A look at the large role the trade deficit of the United States has played since the 1980s.

In the aftermath of the 2008 crisis, renewed attention has been directed to the accumulation and persistence of current account imbalances between countries and to the large role the trade deficit of the United States has played in this area since the 1980s.

Although economists like Wynne Godley had been concerned about the long-run sustainability of this trend before 2008, the need for “rebalancing” trade has emerged as an important part of the post-crisis economic debate. Why is this?

After the crisis many people pointed to the U.S.’s increasing current account deficit as a factor leading to the breakdown of the U.S. economy, so rebalancing is seen as a requirement to achieve long-run stability in the system. In particular, large net inflows of foreign capital, a counterpart of outsized current account deficits, have been blamed by many for the self-reinforcing spiral between asset prices and private sector leverage that proved unsustainable after the crash.

Additionally, as Joan Robinson described in 1966, in a context of falling levels of world employment and international trade, each country is tempted to try to save for itself a larger share in the shrunken total of world activity, even at a cost to its neighbors. As a result, surplus countries are blamed for exporting their own unemployment to the rest of the world.

It is largely for the second reason that in the past five years countries have engaged in unilateral attempts to avoid currency appreciation via loose monetary policy, capital controls, or direct interventions in the market, as well as in coordinated efforts (mostly led by deficit countries) to enforce an international mechanism for rebalancing. The U.S.-led proposition of a cap of 4% of GDP on current account surpluses and deficits made at the 2010 G20 meeting is the most prominent example of the latter.

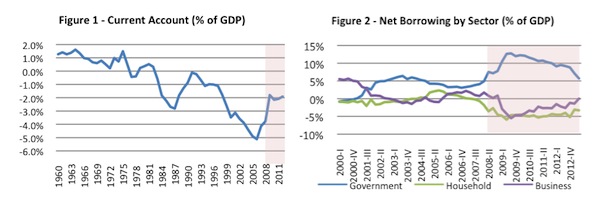

Five years later, as shown in Figure 1, the U.S. current account deficit has decreased substantially, having stabilized at about 2% of GDP, which roughly corresponds to the figure in 1998. Only after the Plaza Accord of 1985, when the dollar depreciated relative to the yen, had the U.S. experienced a comparable rebalancing. However, a closer look at recent data reveals that:

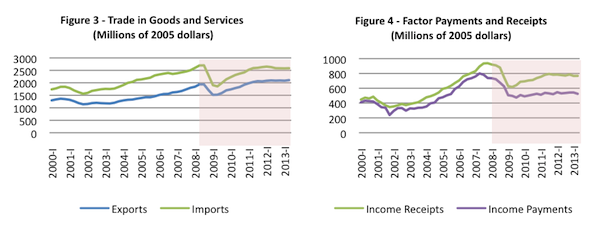

- The improvement of the current account in 2009 was mainly due to a sharp fall in imports (Figure 3).

- In spite of faster growth in imports than in exports in recent years, the current account deficit has remained stable since the increase in factor income receipts was not accompanied by an increase in factor income payments (Figures 3 and 4).

- Both the household and business sectors, which had decreased their net borrowing substantially in 2008, have already reached their pre-crisis levels. The government deficit, which had substantially increased at first to “compensate” for private sector deleveraging, is already lower than before the crisis (Figure 2).

So even if the U.S. current account has improved in the past five years, these observations suggest that neither of the above-mentioned goals for rebalancing, namely its short-run positive effects on aggregate demand or its long-run implications for the stability of the economy, have been accomplished.

When it comes to the goal of short-run recovery, rebalancing seems to have arisen from a contractionary adjustment via imports rather than an expansionary adjustment of exports. When it comes to the long-run stability objective, Godley’s sectoral balances show that we are now back to the previous pattern of debt-led private spending. As a last point of concern, in recent years the stability of the current account deficit seems to have relied solely on the low level of factor income payments to the rest of the world. But this dynamic will soon come to an end as soon as the Federal Reserve abandons its expansionary monetary policy, causing Treasury debt to generate higher yields.

Looking to the future, it is true that the safe-haven status of U.S. dollars and government bonds, as well as the debt-led features of the country’s domestic demand, may once again allow the U.S. to grow more while its current account deteriorates than it grew in the past five years of apparent rebalancing. But, if the lessons of 2008 are followed, the true rebalancing needed for the system’s long-run stability must involve deeper changes in the U.S. growth regime.

A first aspect of this shift should be a redistribution of income both toward wages and to the bottom wage quintile. Ultimately this would be an effective way to avoid another debt-led spiral in the household sector while keeping consumption as a key driver of aggregate demand.