In a recent op-ed dated March 14, “John and Maynard’s Excellent Adventure”, Paul Krugman defends John Hicks’ original 1937 interpretation of Keynes’s General Theory that cast macroeconomics within a general equilibrium framework, but without the current insistence on the micro foundations that so concerns today’s general equilibrium macro theorists. Krugman is absolutely right. One should not be concerned with the so-called micro foundations of macroeconomics, because what is truly macroeconomics cannot be derived from micro analysis, as for example the famous paradox of thrift, whereby micro behavior gives rise to macro paradoxes that cannot be understood from choice-theoretic microeconomic reasoning.

But while we agree with Krugman’s criticism of the hordes of “micro-foundation” revisionists that now dominate economics, we are curious why he did not mention Sir John Hicks recantation of IS-LM analysis (see “ IS-LM: An Explanation”, Journal of Post Keynesian Economics, 3 (2) (Winter 1980-81);). Many of us remain deeply sceptical about the usefulness of the IS-LM framework for interpreting a real world characterized by uncertainty, crises, and institutional transformations that hardly bring the economy towards any equilibrium, never mind “general” equilibrium. But even if we abstract from these complications with the usual excuse of rendering the analysis simple for pedagogic purposes, the original Hicksian IS-LM model and its various textbook extensions (usually constructed with some sort of Phillips curve add-on) are extremely problematic. The difficulties have really little to do with the view that it’s too aggregative by representing only three markets: product, money, and bond markets – which is the criticism to which Krugman seems to be pre-emptively alluding in his article.

The first and obvious problem is that, even in the three-market aggregative model, there can never be such a thing, even at the conceptual level, called general equilibrium. To get that we must presume that there are independent functions of investment and saving and, at the same time, independent demand and supply functions for money. But one of the most basic criticisms that Keynes himself had come to recognize immediately after writing the General Theory is that the supply of money is not some exogenous variable that can be independently pitted against a distinct demand for money function. In a sophisticated monetary economy, the supply of money must be treated as a purely endogenous variable as many modern post-Keynesians and also neo-Wicksellians have come to recognize. Hence, the idea of money market equilibrium is meaningless, since one cannot conceptually ever be out of equilibrium when the two cannot be defined independently of one another.

However, the problem also arises on the product market side. Keynes had long debated the issue of I=S equilibrium, as for instance, also in 1937, with Swedish economists who made use of notions such as ex ante (or planned) investment and ex ante saving . While Keynes said that one can perhaps give some meaning to ex ante investment (in terms of business enterprises planning capital expenditures), at the macroeconomic level one cannot meaningfully describe saving as being anything that can actually differ from investment. Admittedly, this leads to a debate about the meaning and nature of the multiplier as a “disequilibrium” concept. But our point is that if the “supply” of money can never be independent of the “demand” for money and if saving can never be independent of investment, then what use is the IS-LM analysis that presumes exactly that independence?

Moreover, if one were to postulate an infinitely elastic LM curve (as one can infer from David Romer, “ Keynesian Macroeconomics without the LM Curve”, Journal of Economic Perspectives, 2000;) to deal with this lack of independence between the money demand and supply, then the question is what insight does the latter construction provide? It seems that everyone except Paul Krugman believes that short-term interest rates are policy determined, and that they are not set in the way the traditional IS-LM analysis suggests. This means that an increase in investment (entailing a rightward shift of the IS curve) will not lead to an increase in short-term interest rates unless the central bank chooses to raise its central bank rate. Moreover, if the LM curve is flat at any level of interest rates, then what characterizes a liquidity trap and what is it? It certainly cannot be the traditional “flat” lower portion of an otherwise upward-sloping LM curve. Krugman’s liquidity trap is an LM curve that is flat at the zero rate of interest. But what does the IS-LM model have to say about long-term rates of interest? Krugman leaves us in the dark here. And what can the IS-LM model tell us about how the central bank is able to control and set short-term interest rates and what can it tell us about the consequences of quantitative easing on real output or price inflation? We believe that this model cannot really teach us anything about these issues; one needs an institutional analysis, not a rudimentary and misleading instrument.

Keynes himself was ambivalent about the role of interest rates in determining fixed capital formation (with his contrasting views in chapters 11 and 12 of the General Theory) and few would argue that business investment is strongly sensitive to changes in the rate of interest, as depicted in the traditional textbook loanable funds model. Ironically, nowadays, it is household spending on consumer durables and housing that is much more highly interest elastic and this feature is often muddied in the way this latter spending is represented in the “I” portion of the IS relation.

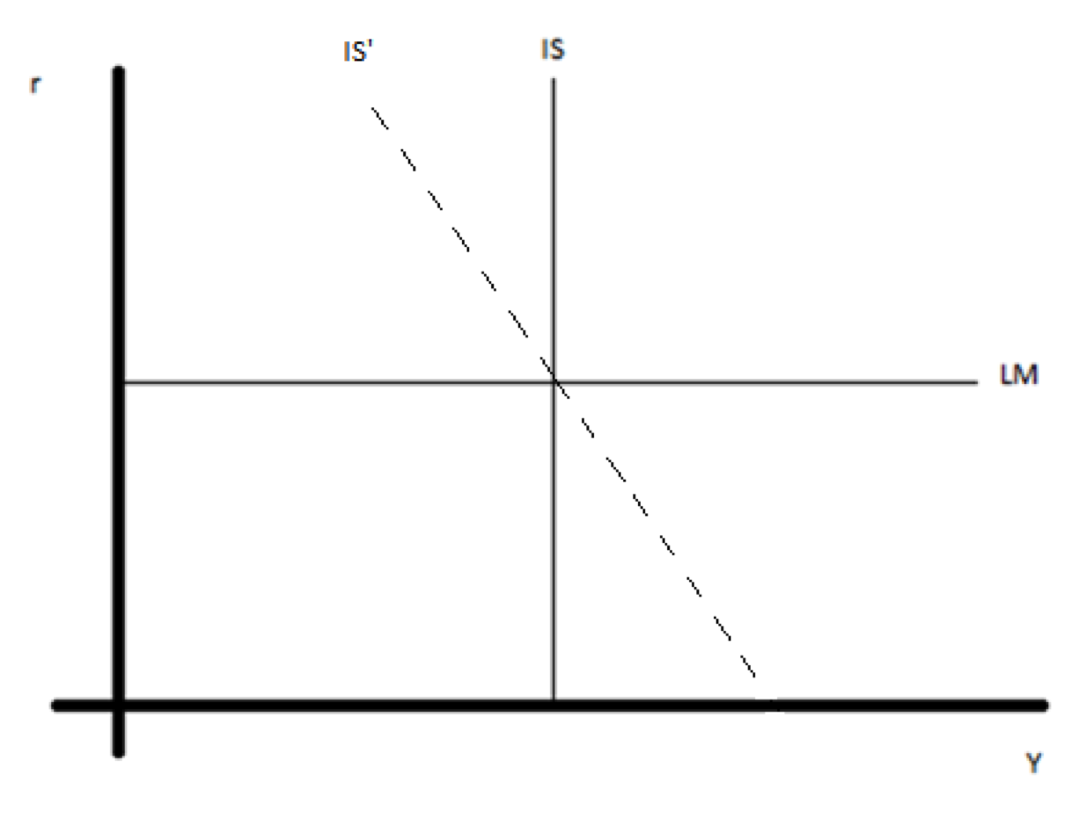

Heterodox economists have traditionally rejected the IS-LM approach for many such reasons; but, even if one were to hold one’s nose, in an uncertain world in which investment is governed by animal spirits (and therefore I being interest inelastic unless inclusive of household spending) and in a world of endogenous money, at best, the IS curve can be represented by a vertical line (or a more elastic relation when including household spending, an IS’ curve). In much the same way, the LM curve can be represented by a horizontal line at any level of interest rates set by the central bank (as shown in the figure below). What insights can such a tool of analysis really offer economists? It suggests that an increase in autonomous spending will generate increases in output without any “crowding out” effect arising through higher interest rates. But one hardly needs an IS-LM framework whose truly central feature is the role played by interest rates to infer that! In our humble opinion, Hicksian IS-LM analysis cannot offer us very much and this is why even Sir John Hicks himself eventually abandoned it almost 35 years ago. And so should Paul Krugman!