The interview, his presentation, and the paper have since become one of my key reference points for understanding the state of China’s financial system.

Here is the interview:

I’ll emphasize the key points.

- Though China has capital controls in place, export-driven growth necessitates a fairly open current account. Wealthy Chinese households can move money out of the country by over-paying for imports, and using the excess to create a deposit account abroad.

- The PBoC has $3T in reserves, but it cannot in practice liquidate all of that. For example, some substantial fraction may be invested in shares of Chinese banks, and selling those shares could spark a banking crisis. Shih estimates that these problems kick in by about the time that outflows reach $1T.

- Shih estimates, in the main empirical contribution of the paper, that the wealthiest 1% of urban Chinese households control something like $2T–$5T in deposits. The point is that if something made them nervouse, they could drain that $1T in a hurry. These households are likely to be sophisticated enough to take advantage of the current-account porosity, and may have other ways to get money out of the country as well. It is reasonable to suspect that the next 9% of households also control substantial deposits, and may also be able to move money fairly easily.

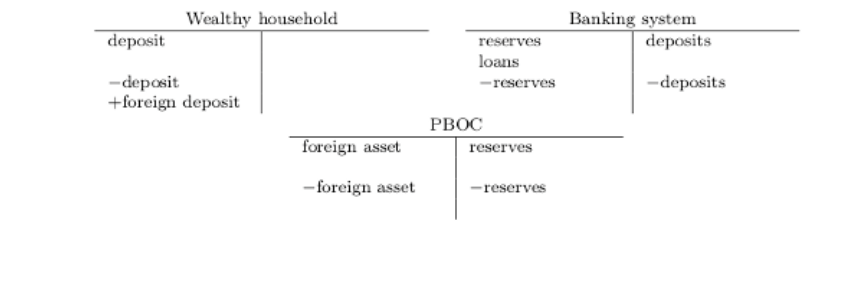

Here is how the unwinding Shih is talking about would play out, in balance sheets. (I’m omitting the balance sheet for the rest of the world.)

Depositors withdraw, and illiquid loans cannot be drawn down, so reserves are drained from the system. If funds were only being moved within China, there would be no systemic problem. But they are being moved out of country, so reserves are being drawn down for the Chinese system as a whole. This happens on the PBoC’s balance sheet.

The PBoC makes payment abroad on the banking system’s behalf by drawing down its foreign-exchange reserves, reducing reserve balances correspondingly. It could liquidate sterilization bonds as well. This payment ends up funding a foreign deposit for the household, perhaps via import invoicing. Shih estimates about $1T in deposits could leave the country in this way, and then the situation would get interesting.

All the above is Shih, as spelled out in the paper. What I take away, as I say at the end of the interview, is that Chinese policymakers are engad in a complex juggling act. They’re trying to control the exchange rate, the capital account, and fix lending and deposit rates, all at the same time. When the system starts to give, it could crumble quickly.