Greece’s view was rooted in the fact that its GDP has shrunk 30%, in sharp contrast to the bullish IMF forecasts made when the bailout began in 2010. That not only complicated the negotiations but has also left many Greeks struggling to survive. With its income falling to such low levels, the Greek private sector has been forced to dis- save for years i.e., living off the past savings, making it impossible for the country to pay back debt to foreign creditors.

The drop in the nation’s real output is on a par with that experienced by the US during the Great Depression from 1929 to 1933. The EU- and IMF-sponsored bailout program that started in 2010 was supposed to have produced a growing economy and a public celebrating the joys of recovery by now. In the event, however, it has done just the opposite, creating tremendous distrust of the EU and the IMF among local residents.

Yet not only has the EU refused to accept responsibility for this collapse in output, but it has argued for additional austerity and structural reforms. That, in a word, is why the negotiations made so little progress.

IMF slowly beginning to understand Greek economy

Which side is right? In a report titled ” Greece: Preliminary Draft Debt Sustainability Analysis” and published on 2 July, only days before the Greek referendum, the IMF admitted that Greece’s debt is “unsustainable” and that it needs to be rescheduled or reduced.

The IMF released this paper when it did because the US was worried the EU’s attachment to past policies had left it unable to acknowledge the need for a rescheduling or reduction of Greece’s debt. In a sense, then, the IMF was lending its support to Greece’s position.

Is Greece’s pain due to delays in structural reforms?

But a careful reading of this document reveals many problems as well. In particular, the IMF argues that “if the program had been implemented as assumed, no further debt relief would have been needed under the agreed November 2012 framework.”

This is essentially the EU argument that delays in implementing structural reforms were one of the causes of the difficulties Greece faces today. However, this argument is based on the highly unrealistic assumption that structural reforms can give a quick boost to GDP growth.

Structural reforms are by nature microeconomic—not macroeconomic—undertakings. The aim of measures such as deregulation is to prompt people to change their behavior and engage in new enterprises, eventually leading to a more vibrant economy. This process naturally requires a great deal of time.

Impact of Reaganomics was not felt until Clinton era

It was “Reaganomics” that first signaled the importance of structural reforms for the world. Although this policy was implemented in the first half of the 1980s, it did not lift GDP until Bill Clinton became president 12 years later.

In fact, the Republican Party responsible for it lost the 1992 presidential election to Mr. Clinton. His slogan, “It’s the economy, stupid!” overshadowed all the diplomatic successes of the Bush administration, which had ended the Cold War, overseen the collapse of the Soviet Union, and won the first Gulf War.

This experience demonstrated just how long it can take for structural reforms to have a significant macroeconomic impact. What I find inexplicable is that the IMF made the same mistake in Japan in 1997, suffered deep embarrassment as a result, and then went on to repeat this error yet again in Greece.

IMF has forgotten lesson of Japan’s failed fiscal consolidation

In 1997 the IMF did not recognize that Japan was in a balance sheet recession, in which the private sector refuses to borrow money even at zero interest rates, and demanded that the government implement fiscal consolidation measures. It also argued that the economic toll of those measures would be offset by a boost to the economy from the necessary structural reforms.

The Hashimoto administration boldly undertook six major reforms, among which was fiscal consolidation, which caused the economy to contract for five straight quarters (based on data available at the time) in what was reported to be the nation’s worst postwar recession. It also led to massive problems in the banking sector, with the Japanese economy eventually described as being in “meltdown” mode.

Having realized his mistake, Mr. Hashimoto changed course just eight months after raising the consumption tax rate and replaced fiscal retrenchment with fiscal stimulus. But it was already too late, and it was not until 1999, fully two years later, that the economy finally stabilized.

During this time the nation’s fiscal deficit ballooned 72% from 1996 levels in spite of tax hikes and spending cuts, and it took almost ten years for the deficit to return to its earlier level.

The lesson of Japan’s experience is that microeconomic structural reforms simply do not work when an economy faces the macroeconomic problem of a balance sheet recession. I find it extremely unfortunate that the IMF, which should have learned that lesson many years ago in Japan, went on to make the same mistake in Greece.

Fiscal multiplier becomes much larger during balance sheet recessions

IMF chief economist Olivier Blanchard admitted in a recent blog post that the negative multiplier effect of the fiscal retrenchment demanded by the IMF in Greece had been “larger than initially assumed,” but went on to insist this was not the only reason Greek GDP fell as far as it did (” Greece: Past Critiques and the Path Forward”).

But most of the other factors he cites—insufficient reforms, Grexit fears, low business confidence, weak banks, and inconsistent policies—are the result and not the cause of the economy’s meltdown, something that would have been obvious to anyone familiar with Japan’s experience in 1997.

The fact that the IMF underestimated the fiscal multiplier effect also shows that as of 2010 its economists were completely unaware of the economic malaise called a balance sheet recession. Over the years I have repeatedly made the point that during a balance sheet recession, when the private sector refuses to borrow despite zero interest rates, the multiplier effect of fiscal stimulus by the sole remaining borrower—government— becomes much larger than it normally is.

A number of key US policymakers who understood this, including former Fed chairman Ben Bernanke and current chair Janet Yellen, used the phrase “fiscal cliff” to warn about the dangers of fiscal consolidation during such a recession. Unfortunately, those warnings appear to have been lost on Mr. Blanchard and other IMF officials.

Greece faced two problems

Strictly speaking, Greece confronted two problems simultaneously. One was that GDP had been artificially boosted by a profligate fiscal policy carried out under the cover of understated deficit data. The other was a balance sheet recession triggered by the collapse of the massive housing bubble that resulted from the ECB’s ultra-low-interest- rate policy that lasted from 2000 to 2005.

The artificial increase in GDP (Mr. Blanchard correctly noted that Greek output was “above potential to start” in 2008) was something that other periphery countries like Spain and Ireland did not have to confront. A certain decline in GDP from such a level was inevitable as profligate fiscal policy was replaced by the necessary fiscal consolidation.

But what complicated matters in Greece is that in addition to the standard decline in GDP that results when profligate government spending eventually sparks a fiscal crisis, Greece was also in the midst of a balance sheet recession. The nation’s housing bubble and subsequent collapse were actually larger than those of Spain in terms of housing price appreciation and decline.

If all of Greece’s current problems were simply the price to be paid for past fiscal indulgence, the decline in output would have been much smaller than the actual 30 percent. But because the economy also faced a serious balance sheet recession, the fiscal consolidation measures implemented to address excess government spending caused GDP to fall by nearly 30%.

Admittedly, it would have been extremely difficult for anybody to balance the need to end the profligate fiscal policy while maintaining sufficient fiscal stimulus to keep the country in balance sheet recession from falling off the fiscal cliff. But now that it is where it is, the policymakers must find ways to get the economy to grow again.

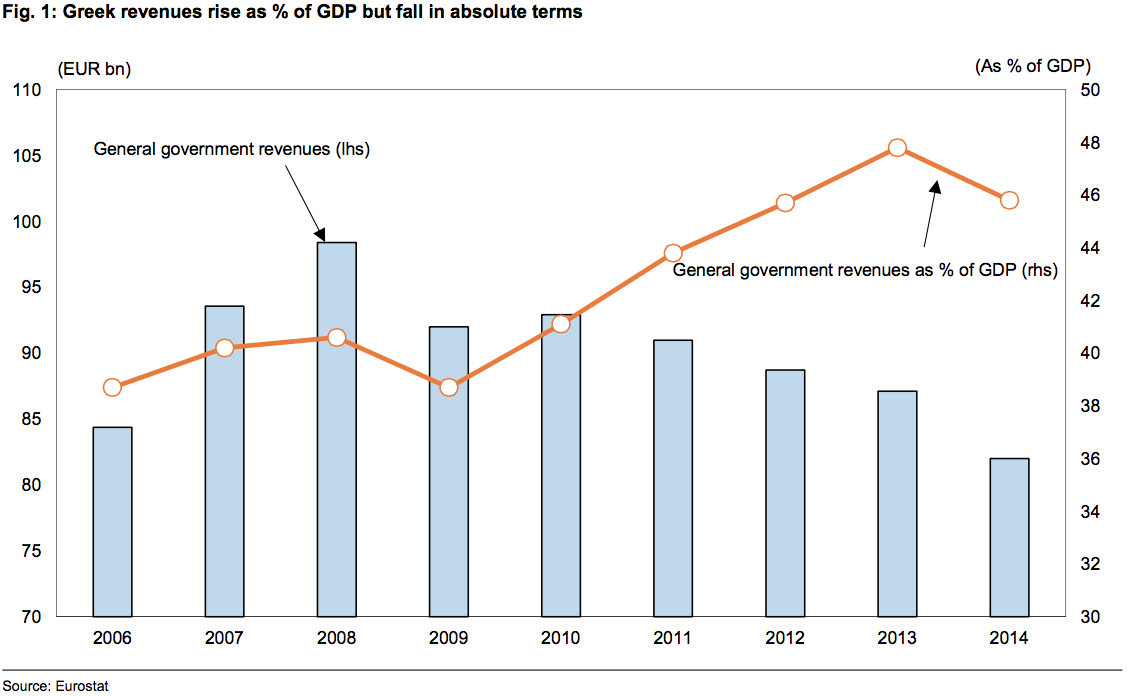

IMF and EU viewed revenues and expenditures as % of GDP…

There is also the possibility that the way data was presented by the EU and IMF further widened the perceptual gap between European lenders and the Greek public. Nearly all of the Greek analysis produced by the IMF and the EU has discussed matters relative to GDP, whereas Greek standards of living are linked directly to the absolute level of GDP.

When Jeroen Dijsselbloem, Dutch finance minister and eurozone group president, was in Japan earlier this year, he indicated that conditions in the European periphery, including Greece, had improved substantially, and that even if the Greek people elected a new government it would have no choice but to leave existing policies in place.

Materials published by the EU and the IMF show clear improvements in Greece’s fiscal deficits, with revenues growing steadily (see broken line in Figure 1) while expenditures remain under control. Having seen only these figures, one would be forgiven for concluding that current policies should be continued.

Thereby completely underestimating borrowers’ sense of crisis

But in fact Greek tax revenues have been steadily declining in absolute terms over the last five years (see bars in Figure 1) despite the numerous tax hikes and reinforcements to the tax-collection system implemented during that time.

The reason is that Greece’s GDP has plunged because fiscal consolidation was carried out during a balance sheet recession, resulting in a destructive deflationary spiral that has devastated the lives of ordinary Greeks.

While the nation may appear to be making progress when we view the data as a percentage of GDP, the raw data show an economy in collapse. This difference in perspectives widened the gap separating European creditors who thought everything is going well, and the Greek public who has been suffering serious declines in their standard of living. And this rift in perceptions was perhaps nowhere as evident as in the results of the national referendum on 5 July.

Rash privatizations aimed at raising money likely to fail

The IMF also overestimated to a grotesque degree the government revenues that would be generated by privatization. This is something that was also acknowledged by the Fund in the report noted above. Revenues actually derived from privatization in Greece have amounted to just 3% of initial assumptions, making the negotiations that much more difficult.

While the Greek government may be partly to blame for its less-than-enthusiastic attitude towards privatization, the European authorities appear to have forgotten a key lesson of German reunification, which is that rash privatizations carried out with the goal of raising as much money as possible tend to end in failure.

The West German government was convinced that selling the assets of state-owned enterprises in East Germany would generate enough income to fund all infrastructure investment required under reunification without raising taxes.

In the event, however, private-sector buyers took advantage of a cash-hungry government, and the revenues generated by asset sales amounted to only a fraction of initial estimates. West Germans faced a large tax hike as a result.

East German companies sold at fire-sale prices…

At the time I was personally interested in a certain manufacturing concern in the city of Dresden, then part of East Germany. I went so far as to visit the West German liquidator at the company headquarters and ask how much it would take to buy the company. At that time he was very confident the operation would fetch a high price, and the price he gave me was far beyond the reach of someone working for a Japanese company.

But several months after returning to Tokyo, I heard the company had been sold for a tiny fraction of the quoted price.

Since the West German government insisted on selling all assets within six months of bringing them to market, prospective buyers adopted the tactic of engaging in negotiations until the deadline loomed and then stepping away from the table. With just days to complete the sale, administrators were forced to dispose of assets at fire-sale prices.

While Thatcher government nurtured state assets into attractive businesses before selling

Faced with the urgent task of raising funds via privatization, the West German authorities also did not consider investing their own money and carrying out needed reforms to increase the value of East German enterprises before selling them.

In contrast, the privatization of British Telecom (BT) by the Thatcher government in the 1980s was considered a major success because the government took the time to implement reforms and make the company more attractive to private investors before putting it on the market.

In short, state-owned enterprises can be sold for high prices only if the government takes the time to execute the reforms and other measures needed to make them attractive to private-sector buyers. Rushed privatizations intended solely to raise money, like the ongoing efforts in Greece, are unlikely to produce favorable results.

The IMF acknowledged these problems in its recent report and substantially reduced its estimates of the revenues to be generated by the sale of state-owned assets, which suggests the Fund is finally starting to face reality.

Varoufakis an eloquent speaker

Another reason for the tortuous progress in the negotiations lies in the very different personalities and beliefs of the officials representing the two sides.

Former Greek Finance Minister Yanis Varoufakis is an excellent speaker of English. According to a British journalist who has covered the euro for more than 20 years, his command of the language is better than that of the other 18 eurozone finance ministers put together.

Moreover, he has an extremely quick mind, and it is not hard to envision him countering if not offending EU officials who believed in the basic soundness of existing policies by citing the sorts of issues noted above.

Market fundamentalist vs. bankruptcy lawyer

Mr. Dijsselbloem is an affable gentleman but is also a market fundamentalist who believes strongly in the virtues of abstinence, hard work, and self-responsibility. The British journalist noted above has gone so far as to label him a Calvinist.

He organized a bail-in when Dutch bank SNS Reaal collapsed, and as head of the Eurogroup he did the same when faced with the banking problems in Cyprus.

When I was at the New York Fed we were taught that bail-ins should be avoided if there was even a 5% probability of triggering financial instability. In contrast, Mr. Dijsselbloem pushed through bail-ins of SNS Reaal and the Cypriot banking sector—based on the principles of market fundamentalism and self-responsibility—in spite of a much higher probability that those measures would create turmoil among large depositors. This shows just how lucky the Dutch finance minister has been.

After all, former US Treasury Secretary Hank Paulson succeeded with a bail-in of California savings and loan IndyMac, which failed in July 2008, but just two months later sent the global economy into freefall with his decision to let Lehman Brothers fail.

Having had the opportunity to speak with both men, my impression is that any talks between the Dutch finance minister, who holds high the principle of self-responsibility and does not acknowledge the existence of an ailment called balance sheet recession, and the self-styled Greek “bankruptcy lawyer” who wants to get the economy moving again, were bound to degenerate into an unproductive ideological skirmish.

Dijsselbloem rejected Greek proposals out of hand

The Financial Times reported that in the last-minute negotiations before the referendum, Mr. Varoufakis asked IMF Managing Director Christine Lagarde whether the IMF would be willing to add to the EU’s proposal a formal statement that Greece’s debt would be sustainable under the rescue package.

This was a natural request given that the Greek government, by accepting the EU’s proposal, would cede all control of both monetary and fiscal policy to the EU, effectively preventing it from taking responsibility over the performance of its own economy.

But when Ms. Lagarde tried to respond to this very straightforward request, Mr. Dijsselbloem cut her off and brought the discussion to an end, saying Greece had only two choices left: take it or leave it.

The Dutch finance minister appeared to take the attitude that there was no need to listen to an impertinent debtor like Greece and refused to discuss the nation’s concerns about who would take responsibility if the measures proposed by the EU caused a further weakening of the Greek economy.

Inasmuch as Mr. Dijsselbloem entered the talks certain that Greece would accept the creditors’ demands because it had no alternative, I suspect he never had much intention of compromising. In the end, Greece’s rejection of the EU proposal and its decision to put the question to a national referendum probably came as a shock to the confident Dutch finance minister.

Agreement without debt waivers or growth forecasts is not a real solution

After achieving a resounding victory in the national referendum, the Greek government resumed its negotiations with the EU. It has been reported that the talks could resume only because France, taking a broader view of matters, persuaded the other creditors that history would not look kindly on them if they allowed the negotiations to break down.

On the debtor’s side, Mr. Varoufakis had to step down first probably because an agreement was impossible as long as he was on one side of the table and Mr. Dijsselbloem was on the other.

The compromise proposal submitted by Greece was almost identical to the EU’s previous proposal in that it contained neither debt waivers nor GDP growth forecasts. I suspect Greece felt bringing those issues up again would further reduce the chances of reaching an agreement.

In other words, I think Mr. Tsipras left those essential two items out of the new proposal because he decided it was critical to prevent further dysfunction in the nation’s banking system. Because of that decision, however, the agreement will resolve none of the fundamental problems facing the effectively bankrupt nation of Greece. Unless Greek growth picks up sharply, the country is likely to roil global markets again before long.

Reasons behind creation of AIIB

I would now like to discuss the Asian Infrastructure Investment Bank (AIIB), an institution whose longer-term impact on Asia cannot be ignored.

Originally the Obama administration sought reforms at the IMF and World Bank in an attempt to secure greater voting rights for China that were commensurate with its economic scale.

In its negotiations with European member nations, the US argued that Europe should acknowledge its reduced economic importance and relinquish some of its voting rights to China. Europe’s initially cool response to this proposal disappointed both the US and China.

Europe eventually agreed to the US plan to expand China’s voting rights. But then the US Congress voiced its objections. And that is where things stand today, leaving the issue unresolved despite the best efforts of the Obama administration.

AIIB a way around western opposition to IMF and World Bank reforms

In light of US and European opposition to IMF and World Bank reforms, few should have been surprised that China decided it made more sense to create a new institution than to stand around waiting for the status quo to change. Eventually it announced the creation of the AIIB.

Europe quickly declared that it would participate in the new institution. I see this as an attempt to smooth over relations with China after its earlier reluctance to allow the nation a more prominent role at the IMF.

The US administration, while arguing China’s voting rights needed to be expanded to make the IMF a truly global institution, ultimately faced opposition from the legislative branch of government. The end result was a significant loss of US influence with both Europe and China.

AIIB gives alternative to countries in need of help

The US sought to expand China’s voting rights and thereby maintain the IMF and World Bank’s central positions in the global economy because allowing the creation of a similar institution would give cash-strapped countries more than one “lender of last resort” to turn to.

Until now the IMF was the only choice for countries in need of financial assistance, which meant they had no choice but to accept the economic and fiscal reforms it demanded.

But if the IMF has competition, countries in need of help will most likely shop around for the institution offering the easiest terms, which means necessary reforms may be delayed.

China may also create an alternative to IMF

In its current form, at least, the AIIB has a different role from the IMF; it is designed to provide development funds, much like the World Bank or Asian Development Bank (ADB). Given that the World Bank and the IMF were created as a pair under the postwar Bretton-Woods regime, US officials may be concerned that China will come up with a sister institution to the AIIB that has an intended role similar to that of the IMF.

If the IMF’s rival is heavily under China’s influence, countries receiving its support will rebuild their economies under what is effectively Chinese guidance, increasing the likelihood they will fall directly or indirectly under that country’s influence.

Lending of development funds to the countries of Asia by a Chinese-led AIIB will also bring about an increase in the nation’s influence throughout the region. That would be of concern to the US, which has succeeded in extending its own influence in the area via the World Bank and IMF.

IMF and the US fundamentally misread Asian currency crisis

There is something to be said for the US argument that there should be only one refuge for economically troubled nations which takes responsibility for ensuring they carry out necessary reforms. However, that view is based on the underlying assumption that the US and the IMF will correctly diagnose the problems it encounters.

In reality, the US and the IMF completely misread the Asian currency crisis that began in 1997, and their errors caused tremendous damage to crisis-struck countries in the region.

The US and the IMF decided that the crisis, which started with a plunge in the Thai baht, was the result of structural problems in nations that had achieved economic growth with “developmental dictatorships.” They argued that these countries would see their economies stagnate for ten years or longer unless the structural issues were resolved.

They ridiculed the lack of transparency in legal and accounting systems, the prevalence of crony capitalism, and the lack of reforms to the region’s financial sectors. The “Washington consensus” at the time was that an Asian economic recovery would be impossible without reforms in all of these areas.

Malaysia, which not only rejected the IMF help, but also rejected the financial reforms sought by Washington and instead implemented capital controls, was declared a “hopeless” case by US officials.

Western investors caught up in bubble ignored warnings

In reality, however, the crisis was triggered not by structural problems in Asian economies but rather by the collapse of an Asian investment bubble in the west. Western investors were transfixed by the region and completely ignored all warnings about a bubble.

Just six months before the crisis erupted, a local economist at Nomura’s Singapore office issued a strongly worded report warning about an Asian bubble. When I tried to discuss her report with western investors, I was frequently brushed off with remarks to the effect that we were pessimistic only because we were viewing things from a (broken) Japanese perspective.

Ignorant investors flooded into Asia in search of quick returns

In the midst of this Asian boom, a joint private- and public-sector forum was held in Venice, Italy with the stated goal of reuniting Europe and Asia. The objective was to win back the promising region that had been lost to Japan and the US in the wake of World War II.

Given that objective, no one was invited from Japan, the US or Taiwan (the latter because there were guests from China). Someone made a mistake, however, and I received an invitation despite my ties to all three countries.

Having witnessed first-hand the feverish enthusiasm of western investors on Asia, I warned at the final joint session that the current successes of Japan and the US in Asia were the result of long years of trial and error, and that any investors planning to come to Asia should do their homework first lest they create a situation that hurts all involved. To my shock, my remarks elicited a heated response from the 500 people in attendance, with some claiming that I had been sent by the CIA and others that I was just trying to protect Japan’s interests in the region.

All I could do then was to say “good luck” and take my seat. But ultimately it was the collapse of this bubble, created by investors who knew nothing about Asia except that it was a certain road to riches that sparked the Asian currency crisis.

After the crisis erupted foreign investors started pointing fingers at the inadequacy of Thai bankruptcy law and Malaysian accounting standards, but their complaints only demonstrated that they were investing in those countries without the basic knowledge of these countries.

AIIB could become important tool in keeping US “honest”

Japan’s finance minister at the time, Kiichi Miyazawa, was quick to see to the heart of the matter and sounded out other nations about the creation of a Japanese government- led fund to help countries hit by the crisis, which had been triggered by the sudden outflow of foreign investment. But that plan was soon quashed by the US Department of the Treasury.

A crisis that could have been stopped was therefore left to run its course, with severe consequences for Asia’s economies and the lives of the people living there. It was this painful experience that later led Asian countries to pile up the massive quantities of foreign reserves described by western economists as a “savings glut.”

An indication of just how slipshod the US diagnosis of structural problems was at the time can be gleaned from the fact that Malaysia, declared the most hopeless case in the region, was the first to recover. Moreover, the process took only two years instead of the ten predicted by US authorities.

If China had come up with a plan similar to Mr. Miyazawa’s, it could have gone a long ways towards stabilizing the situation, given that China is unlikely to have acceded to US requests to stay out. The decision of many Asian countries to participate in the AIIB is probably due in part to a distrust of the US born during the currency crisis.

In that sense, I think the AIIB may come to play an important role in keeping America honest.

It is difficult to say at this point whether the AIIB will have a negative or a positive impact on the global economy. At the very least, however, I think the emergence of an international institution with a viewpoint different from that of western creditors will help enhance the quality of debate over emerging economies’ debt problems.