Introduction

In July 2018, Professor William Lazonick came to Argentina and gave a lecture called “The Investment Triad: Productive Capabilities and Sustainable Prosperity” based on INET’s paper “Profits Without Prosperity: How Stock Buybacks Manipulate the Market, and Leave Most Americans Worse Off” (2014).

I had the opportunity to discuss the paper and focused on the differences between developed countries (especially the U.S.) and underdeveloped countries (mainly Argentina) regarding the transformations in industrial relations that have occurred since the seventies. In this article, I offer a summary of Lazonick’s arguments and my application of his analysis—namely, the impact of labor and capital on the wage share and the composition of aggregate demand in Argentina.

Lazonick’s Argument of the Corporate Allocation Regime

A key element of Lazonick’s analysis of the unfolding of American capitalism was drastically modified in the 1980s. Until then, the allocation regime was linked to a “retain-and-reinvest” (“RR regime” from now on) and, since then, to a “downsize-and-distribute” strategy (“DD regime”).

According to Lazonick, during the “RR regime” companies retain their profits and reinvest them to grow and to increase productive capacities. A central theme was also investing in workers through higher wages, working conditions, and training since a company’s competitive edge was embedded in them. This regime allowed the largest U.S. corporations to become world leaders of their sectors, innovative enterprises, and guarantors of life-long careers for their workers.

On the contrary the “DD regime” implies that companies abandon the path of innovation through investment, and use their profits to distribute earnings to their shareholders and higher management. Since then, industrial relations suffered three major structural changes: 1) rationalization, 2) marketization and 3) globalization. Rationalization is linked to plant closures in the 1980s, marketization to the end of workers’ career in one company and the utilization of external labor markets to manage “human resources” (Doeringer y Piore 1985), and globalization is observed in the offshoring trend.

Initially those transformations could be understood as responses to changes in the economic context but while they became widespread, business performance began to be analyzed by indicators, such as earnings per share, so profits, instead of being invested to regain competitive advantage, turned to massive stock repurchases to manage stock prices in line with the recommendations of the “maximization of shareholder value” rule.

The effects of these changes in industrial relations are profound and clear. Not only did job creation stagnate, especially in blue collar jobs, but income distribution also became more unequal—with large compensation packages going to managers in the top percentiles. On an aggregate basis the growing gap between productivity and wages clearly depicts how American capitalism is utilizing its labor power. No wonder that, as a final result, GDP growth has decreased.

Sadly, as we shall see in section 2, although in Latin America there is no relevant stock market to fulfill the conditions of a “DD regime”—there are not a lot of publicly traded companies, as most corporations are family owned—its logic has existed here for as long as data exists. I would then propose relabeling the regime—only for emphasis purposes—as “downsize-and-distribute-and-fly” for the case of this region.

But let’s first review the wider picture where these transformations occur and especially how they affected Latin America.

New International Division Of Labor And The Labor Market

In a nutshell, towards the 1970s developed economies began to face economic difficulties: overproduction in conjunction with a slowdown in productivity growth caused by increasing difficulties to match a diversified demand with long production batches. In short, a depletion of the technical basis of Fordism. To push forward, companies innovated through telecommunications as well as automation.

Delocalization allowed companies to send labor-intensive production stages abroad, reducing costs with no substantial investment required, especially where outsourcing was implemented (and global value chains emerged). Automation, on the other hand, allowed several transformations on the factory floor. It reduced costs in small batch production through automatic setting of machinery, which further promoted outsourcing.

Those changes and raising unemployment in developed countries reduced their political power. This ignited a downward pressure on wages and employment quality in developed countries from which only the complex workers were spared. On the contrary, Asian countries began to actively participate in the world market, “taking advantage” of their massive population and low salaries to become export platforms for simple products or components.

However, the “new international division of labor” (Fröbel, Heinrichs, & Kreye, 1980) had no relevant effect on the role of Latin America. The region provided—and still does—primary products to the world market.1 Nevertheless, the intensified competition from Southeast Asia in low-tech manufactured products as well as Latin America’s productive lag with the developed world led Latin American countries to a long recession—called the “lost decade”. The manufacturing sector was dismantled and the region suffered a re-commoditization of exports. As expected, this had depressing effects on employment and wages throughout Latin American labor markets.

“Downsizing”: The Income Distribution

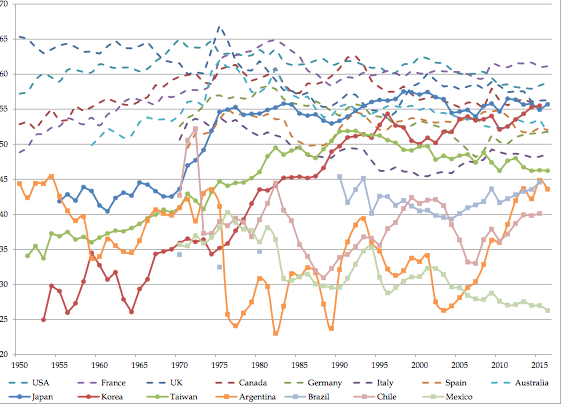

During the Fordism-welfare state era the wage share achieved high and raising levels in the industrialized world. As can be seen in Chart 1, most of these countries rose to levels around 60% by 1970s. For example the U.S. wage share rose from 57.2% in 1950 to an historical maximum of 64.9% in 1974. However, since then, most economies have experienced a downward trend. For the industrialized world the decline reaches some 5 percentage points until the 2000s, ending the period around 55% on average. Looking again at the U.S., its decline reaches 62% in 2000 and 58% by 2015.

Chart 1. Wage share of selected countries. 1950-20 Sources: Graña and Kennedy (2008) and national statistics institutions.

On the contrary, Asian economies linked to the transformation in the international division of labor show a different trend. Until the seventies for Japan—and the nineties in the case of Korea and Taiwan—the wage share rose quickly from its originally low levels, but then slowed down when reaching levels similar to the industrialized world and stagnated by late 1990 during the Asian crisis. For instance, Japan managed to push its wage share from 41% in the 1950s to 55% in the 1970s and touched its maximum of 57% in 1998. Korea, on the other hand, rose from 25% in early 1950s to 54% in 1996, a level it only surpassed in 2014.

Latin America is a special case. It presents a much lower wage share—it only occasionally reaches 50%—and shows extreme volatility. On top of that, it does not show important changes between both periods. For example, in Argentina’s case the wage share loses 10 percentage points between 1950 and 1965, then recovers until 1975, only to lose 15 percentage points in one year with the last military dictatorship in 1976. Then it recovers by 1994 and drops again by 2002, with the economic meltdown. Finally, it increases again in 2014. Chile shows a similar trend, from over 50% to 37% with Pinochet’s military coup, upwards towards 45% by early 1980s, a sharp decline by early 1990s, recovery by the end of the century and so on.

To sum up, the stagnation or decline—depending on the case—in the wage share from the mid-1970s onwards seems to be a worldwide phenomenon, with Asia joining the trend later on. Now, this similarity becomes less significant when evaluating both the magnitude and variability of the evolution of each country’s share of labor compensation. In short, from the analysis of the functional distribution of income it follows that Latin American countries, besides their own specific features, share common characteristics when compared to developed countries. Unfortunately, these characteristics are negative: a lower and more volatile wage share.

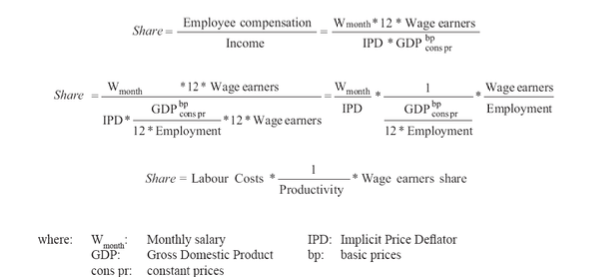

Possible explanations to that differential evolution between periods and countries can be found if we look closer into the way labor force is utilized. Elsewhere (Lindenboim, Graña, Kennedy, 2011) we mathematically decompose the wage share in its determinant factors: mainly labor cost and labor productivity.2

The multiple ways these factors evolve explain the divergence of developed and underdeveloped countries that share the same trend in functional distribution of income. For the developed world the reduction in the wage share has been the result of the increase in productivity not distributed to wage earners—which received only a small, highly unequally, distributed increase—while in the underdeveloped world the poor productivity results are contemporary with stagnation or reduction in real wages.

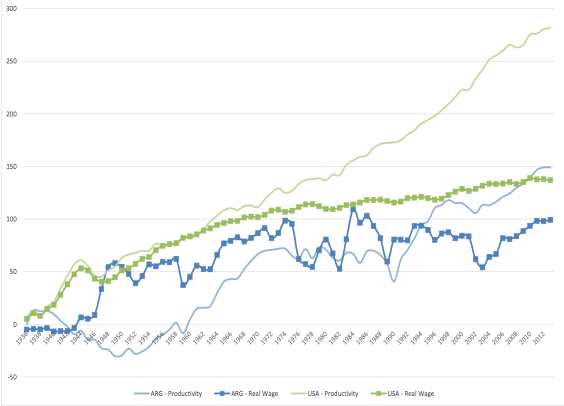

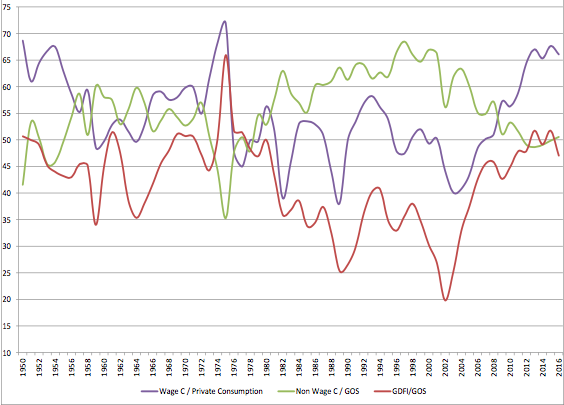

As shown in Chart 2, until the 1970s wage earners in the U.S. managed to obtain real wage increases in line with productivity. Still, since then the gap widened in line with Lazonick’s argument, with damaging consequences in terms of the raise in inequality. The different trend observed depends on a series of institutions present during the welfare state (mainly, but of course not only, labor unions and full employment) which were scraped during the neoliberal years. Yet, as sad as the American scenario is, let’s take a deeper look at Argentina (chart 2). While productivity has lagged behind—including several periods of total stagnation or reduction, such as 1940-1950 and 1975-1990—wages have had a terrible dynamic. Since mid-1970s real wages have dramatically declined in the long run.

Chart 2. Accumulative growth in real wages and labor productivity. Argentina and USA. 1936-2014 Source: Graña (2013)

Taking these two countries as expression of the developed and underdeveloped countries, respectively, we can say that the shared decline in labor compensation share of GDP is explained by different determinants. In the U.S. we see a redistribution of productivity gains towards high wages and surplus, while in Argentina we see a reduction of real wages and higher surplus. Thus, the impact of that change on the demand side of the economy will be significantly different.

“Redistribute”: Consumption and Investment

The other side of the distribution of income is how that income is allocated between final consumption and capital formation. In this section, we intend to show how changes in the wage share are followed by the transformation of aggregated demand between the two periods. To such end, we will mainly study the relationship between employee compensation and private consumption, on the one hand, and operating surplus and gross domestic fixed investment (GDFI), on the other3.

Sources: Authors estimations based on BEA.

Let’s begin with the U.S., the case analyzed by Lazonick (Chart 3). At first glance what stands out is, in line with the behavior of the variables related to functional distribution, the stability of the components of final demand. A second aspect is the level achieved by the data: employee compensation is barely below private consumption, which implies that the share of consumption absorbed by wages is remarkable. Nevertheless, the gap between employee compensation and private consumption has widened since the 1980s. Employee compensation has shown a slightly downward trend in contrast with private consumption, which has been increasing. Of course the difference between the two has been filled with debt, contributing to some extent to the 2008 crisis. Opposite to this, there has also been a rise in operating surplus coupled with a decline in investment. In short, exactly what Lazonick labelled under the DD regime. This also highlights, currently, the nonexistent connection between higher levels of surplus and investment promotion.

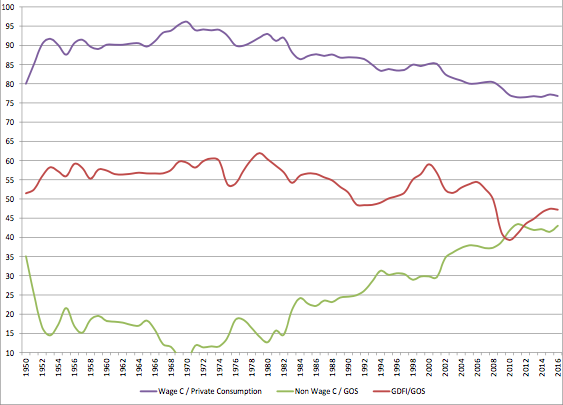

If we look at Latin America, the scenario is a little different. For Argentina, a key aspect stands out from the information shown in chart 4: the significant gap between the share of employee compensation and of private consumption in income which only in their maximum reaches 65% (while in the U.S. the minimum is 75%). Hence, the gap between operating surplus and investment.

However, these gaps show different levels depending on the historical period. Thus, it is clear that since the mid-1970s both “gaps” have grown and only reversed, partially, in the first decade of the 2000s. Certainly, there are significant particularities within this twenty-year period that deserve to be highlighted.

Chart 4. Wage, non-wage consumption and Gross Domestic Fixed Investment. Argentina. 1950-2016 Sources: Graña and Kennedy (2008)

From Chart 4 it follows that while at the beginning wage consumption represented about 70% of private consumption, its fall during the 1950s coupled with the stability of the latter resulted in a drop in the relation of both variables close to 50% in 1959. The other side of this process is the increase in the operating surplus, which does not translate into an increase in investment. This means that, although by the late 1950s there was a rise in the share of investment in income, such increase was not as high as that of operating surplus. There was, then, a growth of the portion of operating surplus that, either directly or indirectly, is used as a source of private consumption. In short, whereas by the middle of the 20th century, about half of the operating surplus was allocated to private consumption, by the early 1960s, this percentage increased to 60%.

As can be inferred from the chart, what occurred during the 1960s shifted these trends and the relations returned to their 1950s levels. After the outbreak of the military dictatorship and until the end of the 20th century, dynamics of the employee compensation–consumption relation were characterized by an extreme volatility of the wage share. Thus, the collapse in the wage share in 1976 translated into a reduction of the share of employee compensation in private consumption. Opposite to the slight increase in the share of investment observed in the 1950s, during the 1980s investment represented a share in GDP lower than that under the industrialization by import substitution (ISI) model. No major changes took place in this regard during the 1990s. The truth is that over the first years, there was a significant improvement (resembling that of the share of labor compensation) explained by the growth of both the share of private consumption absorbed by employee compensation and the share of investment in income. However, when looking at the entire period, such trends worsened, and the relations among aggregates returned to their initial levels. It is also worth noting that these were the years when the private sector was affected by a permanent deficit, as can be concluded from the chart showing that the sum of the share of Gross Operating Surplus (GOS) allocated, either directly or indirectly, to consumption or investment was well above 100%. As such, this is one of the reasons that explain Argentina’s need of permanent indebtedness which at last resulted in the collapse of the convertibility regime by the beginning of this century.

Following such debacle, the 21st Century showed promising signs: employee compensation has increased in parallel with stabilization of private consumption, which implies a rise in the percentage of employee compensation in private consumption, whereas the relative fall of operating surplus is accompanied with an increase in investment. Unfortunately, since 2011, Argentina’s economy has stagnated with high inflation and declining real wages which have hampered investment.

In short, during the neoliberal era, the fall in the wage share generated lower levels of investment. Then, until 2011, growing real wages and wage share pushed investment higher4. However, the “downsize” trend in Argentina is clear: in the best scenario only half of the surplus was reinvested, similar to levels in the U.S. today.

“Fly”: Balance of Payments Constraints

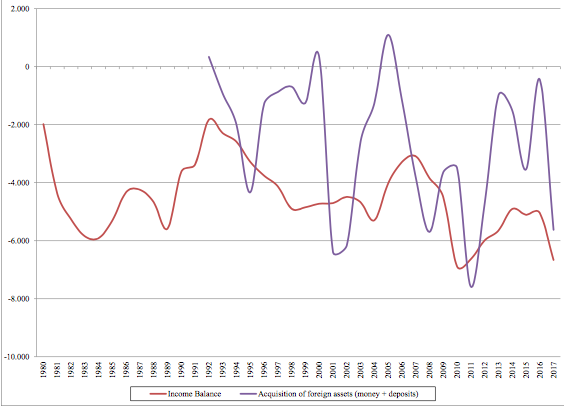

Finally, as increasing surplus is not going to investment, we need to understand where it is going. First, as we saw in Chart 4, half is going to consumption. In Chart 5 we show Argentina’s income balance (from the balance of payments data) and the acquisition of foreign assets by the private sector in 2017 dollars.

On average, Argentina faces a net income payment to non-residents of $4.5 billion dollars made up from profits and dividends from foreign companies as well as public and private foreign debt interest. And, due to the extreme volatility of the exchange rate, the purchases of around $2.6 billion in assets, particularly the purchase of U.S. dollars bills and deposits in foreign banks (mainly Uruguay, the U.S. or Switzerland). Those figures represent approximately 18% and 11%, respectively, of total exports in the last decade (2003-2017).

So, not only is higher surplus not funneled to investment but it is sent abroad, serving other countries’ accumulation process. This constitutes the “fly” component of the surplus allocation regime in Argentina.

Chart 5. Income balance and acquisition of foreign assets (money and deposits) Argentina. 1980-2017. Millions of US 2017 dollars. Sources: Kennedy and Sanchez (2018) and CEPALSTAT.

Concluding Remarks and Some Ideas for Future Research

As Lazonick (2014) states, in the long run, stagnation or decline in real wages—and in the wage share—has not conveyed any improvement to national economies because it eventually stagnated them, their investment and productivity. This, in time, is the basis for further deterioration of working class living standards.

If the American case is quite clear, the magnitude of the deterioration of Argentina’s living conditions since the seventies does not leave many doubts. The transformation in industrial relations has shifted distribution towards capital which has not been invested but distributed and sent abroad. It is clear that Argentina does not have a surplus production problem—nor is it lacking internal savings—but faces tremendous challenges in order to channel that surplus into productive investment. Sadly, economic policies intended to compensate the “fly” with the reception of Foreign Direct Investment and/or foreign public indebtedness only worsened the situation. This is the background of Argentina’s 2018 crisis.

Nevertheless, there is still a difference to be researched. Latin American countries seem to require greater and growing shares of surplus to sustain similar levels of investment. That is explained by the income balance, and the important role of foreign companies in the economy, and the acquisition of foreign assets—especially money and bank deposits, not foreign investment.

So the discussion regarding the reconstruction of an “RR regime” in Argentina would not only improve productivity and wages but also alleviate balance of payments constraints since most of the surplus is sent abroad.

In the complex international economic context we are facing, especially in the underdeveloped countries, we need to advance critical perspectives on the economic issues affecting working class living conditions. The further liberalization of the labor market is no solution to any of the problems observed in these pages. Lazonick’s paper is an important contribution in this area, to which this small comment only tries to further illustrate with the case of Argentina.

References

Doeringer, P. B., and Piore, M. J. (1985). Internal labor markets and manpower analysis. ME Sharpe.

Fröbel, F., Heinrichs, J., & Kreye, O. (1980). The new international division of labour: structural unemployment in industrialised countries and industrialisation in developing countries. Cambridge University Press.

Graña, J. M. (2013), Las condiciones productivas de las empresas como causa de la evolución de las condiciones de empleo. La industria manufacturera en Argentina desde mediados del siglo XX, PhD Thesis. http://bibliotecadigital.econ.uba.ar/?c=tesis&a=d&d=1501-1221_GranaJM .

Graña, J. M. and D. Kennedy (2008): Salario real, costo laboral y productividad. Argentina 1947-2006. Análisis de la información y metodología de estimación, Working paper Nº 12, CEPED, November (ISBN 978-950-29-1141-0).

Kennedy, D. y Sánchez, M. A. (2018). “El drenaje de divisas del sector privado y el renovado protagonismo del endeudamiento público externo en su sostenimiento. Un análisis del balance de pagos de Argentina. 1992-2018”. Forthcoming.

Lazonick, W. (2014) “Profits Without Prosperity: How Stock Buybacks Manipulate the Market, and Leave Most Americans Worse Off”, INET.

Lindenboim, J., Kennedy, D., & Graña, J. M. (2011). Share of Labour Compensation and Aggregate Demand, Working Paper Nº 203. UNCTAD

- 1. This includes Mexico. Since the debt crisis in the 1980s—and especially since the NAFTA agreement—it has shifted its economy towards exports to the American market. However it has remained stuck in low wage jobs competing with Asian economies for offshoring, with no innovative companies rising from it.

- 2. The starting point is, for sure, the result obtained from dividing employee compensation (including employees’ and employers’ contributions to the social security system) by total income, represented by Gross Domestic Product at basic prices (GDPbp), at current prices. The numerator results, in turn, from multiplying the average monthly salary (Wmonth) by the number of months and the total number of wage earners, while the denominator is equal to GDPbp at constant prices (cons pr) multiplied by the Implicit Price Deflators (IPD). In the second line, we multiply and divide the denominator by the number of months in a year and the total volume of employed people, and regroup. Finally, in the third expression, a specific name is assigned to each of the three components of the mathematical expression that follows.

- 3. Hence, we must describe two different essential characteristics. First, income aggregates considered as such are, in fact, not the most appropriate components since the estimates of the income of self-employed workers and employers (from their work activity) are included in operating surplus. Likewise, we should use disposable income estimates. In both cases, the difficulty arises from the fact that, at least in Argentina, such adjustments can only be made for a very short period of time. Thus, they should be disregarded when conducting a broader analysis as this one. Second, the nature of the comparative analysis requires an assumption regarding how employee compensation is allocated between consumption and savings. Here we assumed fully allocation to consumption and, thus, the remaining goods and services are acquired through operating surplus, whether acquired directly or through financing from surplus-related sources. The purpose of this assumption is not to reflect what actually happens, but just to portray the most favorable situation for wage earners. Any violation of the assumption would imply a lower share of labor compensation in private consumption and, thus, a greater consumption through operating surplus sources.

- 4. For other Latin American countries see Lindenboim et al (2011).