Thomas Ferguson is the Research Director at the Institute for New Economic Thinking. He is Professor Emeritus at the University of Massachusetts, Boston and Senior Fellow at Better Markets. He received his Ph.D. from Princeton University and taught formerly at MIT and the University of Texas, Austin. He is the author or coauthor of several books, including Golden Rule (University of Chicago Press, 1995) and Right Turn (Hill & Wang, 1986). His articles have appeared in many scholarly journals, including the Quarterly Journal of Economics, International Organization, International Studies Quarterly, and the Journal of Economic History. He is a member of the editorial board of the International Journal of Political Economy and a longtime Contributing Editor at The Nation.

Thomas Ferguson

By this expert

The Knife Edge Election of 2020: American Politics Between Washington, Kabul, and Weimar

Covid and BLM protests were key to Biden’s victory

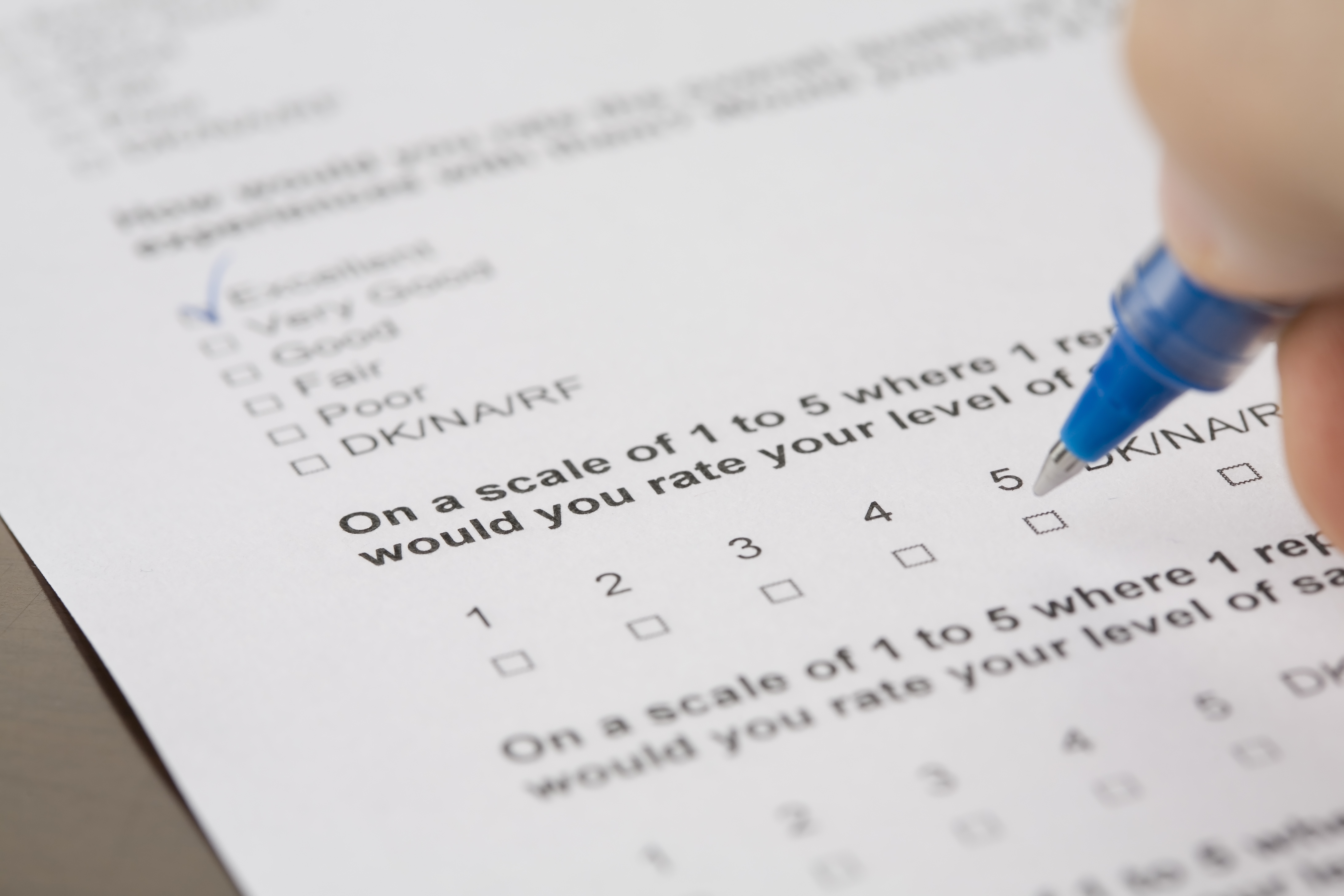

Public Opinion on U.S. Trade Policy: Time to Ask Better Questions

Open-ended polling responses reveal considerably more complexity – and more ambivalence and negativity – in Americans’ views of international trade than has been inferred from widely cited closed questions

Ambivalence About International Trade in Open- and Closed-ended Survey Responses

Open-ended polling responses reveal considerably more complexity – and more ambivalence and negativity – in Americans’ views of international trade than has been inferred from widely cited closed questions

New CDC Guidelines to Reopen Schools Could be Dangerous

School re-opening push based on outdated science is poorly timed in face of coronavirus resurgence

Featuring this expert

Thomas Fricke has an article in Der Spiegel citing an INET study showing that prioritizing health in the pandemic has led to better economic outcomes

“Calculations by Phillip Alvelda, Thomas Ferguson and John Mallery, which have just been published by the Institute for New Economic Thinking, suggest how scary the choice between life and business is in the corona crisis . A comparison of all possible countries and strategies over the past year then gave a fairly clear picture: Those who consistently aimed to stop the epidemic through hard lockdowns have significantly fewer deaths - even if they initially suffered greater economic damage; while it is with countries like the UK it was exactly the opposite, which initially hesitated with the lockdown and raised all the more money to avoid economic damage. With the fatal result that precisely because of this, the second wave became all the more violent - and economic output collapsed in the end. Conclusion of the study: The more negligent governments allow the pandemic to work in order not to harm the economy, the more the economic costs will pile up over time and ever new waves. Almost no matter how hard these rulers and central bankers try to counter it with economic stimulus programs. The damn virus finds activity between people (also economic) pretty good.” — Thomas Fricke

Thomas Ferguson is quoted in Alternet on Georgia's senate election

“Ferguson, whose research has shown that candidates who raise more money stand a much greater chance of winning election, added that “when you get that much money pouring into the election, it means that you have all these investors who decide which election is ‘worth it’ and that tends to pull even liberal democrats to the right. It is a somewhat subtle effect but a very real one and clearly an anti-democratic consequence of the system.” — Andrew Kennis

INET study is cited in the Socialist Worker

“Rich economies have more resources to spare to prioritise saving lives. And Wolf reproduces the Institute for New Economic Thinking’s now famous chart that refutes the idea there is a “trade-off” between saving the economy and saving lives. On the whole, those states that prioritised saving lives also lost less economic output. China is the standout case. But it isn’t just about how rich an economy is. The same chart shows that the states that suffered the biggest losses of lives and output include Italy, Britain, Spain, and France. The US and Belgium aren’t far behind.” —Alex Callinicos

INET article cited in NTV on how to handle the pandemic this winter

“A look around the world shows that so far no country has managed to effectively protect its risk groups when the number of infections is high - Sweden at the beginning of the pandemic or Switzerland in the second wave also had to pay for their special routes with many deaths. And if such a strategy fails, you have wasted valuable time and may find yourself confronted with an infection that is completely out of control. This would mean a collapse of the health system with all the ensuing consequences. This also includes immense damage to the economy. This is also confirmed by a study by the Institute for New Economic Thinking. Those who reacted belatedly or wavered between strategies not only had very high casualties, but were also the most damaging to their economies, it said. The authors cite Great Britain as a negative example.” — Klaus Wedekind