A response to Paul Krugman’s recent essay on U.S. and European productivity opens onto a broader question. If the standard metrics point in conflicting directions, perhaps the problem lies less with the economies than with the measures themselves.

In a July 5 essay on economic performance in Europe and the United States, Paul Krugman compares two metrics, real GDP per capita over time and a sequence of Purchasing Power Parity income measures. He notes they give inconsistent results: one shows the US moving sharply ahead, the other shows Europe keeping pace. He asks, “which of these stories is true?” In addressing this question, Krugman overlooks the possibility that the correct answer might be, “neither one.”

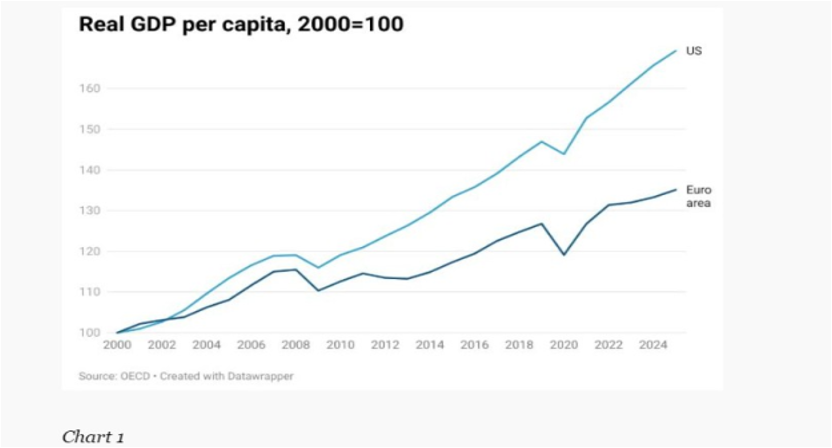

Consider Krugman’s Chart 1, according to which the “average” American is over sixty percent richer, in real terms, in 2026 than in 2000, the peak year of the internet boom. Sixty percent. That’s in “real” terms, meaning food, clothing, cars, houses, vacation travel, sporting events… the works. Really? Meanwhile real median weekly earnings have risen, according to the St. Louis Fed, by only 10.5 percent.[1] Krugman’s number is either false, or so distorted by the skewed income distribution to be meaningless. Or possibly, both.

Krugman touches on an important reality when he notes the contribution of the tech sector to measures of US productivity growth, and the driving role of aggressive price adjustments in generating high measured rates of “real growth” in tech. But why is US tech productivity so high? Krugman writes that the US has “most or all global tech production.” Really? Taiwan Semiconductor Manufacturing Corporation doesn’t count? And what about the 250,000 who work for FoxConn in Shenzen? Could it be that US productivity in tech has something to do with the fact that US tech companies (like Apple) outsource the dirty work to China, keeping the high value-added activity at home? It is not as though there are that many different ways to make a semiconductor; what there are, are different ways to organize the supply chain.[2]

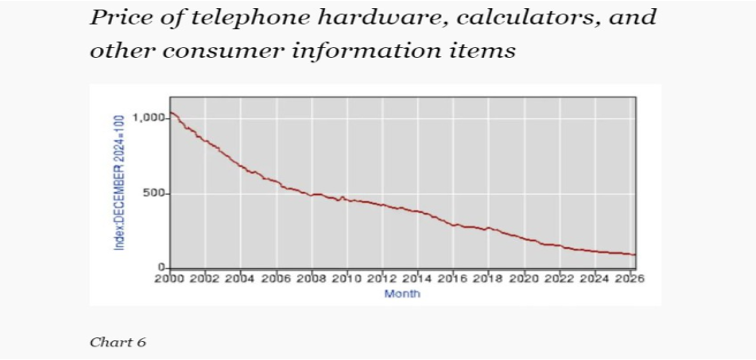

On the issue of tech prices, Krugman writes as though his Chart 6 was the adjusted price of a “new” product – smartphones. But it isn’t. The caption reads: “telephone hardware, calculators, and other consumer information items.” This upsets the notion that the smartphone is “new.” Sure, the package is a novelty of recent decades. But everything mine does – phone, fax, mail, camera, tape recorder, TV, calculator, newspaper, magazines, video games, meetings, travel agent, banking – existed and had its counterpart in the last century’s analog world. The price declines measured are from the cost of all those separate gadgets, now consolidated into a pocket.

So, sure, the price of all those things has fallen, and if you treat them as though they still have the same weight in consumption as they did back in 2000, we all look (somewhat) richer. But all those functions have less economic value today than they did a quarter-century back.[3] If you start from today’s consumer basket, that is, from the benchmark that will eventually be adopted, you’ll find that tech items now constitute a smaller share of our budgets (and of GDP) than they used to, and their weight in the index after the benchmark revisions will be less. Today’s incomes go instead to the many things that are more expensive than they were in 2000: energy, tuition, rent, insurance, interest, human services – the list is long. And that’s the real paradox of information technology: the big advances fade out of the transactions that we call our economy. And so, they also eventually fade from the output data. This is called the index-number problem; it’s a paradox, and there’s no perfect solution. What we do know, is that to use the base-year weights generates exaggeration.

To explain his other measure, purchasing power parity, Krugman adverts to the “Big Mac Index,” – the price of what he calls a “standardized item sold all around the world.” Except it isn’t. In the US, McDonalds is a roadside fast-food joint, an aging artifact of the highway culture. In Europe, as any tourist knows, it’s generally closer to a local cafe. Restaurants are an experience, and so the Big Mac in the two continents is not the same — and that’s quite apart from Europe’s VAT and public health policies, and their effect on European prices. Without deprecating the International Comparison Project, PPP comparisons are bedeviled with such quality problems.

Krugman is a Europhile who believes in the old formula of high regressive taxes and big social benefits, and he evidently thinks this formula still applies. I’m guessing he wasn’t warned, as I was in Greece in 2010, “don’t go to a public hospital, you’ll leave in a box.” Possibly he hasn’t visited French universities where the faculty have no offices and the stalls lack toilet paper. I wonder if he’s tried to travel, lately, on German trains, undermaintained thanks to the “debt brake.” Not to mention the waits at Britain’s National Health Service or the condition of her aging railbeds. Capturing all these quality differences in a PPP measure is, well, just about impossible.[4]

Krugman is right to say that the comparisons he cites use “completely standard methods.” I make no criticism of the statisticians struggling to measure economic outcomes in a changing world. The problem is that the methods are not up to the task.[5]

Still, a little common sense might help. If average Americans had really gotten over fifty percent richer in 2024 than in 2000, would Donald Trump be President today? If “Europe” were not stagnating, would Germany’s AfD, France’s RN, and the UK’s Reform be on the cusp of power? Something is clearly wrong with measures that show the US in a moment of unparalleled prosperity, and equally with measures that show Europeans – although not so rich – enjoying the same degree of improvement in their lives. Economists with their noses in these numbers should, perhaps, get outside more.

So what about the US and Europe? Neither is exactly poor, although the differentials across Europe – between Denmark and Portugal, say, or Sweden and Bulgaria, are far larger than those across the American states.[6] But anyone who has been there knows that, compared to China, both Europe and the US are in relative decline. European and American lives are not so special anymore. And China is about twice as large as Europe and America combined.

Further, there’s a good case that Europe’s relative decline is faster, for now. You can see this in the ongoing contraction of major European industries, notably in Germany and especially in automobiles, chemicals, pharmaceuticals – the energy-intensive sectors that have dominated German exports. The US economy is propped up, as Europe’s is not, by the Permian Basin, the stock market, and a construction boom in data centers. Europe lacks these crutches, and has the added disadvantages of a delusional energy policy, a mad rush to rearm, and Sinophobia even more severe than America’s.[7] These things, along with the better reputation of US Treasury debt as a safe haven, may help explain the decline of the euro compared to the dollar, which (contrary to Krugman) is, at least in some eyes, an actual indication of relative decline.

Europe’s economic strategy was locked-in by the neoliberal ideology that prevailed at the time the Eurozone was formed. This strategy has for decades been an exercise in self-harm. The harm has been compounded by Europe’s deference to American geopolitical objectives and failure to define its own interests in the modern world. The notion that Europe only needs more “reform” (flexible labor markets, later retirement, fewer public services, debt brakes…) and more “integration” is beyond absurd. Europe needs peace with Russia, cooperation with China, and a regional development strategy – aimed at places like Romania and Bulgaria that have stagnated since the collapse of the socialist bloc – a New Deal like the one that rescued the American South in the 1930s. For that, and to save its industry from collapse, Europe needs Russian and Middle Eastern gas and oil, and for that, it needs somehow to stop the war in Ukraine and the US/Israeli assault on Iran.

- 1. According to the same source, real median household income is up 16.7 percent over the same period.

- 2. Major European tech companies do outsource to China, but the share is less than has been the case for US companies.

- 3. The basic determinants of economic value are scarcity and the degree of monopoly power, both of which have declined in the information sector. This is issue is discussed in my book with Jing Chen, Entropy Economics: The Living Basis of Value and Production (Chicago, 2025).

- 4. Quality problems are not unique to Europe; any observer can identify similar complaints on the American side. The point is that valuing all of the distinctions in the vast part of our economic lives that do not consist of directly comparable goods and services is an intractable problem, which sending teams to record prices in stores cannot solve.

- 5. John Maynard Keynes makes the same point, writing in The General Theory that “To say that net output is greater, but the price-level lower, than ten years ago or one year ago, is a proposition of a similar character to the statement that Queen Victoria was a better queen but not a happier woman than Queen Elizabeth – a proposition not without meaning and not without interest, but unsuitable as material for the differential calculus.” The entire passage, in Chapter 4 on “The Choice of Units,” should be engraved on the desk of all those trying to make sense of index numbers. Keynes concluded that he should restrict himself to “two fundamental units of quantity, namely, quantities of money value and quantities of employment.”

- 6. Denmark has about twice the per capita income of Portugal, and Sweden almost three times that of Bulgaria. There are no pairs of US states whose average income differential is as much as two to one. As for the very wealthy, the US has more of those, whose net worth is known. In Europe, they are more discreet.

- 7. Which region is more afflicted by price-gouging is a question that I'll leave to Isabella Weber of the University of Massachusetts – Amherst, the recognized expert in this area.