Both before 2008 and today, there’s a disturbing tendency in Washington to not take mortgage fraud seriously

In this post I will focus primarily on how fraud in the origination and distribution portions of the privately securitized mortgage supply chain contributed to the financial crisis, because it provides a salient example of how widespread and deeply rooted in markets the economics of deception has become, as well as how difficult it is to protect ourselves from it. Losses in private mortgage backed securities (MBS) were at the heart of the financial crisis of 2007-2008. The failure of the mortgages underlying these securities caused substantial losses for the institutions directly invested in them or which held derivatives based on them, as well as loss of wealth for the communities in which foreclosures occurred. The private MBS market suffered $500 billion in losses from foreclosure from 2007-2012, which was disproportionately borne by poor communities that never recovered from the crisis (Herndon 2017; Mian and Sufi, 2017). A large body of empirical research has now convincingly documented how mortgage fraud contaminated all portions of this supply chain (Griffin and Maturana, 2016; Piskorski, Seru and Witkin, 2015; Garmaise, 2015; Jiang, Nelson and Vytlacil, 2014; Black, 2013; Ben-David, 2011). This research has shown how these mortgages were originated with fraudulent and negligent practices, and how these abusive practices were then concealed from and misrepresented to investors who purchased securities based on these mortgages.

The private label originate-to-distribute supply chain consisted of institutions which originated mortgages and then sold these loans to investment banks for distribution. Investment banks then packaged mortgages into securities, obtained ratings from ratings agencies, and sold the securities to investors. Finally, a servicer would process loan payments and manage defaults on behalf of the investors. Often a single large institution, such as Wells Fargo, would be responsible for all parts of this supply chain, but it was more common for these functions to be handled by separate institutions.

The basic issue underlying misrepresentation of MBS quality in the distribution portion of the supply chain was succinctly summarized in a recent ruling by District Judge Denise Cote,

“This case is complex from almost any angle, but at its core there is a single, simple question. Did the defendants accurately describe the home mortgages in the Offering Documents for the securities they sold that were backed by those mortgages? Following trial, the answer to that question is clear. The offering documents did not correctly describe the mortgage loans. The magnitude of falsity, conservatively measured, is enormous.”[1] [emphasis added].

What sellers of MBS concealed from investors was a wholesale breakdown in underwriting standards at origination, which included outright falsification of borrower financial information. However, the sale of loans that were originated with fraudulent practices, or simply negligent underwriting, typically violated market regulations and contractual obligations. These rules require the accurate disclosure of loan quality. Of course, if these practices were disclosed, the securities would obviously not have been marketable. Loan officers and underwriters who originated loans for private securitization used a variety of techniques to falsify borrower financial information such as inflation of appraisal values, failure to report second liens, income overstatement, and misreported owner occupancy status. This was done to qualify borrowers for larger loans than they would otherwise be able to obtain and had the effect of making loans more risky by increasing borrower leverage.

The direct falsification of borrower financial information was largely committed by loan officers and underwriters within the industry, who coached borrowers on the specific ways to falsify their information, rather than by borrowers who defrauded otherwise honest lenders. For example, based on investigations and fraud reports, the FBI found that 80% of fraud cases involved collusion or collaboration with industry insiders (FBI, 2007). For example, a loan officer from Ameriquest explicitly described deceiving borrowers who were not comfortable with falsifying their information. He stated that, “Every closing was a bait and switch, because you could never get them to the table if you were honest,” and further elaborated, “There were instances where the borrower felt uncomfortable about signing the stated income letter, because they didn’t want to lie, and the stated income letter would be filled out later on by the processing staff.”[2] Perhaps most infamously, workers at another Ameriquest branch dubbed their break room the “Art Department” because it contained all the tools needed to falsify documents (Hudson, 2010).

A recent body of empirical research has also confirmed that misrepresentation in private MBS was a widespread, systematic problem, rather than solely isolated incidents. For example, using conservative measures Griffin and Maturana (2016) find that 48% of loans that were privately securitized contain at least one of three relatively easy to quantify forms of fraud: appraisal inflation, unreported second liens, and misreported owner occupancy status. They find that loans with one of these forms of fraud were 51% more likely to become delinquent. The problems with misrepresentation in this market could be reasonably described as a “market for lemons.” The term “lemon” refers to a car which is poor quality, or more generally to any product that is poor quality. A market for lemons is a market where good and bad quality products are sold, but where there is asymmetric information so that buyers cannot know beforehand whether they are buying a good or bad product.

In a market for lemons there is what is known as a Gresham’s dynamic, where bad products tend to push out good products because good and bad products must sell at the same price (Akerlof, 1970). To put it slightly differently, it is very difficult to be an honest player in a crooked game. Over the course of the housing bubble, empirical research has clearly documented that bad practices in this market had largely pushed out good practices, because a “significant degree of misrepresentation exists across all reputable intermediaries involved in the sale of mortgages,” [emphasis in original] (Piskorski et al., 2015). This Gresham’s dynamic is one of the most dangerous market pathologies, because the market will eventually fall apart when bad practices sufficiently crowd out good practices. There was a wholesale collapse of funding for private MBS when these scandals were uncovered. Almost a decade later the private market has still not recovered to a point where it would be able to provide the funding needed to support the housing market. It is not a gross exaggeration to say that since the financial crisis the government has essentially become the housing market because the government guarantees roughly 80% of mortgages.[3] Had the government not provided historic support for the secondary market, mortgage finance for households would simply not be available (Levitin, 2014; Frame et al., 2015).

The misrepresentation of residential mortgage-backed security quality provides a salient example of how the deception enabled by asymmetric information is much more widespread and persistent than commonly acknowledged, so that we need to consistently guard against fraud. Prior to the crisis, a common position among economists was that prohibitions against fraud were simply not necessary, because asymmetric information structures were not thought to be widespread or serious enough to compromise economic activity. Moreover, even if asymmetric information was widespread, markets provided powerful incentives to prevent fraud, such as reputation. In a now infamous example from the years leading up to the financial crisis, when Brooksley Born, then head of the Commodities Futures Trading Commission, warned Alan Greenspan about the need to prevent fraud, he replied that there wasn’t a need for a law against fraud, because if someone was committing fraud, “the customer would figure it out and stop doing business with him.” As a lawyer with considerable experience defending defrauded financial clients, she thought that, “this made no sense,” and that, “the existence of fraud prohibitions was critically important.”[4]

This encounter shows how a deep understanding of the widespread nature of the economics of deception is important not only for preventing fraud in the future, but also for understanding how markets actually function in practice. Indeed, Greenspan should not have been surprised by misrepresentation of MBS quality, for the simple reason that it also occurred in all six previous attempts at introducing private mortgage securitization in U.S. history. These problems were so severe and consistent that an economic historian, who was writing in 1995 before the recent financial crisis uncovered spectacular scandals, concluded his history of mortgage securitization with a stern warning of these dangers. He argued that each of the early failures in private mortgage securitization in the U.S. before the 1930s, “provided evidence that private securitization structures rest on a razor’s edge. There is always some limit to the amount of default risk that can be absorbed in a privately financed securitization structure, and whenever that threshold is broken the severe informational problems that are inherent in mortgage securitization appear in full force. We have seen that insiders regularly exploited their informational advantage in these situations before 1930 and, by doing so, imposed much larger losses on investors than would have resulted from default risk alone,” (Snowden, 1995).

Figure 1: Cutting Red Tape, as Tragedy

The history described above provides strong reasons to be constantly vigilant against fraud. However, it will be useful to conclude with a cautionary warning that preventing fraud will likely be difficult due to regulatory capture from both ideology and perverse incentives. Greenspan, who was the chief financial regulator at this time, could be described as “ideologically” captured, in that his worldview did not recognize the need for anti-fraud enforcement, because he believed the free market already provided powerful incentives against fraud. Due to this, he refused to use his rulemaking and other supervisory powers to prevent the worst origination practices (Levitin and Wachter, 2013; Taub, 2014).

Another key enabler of mortgage fraud was that regulators faced incentives which promoted a “competition in laxity” or “race to the bottom.” These incentives helped the worst abusers “weaponize” regulatory agencies, by using these agencies to prevent investigation into their practices by other agencies that were not captured. The Office of Thrift Supervision (OTS) was likely the most spectacular example of competition in laxity from the 2007-2009 financial crisis. The OTS faced perverse incentives because its funding was based on a levy on the amount of assets under its supervision. The OTS therefore had an incentive to increase the amount of assets under its regulation so that it could increase its funding. To do so, it offered banks less stringent regulation, as advertised in a now infamous 2003 photo from the FDIC annual report, shown in Figure 1. This photo shows the director of the OTS, James Gilleran, posing with three bank lobbyists, to advertise the lax approach of the OTS by taking a chainsaw to federal banking regulations, underneath a banner which reads “Cutting Red Tape.” The OTS supervised the institutions responsible for the largest failures of the crisis such as AIG, Countrywide, Indymac, Lehman Brothers, and Washington Mutual, and actively prevented investigations into their worst practices. The OTS was abolished for this negligence following the financial crisis (Taub, 2014; FCIC, 2011).

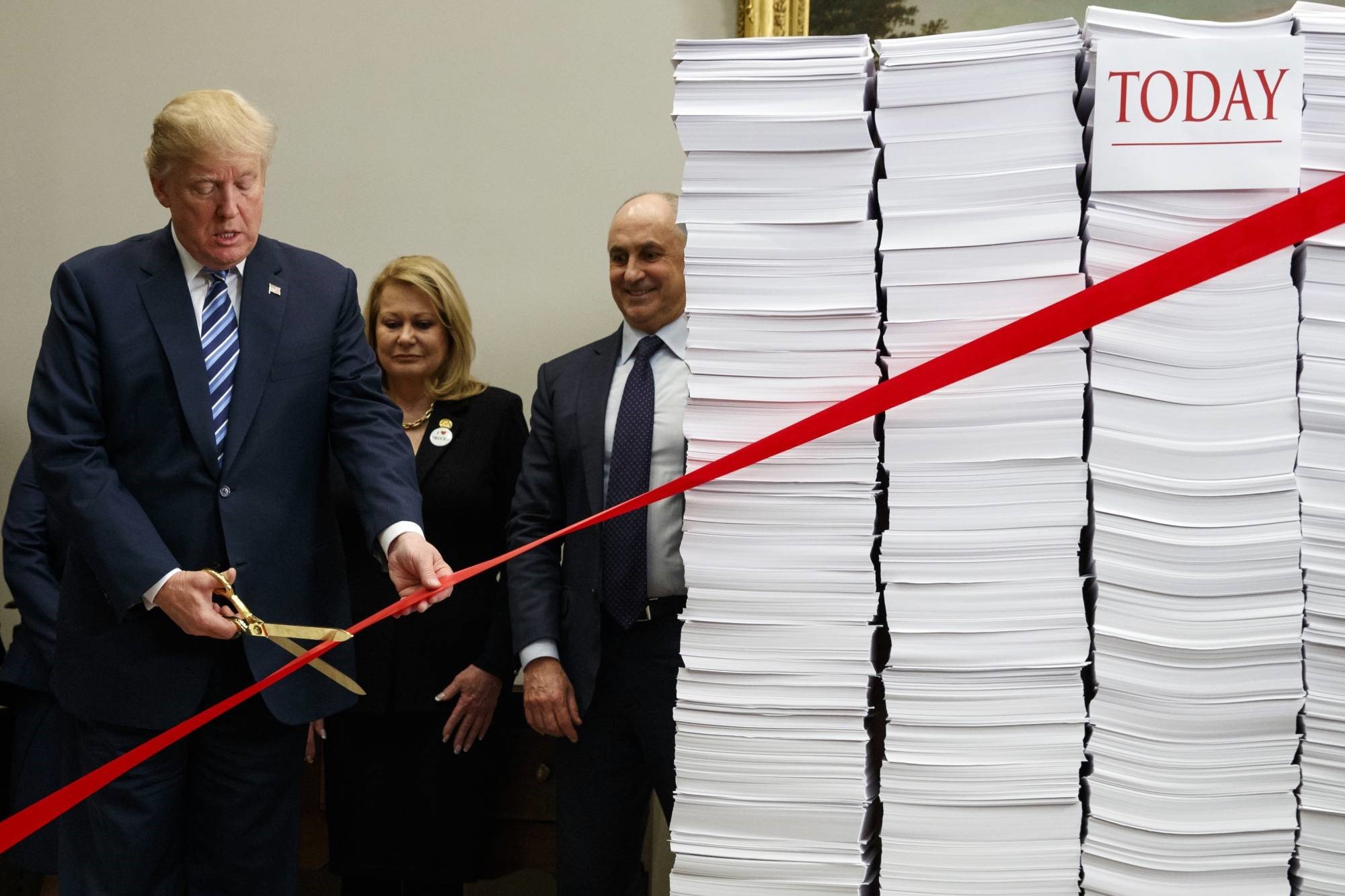

Figure 2: Cutting Red Tape, as Farce

Unfortunately, the spirit of cutting red tape is alive and well in the current administration, as shown below in Figure 2. There is a high danger that our regulatory agencies, including the ones created to address the problems that led to the financial crisis, are currently being weaponized. An example of this is the choice of Mick Mulvaney to replace Richard Cordray as the head of the Consumer Financial Protection Bureau, despite the fact that Mulvaney has stated that the agency was a, “sick, sad joke,” and that, “some of us would like to get rid of it.”[5] Unfortunately, recent history has provided us with the costly lesson that a prudent person should reach for their wallet whenever they hear those responsible for enforcing the rules talk about cutting red tape. We forget this lesson at our own peril.

References

Akerlof, George. 1970. “The Market for “Lemons”: Quality Uncertainty and the Market Mechanism.” The Quarterly Journal of Economics, 488 500.

Ben-David, Itzhak. 2011. “Financial constraints and inflated home prices during the real estate boom.” American Economic Journal: Applied Economics, 55 87.

Black, William K. 2013. The Best Way to Rob a Bank is to Own One: How Corporate Executives and Politicians Looted the S&L Industry. University of Texas Press.

FBI. 2007. “Financial Institution Fraud and Failure Report Fiscal Years 2006 and 2007.”

FCIC. 2011. “The Financial Crisis Inquiry Commission Report: Final Report of the National Commission on the Causes of the Financial and Economic Crisis in the United States.” Financial Crisis Inquiry Commission.

Frame, Scott, Andreas Fuster, Joseph Tracy, and James Vickery. 2015. “The Rescue of Fannie Mae and Freddie Mac.” Federal Reserve Bank of New York Staff Report 719.

Garmaise, Mark J. 2015. “Borrower Misreporting and Loan Performance.” The Journal of Finance.

Griffin, John M, and Gonzalo Maturana. 2016. “Who Facilitated Misreporting in Securitized Loans?” Review of Financial Studies.

Herndon, Thomas. 2017. “Liar’s Loans, Mortgage Fraud, and the Great Recession.” Political Economy Research Institute Working Paper.

Hudson, Michael W. 2010. The Monster: How a Gang of Predatory Lenders and Wall Street Bankers Fleeced America—and Spawned a Global Crisis. Macmillan.

Jiang, Wei, Ashlyn Aiko Nelson, and Edward Vytlacil. 2014. “Liar’s loan? Effects of origination channel and information falsification on mortgage delinquency.” The Review of Economics and Statistics.

Levitin, Adam. 2014. “Postal Banking: Maybe Not So Crazy After All?” American Banker.

Levitin, Adam J, and Susan M Wachter. 2013. “The Public Option in Housing Finance. UC Davis Law Review, 46: 1111 1655.

Mian, Atif, and Amir Sufi. 2017. “Fraudulent income overstatement on mort- gage applications during the credit expansion of 2002 to 2005.” The Review of Financial Studies.

Piskorski, Tomasz, Amit Seru, and James Witkin. 2015. “Asset Quality Misrepresentation by Financial Intermediaries: Evidence from the RMBS Market.” The Journal of Finance.

Snowden, Kenneth. 1995. “Mortgage Securitization in the United States: Twentieth Century Developments in Historical Perspective.” In Bordo and Sylla, Anglo-American Financial Systems.

Taub, Jennnifer. 2014. “Other People’s Houses.” Yale University Press.

Footnotes

[1] From ruling in Federal Housing Finance Agency v. Nomura Holding America, May 11th, 2015. Accessed on June 26th, 2015 from: https://s3.amazonaws.com/s3.do…

[2] National Credit Union Administration Board v. Wells Fargo Bank, National Association, 2014.

[3] Fannie Mae and Freddie Mac have guaranteed or directly held 60% of mortgages, while the FHA/VA insures 20% .

[4] Accessed August 7th, 2018 from: http://www.washingtonpost.com/…