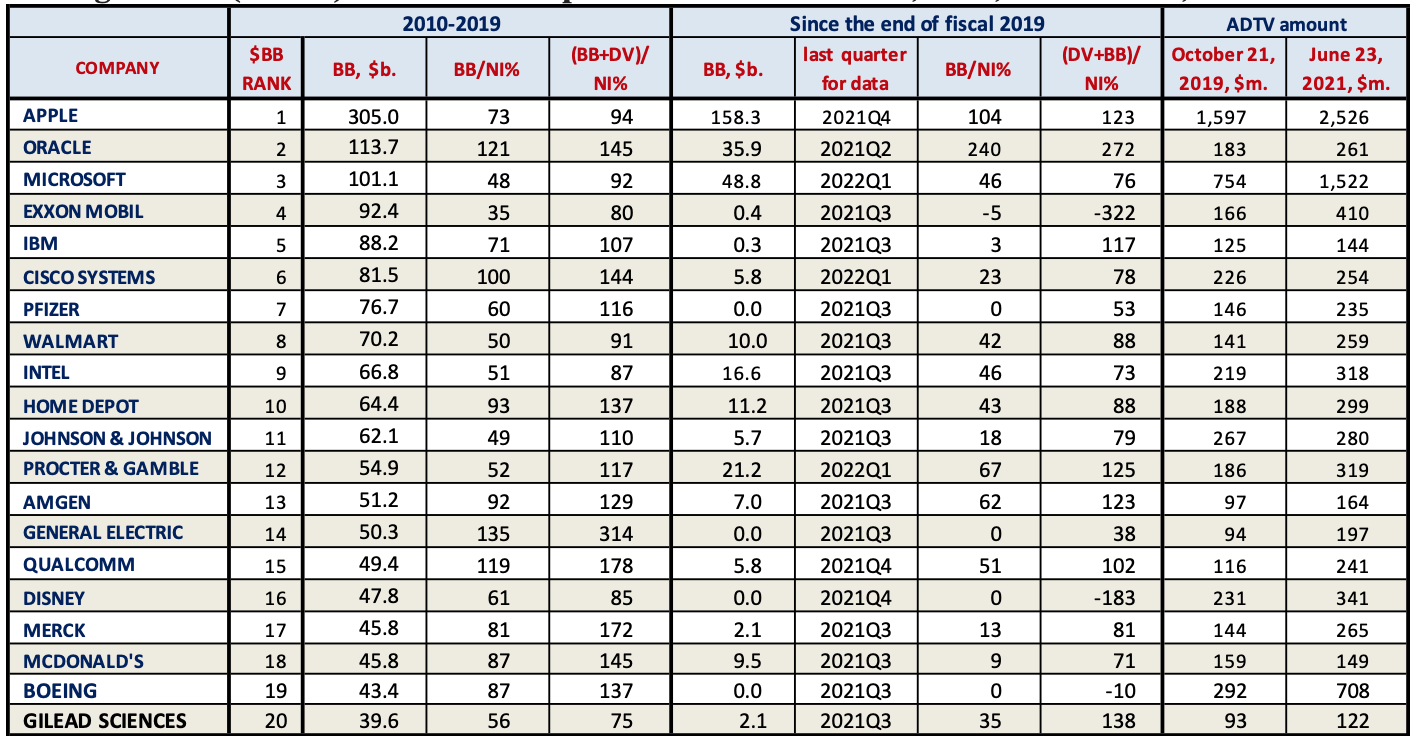

The 20 largest industrial repurchasers

Apple is not the only major U.S. company that has been sacrificing America’s future on the altar of MSV. The following table shows the top 20 purchasers among industrial (or non-financial) corporations for 2010-2019. Of these 20 companies, 13 distributed more than 100 percent of net income to shareholders over the decade while the other seven distributed 75 percent or more. Coming into the pandemic, 12 companies on the list—Apple, Oracle, Microsoft, Cisco, Walmart, Intel, Home Depot, Johnson & Johnson, Amgen, Qualcomm, Disney, and Gilead—were in what I call “dominate-and-distribute” mode, using the profits from their still-dominant market positions primarily to support their stock price; while the other eight—Exxon Mobil, IBM, Pfizer, Procter & Gamble, General Electric, Merck, McDonald’s, and Boeing—were in “downsize-and-distribute” mode, distributing corporate cash to shareholders as they downsized their labor forces.

This ranking of the largest repurchasers among U.S. industrial corporations is based on buyback activity in 2010-2019, prior to the Covid-19 pandemic. The table also shows the buybacks done by these 20 companies since the beginning of fiscal 2020, covering the period of the pandemic to the date of each company’s financial report through December 2021. Apple, Oracle, Microsoft, Walmart, Intel, Home Depot, Procter & Gamble, Qualcomm, and Amgen have spent 42 percent or more of net income on buybacks during this period. These nine companies have benefited from very strong demand for their products and high profits during the pandemic.

The last two columns of the table show the rather generous ADTV amounts for the 20 largest repurchasers among industrial companies, 2010-2019, at two points in time, one in advance of the pandemic and one in the midst of it. Except for McDonald’s, the ADTV amounts all rose, in many cases substantially, in June 2021 compared with October 2019, reflecting combinations of higher stock prices and higher stock trading volumes. Notwithstanding a sharp downturn in March 2020, when the World Health Organization declared the spread of SARS-CoV-2 a pandemic, the U.S. stock markets have boomed.

Twenty largest stock repurchasers, 2010-2019, among U.S. industrial corporations, their buybacks since fiscal 2020 through December 2021, and their SEC Rule 10b-18 safe-harbor average daily trading volume (ADTV) amounts for repurchases on October 19, 2019, and June 23, 2021 Notes: BB=stock buybacks; DV=cash dividends; NI=net income; ADTV=average daily trading volume limit to secure the safe harbor against stock-price manipulation charges under SEC Rule 10b-18. Sources: Company 10-K and 10-Q filings with the SEC; Yahoo Finance daily historical stock prices. The table includes the latest quarterly data available for each company as of December 31, 2021.

The Academic-Industry Research Network has done research on the shift from innovation to financialization at many of these companies, along the lines of our work on Apple, summarized above (see, for example, Cisco, General Electric, Pfizer, Intel, Merck, McDonald’s, and Boeing). Yet, at two of these companies—Pfizer and Intel—buybacks have ceased for the sake of investing in innovation, with pointed denunciations of repurchases by their current CEOs. Their negative views of buybacks are noteworthy, not only because they run leading companies that are of critical importance to America’s economy, health, and security, but also because the CEOs’ criticisms of stock buybacks may encourage politicians, including President Biden, to take a stand against corporate financialization.

A highly financialized corporation from the late 1980s, in early 2019 Pfizer committed to doing $8.9 billion in buybacks, to be completed by August 1 of that year. Thereafter, the company ceased doing buybacks as it turned its strategic attention to conserving a portion of its profits to finance investment in its drug pipeline. Previously, Pfizer’s strategy had been to acquire other companies with lucrative drugs on the market that had years of patent life left and to extract the profits to fund its distributions to shareholders. By 2019, however, with acquisition targets disappearing and the patents on a number of Pfizer’s major drugs expiring, its board recognized that Pfizer itself could be acquired by another Big Pharma company unless it could develop high-revenue (“blockbuster”) drugs internally.

Since August 2019, for the sake of internal drug development, Pfizer has done no buybacks. Indeed, in a rare move among U.S. corporations, in January 2020 Pfizer committed to forego buybacks that year, and it did so again in January 2021. The company did, however, increase its dividend in 2019, 2020, and 2021. The implementation of this change in Pfizer’s investment strategy entailed the retirement of Ian Read as Pfizer CEO as of January 1, 2019, in favor of current CEO Albert Bourla. As CEO from 2011, Read had engaged in downsize-and-distribute. In an earnings call with stock-market analysts in January 2020, Bourla made a rather extraordinary admission of the company’s financialized past when he made it clear that Pfizer had stopped doing buybacks so that the company could invest in innovation:

The reason why in our capital allocation, we are allocating right now money [is] to increase the dividend and also to invest in our business…all the CapEx to modernize our facilities. The reason why we don’t do right now share repurchases, it is because we want to make sure that we maintain very strong firepower to invest in the business. The past was a very different Pfizer. The past of the last decade had to deal with declining of revenues, constant declining of revenues. And we had to do what we had to do even if that was financial engineering, purchasing back ourselves. We couldn’t invest them and create higher value. Now it’s a very different situation. We are a very different company (“Event Brief of Q4 2019 Pfizer Inc Earnings Call – Final,” CQ FD Disclosure, January 28, 2020).

Bourla did not explain why the “old” Pfizer—which, less than 12 months before, had done $8.9 billion in buybacks—“had to do what we had to do even if that was financial engineering, purchasing back ourselves.” But his rambling statement is a very rare recognition by a CEO of a major U.S. corporation that stock buybacks are the enemy of investment in innovation.

As the case of Pfizer clearly illustrates, even within business corporations that have become the leading repurchasers of their own stock, there is an ongoing tension between innovation and financialization, with the outcomes determined by specific sets of circumstances. Intel, No. 9 in buybacks in the table above, is another explicit example of a company’s attempting to shift corporate strategy from financialization to innovation in an advanced-technology industry, with cessation of buybacks as an important part of that strategy.

Once the world leader in chip fabrication, a financialized Intel found itself falling behind in the face of innovative global competition. Under its new leadership, Intel is now seeking to invest in advanced nanometer fabrication facilities with the goal of catching up with industry leaders TSMC and Samsung Electronics. Intel ceased doing stock buybacks from the second quarter of 2021 after replacing CEO Robert Swan, a finance expert, with Pat Gelsinger, a technology expert. In a 60 Minutes interview, Gelsinger said that a condition of his taking the top Intel job was assurances from the company’s board that Intel would “not be anywhere near as focused on buybacks going forward as we have in the past.”

In a subsequent interview with CNET in November 2021, Gelsinger was much more expansive and emphatic. He recounted how, before taking the CEO job, he had written a strategy paper for Intel’s board, for which he got their unanimous agreement. “I was concerned,” Gelsinger said in the interview, “about how we get the process roadmap back in shape.” He continued:

We underinvested in capital. I went to the board and said: “We’re done with buybacks. We are investing in factories.” And that is going to be the use of our cash as we go forward. And they aggressively supported that perspective; that we needed to just start investing, and those investments would start creating a cycle of momentum that would get our factory teams executing better.

A seven-point rewrite of President Biden’s SOTU Address

Had President Biden’s speechwriters been inclined to be critical of stock buybacks, and had they been aware of the statements of CEOs Bourla and Gelsinger, here is how the President could have addressed an issue on which, as Vice President, he had said the future of the economy depended. I have made my own speechwriting additions in bold typeface to seven relevant portions of the text of the President’s State of the Union Address:

Addition #1:

We meet tonight in an America that has lived through two of the hardest years this nation has ever faced.

The pandemic has been punishing. Moreover, in 2021 stock buybacks by U.S. corporations were at a record high.

And so many families are living paycheck to paycheck, struggling to keep up with the rising cost of food, gas, housing and so much more.

Addition #2:

For the past 40 years, we were told that tax breaks for those at the top and benefits would trickle down, and everyone would benefit.

But, in the presence of corporate financialization, manifested by trillions upon trillions of dollars in stock buybacks, that trickle-down theory led to a weaker economic growth, lower wages, bigger deficits and a widening gap between the top and everyone else in nearly a century.

Addition #3:

When we use taxpayers’ dollars to rebuild America, we are going to do it by buying American: buy American products, support American jobs, provided by American companies that invest in their employees rather than extract the value that these employees create to manipulate their stock prices.

Addition #4:

But folks, to compete for the jobs of the future, we also need to level the playing field with China and other competitors.

That is why I am determined to put an end to the looting of U.S. corporations by rescinding SEC Rule 10b-18—which, among other things, permits a company like Apple to do $3.5 billion in stock buybacks, trading day after trading day, without fear of stock-price manipulation charges.

Addition #5:

Intel’s CEO, Pat Gelsinger, who is here tonight — Pat told me they are ready to increase their investment from $20 billion to $100 billion.

That would be the biggest investment in manufacturing in American history.

And let’s acknowledge Mr. Gelsinger’s concern for both the future of Intel and the future of our economy when, as a condition for taking on the top job one year ago, he told Intel’s board: “We’re done with buybacks. We are investing in factories.”

Addition #6:

One way to fight inflation is to drive down wages and make Americans poorer.

I think I have a better idea to fight inflation: Lower your cost, not your wages.

And stop doing buybacks, which only serve to inflate the stock market and the bank accounts of the very rich.

Addition #7:

We pay more for the same drug produced by the same company in America than any other country in the world.

Yet, as research shows, U.S. pharmaceutical companies distribute all their profits to shareholders as buybacks and dividends.

Now, under CEO Albert Bourla, Pfizer has acknowledged the error of the company’s past behavior. As Mr. Bourla said just before the pandemic: “The reason why we don’t do right now share repurchases, it is because we want to make sure that we maintain very strong firepower to invest in the business.”

Now that Pfizer is immensely profitable from helping to deliver the Covid-19 vaccine and the Covid-19 antiviral pill, I have no doubt that Mr. Bourla still thinks that Pfizer is “a very different company” that, whatever the pressures it faces from Wall Street, will not revert to, as he put it in January 2020, “financial engineering, purchasing back ourselves.”

And guess what? The Biden administration is determined to help Pfizer help America Build Back Better by rescinding SEC Rule 10b-18.