Ratner and Sim’s “Who Killed the Phillips Curve – A Murder Mystery”

“… the slope of the Phillips curve — a measure of the responsiveness of inflation to a decline in labor market slack — has diminished very significantly since the 1960s. In other words, the Phillips curve appears to have become quite flat.” Janet L. Yellen (2019)

A recent US Federal Reserve staff working paper written by David Ratner and Jae Sim (2022) has captured widespread attention, especially among economists, who, like ourselves, believe that a repeat of the anti-inflation policy scenario of the early 1980s of sharply raising central bank interest rates might prove inappropriate, if not catastrophic, as solution to dealing with the current inflationary environment. While inflation is hurting the poor disproportionally more because of their low incomes, a steep across-the-board rate hike may be a remedy that is worse than the disease, particularly since, as it has been well established (see, for instance, Storm 2022), we are not primarily facing with a demand-side inflation.

Indeed, not only might the inflation rate be quite insensitive to falling aggregate demand pressures, but sharp and persistent increases in interest rates could devastate many poor working households which would face the specter of increasing unemployment. This concern is amplified by the fact that, unlike the situation in the early 1980s, these poor households now tend also to be very heavily indebted as a proportion of their personal disposable incomes and may face even greater risk of insolvency both because of higher interest rates and because of the increasing unemployment (see Costantini and Seccareccia, 2020).

The US Fed as well as many other central banks internationally seem now to be united in favor of a steep hike in the Fed’s policy rate, as we witnessed with the most recent 0.75 percent jump on June 15. We are told, moreover, that there are many more increases to come since the Fed rate is, supposedly, still much below its “neutral” level. For a very recent plea in support of what may have been the “mother” of rate hikes in the United States, namely another “Volcker shock”, one has only to peruse the recent paper by Bolhuis, Cramer and Summers (2022) in which they suggest that, to get the current inflation rate down to align with the US Fed’s 2 percent inflation target, it would now “require nearly the same amount of disinflation as achieved under Chairman Volcker.” (2022, p. 1).

Given the nature of the current supply shocks affecting our weak Covid-battered economies, orchestrating another Volcker-style scenario by creating yet another deep recession is chilling. Besides, it would appear to be somewhat in conflict with the above assessment of former US Fed Chair Janet Yellen in 2019 as well as with the research of these two US Fed economists, Ratner and Sim, who suggest that the slope of the Phillips Curve is actually relatively flat and it has remained so for decades, for reasons that have little to do directly with the Volcker shock of the early 1980s.

While this was long established outside of the mainstream (for a review, see Seccareccia and Kahn 2019), numerous researchers in established circles have been writing recently about the flat Phillips curve. For instance, Engemann (2020), Del Negro, Lenza, Primiceri, and Tambalotti, (2020), as well as Del Negro, Gleich, Goyal, Johnson, and Tambalotti (2022), all recognize what had actually been obvious to many of us for a long time. The important implication is that, as Yellen (2019) recognized, the flatness of the relation implies an immensely high sacrifice ratio if pursuing a Volcker-style strategy (as recommended by Stanbury and Summers 2020), since it would require excessively high unemployment to get the inflation rate down by even a very small increment.

Yet, the conventional wisdom nowadays, which seems to willfully ignore this empirical evidence, still relies on some variant of the so-called New Keynesian Phillips Curve resting on the crucial assumption that the inflation rate responds to aggregate demand pressures as reflected in an economy’s rate of capacity utilization and/or the unemployment rate. If that were true, then this would advise the adoption of some “automatic formula” such as a return to some Taylor rule equation, as some conservative policy analysts are recommending, that would rest on an “inflation first” priority of central banking, which in the case of the United States would contravene its dual mandate.

However, evidence-based economics would suggest that the well-worn relation between unemployment and inflation does not actually exist, at least not in the form it is traditionally depicted by the mainstream. Since the 1980s, particularly during the disinflation era of the Great Moderation associated with falling unemployment and, even more so, when the US unemployment rate did fall significantly (as immediately after the Global Financial Crisis (GFC)), the inflation rate remained largely unresponsive and stayed close to the 2 percent inflation target even though the US civilian unemployment rate fluctuated a great deal from a double-digit level of 10 percent towards the end of 2009 to a low point of 3.5 percent just before the pandemic at the end 2019 and early 2020.

Apparently, for the mainstream, as it is now observable from recent central bank decisions to steer economies towards higher interest rates, what we have witnessed over the last four decades since the Volcker shock was some pure aberration. The current low unemployment rates, such as the US 3.6 percent unemployment rate in May, arising as economies recover from the pandemic, are now considered “unsustainable” low rates, even though the same central bank authorities deemed similar unemployment rates relatively sustainable in 2019 and early 2020. Now these low unemployment and high vacancy rates suddenly call for high interest rates and necessitate growing unemployment to prevent the acceleration of inflation.[i]

It is as if we have been abruptly thrust back to what were the confused arguments of the 1970s when economists like Milton Friedman had described those low unemployment rates resulting from the 1960s’ Keynesian expansionary macroeconomic policies as the cause of the accelerating inflation that had resulted during the 1970s. We now have reestablished a narrative with the same litany of arguments: governments have pumped too much money into the economy during the pandemic because of the massive deficit spending and because of the very loose monetary policy of quantitative easing and excessively low interest rates. These have now driven unemployment rates to unsustainably low levels that can only generate accelerating inflation. To prevent a galloping inflation, high interest rates have become an imperative.

The US Fed working paper on Kalecki’s economics, dated September 2021, but which appeared only recently, is a breath of fresh air. Ratner and Sim (2022) claim that the Phillips curve in the United States and the United Kingdom has been almost flat since the 1980s because of the significant erosion of the bargaining power of workers. This began during the Reagan and Thatcher years, and which was especially reflected in declining union density rates over the last four decades. Thus, the supposed triumph over inflation for roughly four decades, until the surge during this last year of Covid-19, cannot be fully attributed to the conduct of monetary policy by the US Fed and the Bank of England. The Fed working paper, therefore, casts serious doubt on the mainstream narrative, which posits that the policy of the late Fed Chairman Paul Volcker of large hikes in interest rates was responsible for taming the 1980s inflation. If the Volcker shock was actually not what caused the long-term change in the dynamics of the inflation rate since the 1980s, and until the current Covid-19 crisis, then what was the culprit that flattened the Phillips curve?

The main takeaway of their paper is clear: interest rate hikes could have helped but it was rather the class conflict — particularly the offensive against the working class — that stood behind the inflation debacle of the Great Moderation, which had long-term consequences. Putting it that way, this could sound quite subversive to many mainstream economists. Indeed, as Nick Peterson (2022) writes in the Financial Times: “coming from deep inside the Fed this is near heresy. After all, central banks have naturally long been in thrall to theories that made them the heroes of the story.”

However, the authors recognize that the ideas are not new at all. In an unusual display of openness to heterodox ideas, Ratner and Sim give credit to post-Keynesian economics, and especially to the famous Polish economist Michał Kalecki (1943, 1971), who was a contemporary of John Maynard Keynes and co-discoverer of the principle of effective demand, apart from advancing several of Keynes’ contributions. Indeed, Kalecki, along with such less well-known writers as Henri Aujac (1950), was the founder of the view that inflation is primarily an expression and the outcome of class conflict (or conflicting claims) over national output by the way firms price their products vis-à-vis workers’ wage setting.

As a tribute, the authors replace the New Keynesian Phillips curve with a more general “Kaleckian” Phillips curve, as they call it, in which they include an exogenously-determined parameter impacting on its slope that reflects the degree of bargaining power between workers and firms.

We believe that their main contribution is the introduction of the “Kaleckian” Phillips curve to the canonical Two-Agents New Keynesian (TANK) model with monopolistic competition (in this case, the two agents are workers and firms). This tweak implies that, apart from the usual bargaining over wages, there would be bargaining over the product price (or monopoly rents). Workers through labor unions would try to keep the markup as low as possible so that wages and the labor share would be larger, whereas firms would try to do the opposite. The degree of bargaining power would determine the winners and losers in the distribution of monopoly rents. It follows that the “Kaleckian” Phillips curve explains why the inflation and unemployment rates have been relatively low since the 1990s — without considering the recurrent crises and the most recent inflationary episode — because the bargaining power of workers has been extremely limited.

Apart from that, the model has additional interesting aspects, of course, within the obvious constraints of the DSGE framework, which, to many of us, is problematic (see Storm 2021). For instance, the fight over the share of monopoly rents involves two different and opposed channels that impact the level of output and the NAIRU. When the degree of bargaining power is roughly balanced, small increments in the bargaining power of firms have a very positive impact on output and employment since the investment incentives are higher, whence the job creation channel dominates. In contrast, when the bargaining power of firms is particularly high, firms prefer to increase their profits by selecting the highest markup at the expense of output and job creation; thereby the markup channel dominates. But there is no reason why the degree of bargaining power would vary over time because it is an exogenous parameter. Thus, within the model, involving the standard DSGE assumptions of “rational expectations,” a steady decline in the bargaining power of workers is unexplained (and conceivably “irrational”) from the point of view of labor unions since this simply goes against workers’ interests.[ii]

On the other hand, the authors contrast the “Kaleckian” Phillips curve with respect to the New Keynesian Phillips curve in response to a positive demand shock. The results are different because, in the former, the slope of the curve changes with the degree of bargaining power between firms and workers whereas, in the latter, it remains constant regardless of the degree of bargaining power. That is because in both models there is bargaining over the wage but, in the “Kaleckian” case, there is also bargaining over the markup and product price. As a result, a positive demand shock in the “Kaleckian” model would amplify the impact on inflation and diminish it on employment.

Finally, the paper presents some time-series and cross-sectional evidence for the United States and the United Kingdom that leads to a significant positive relationship between the bargaining power of workers and the slope of the Phillips curve, which would be supporting their model. Nevertheless, the econometric evidence does not discard the possibility that the respective monetary policies themselves did have a significant impact as well. In the authors’ own words: “The estimation results point to a possibility that both the post-1980s disinflation and the concurrent flattening of the Phillips curve owe as much to the labor market institutions of these two countries as to the monetary policies of these two countries.” (Ratner and Sim 2022, p. 26).

We appreciate their research findings and find ourselves broadly in agreement with their conclusions about the flatness of the Phillips curve. This is a view, however, that is somewhat inconsistent with the current hawkish position of the US Fed that seems now to believe that the short-run Phillips curve is more hyperbolic rather than flat, otherwise its whole current strategy of wringing the inflation out of the US economy through strong doses of higher interest rates would be futile, since we are not experiencing primarily a demand-side inflation. We have already argued above and have also discussed elsewhere (see Seccareccia and Khan 2019, Lavoie and Seccareccia 2021, and Seccareccia 2022) that the Phillips curve is quite flat for a very large relevant range of the unemployment rate.

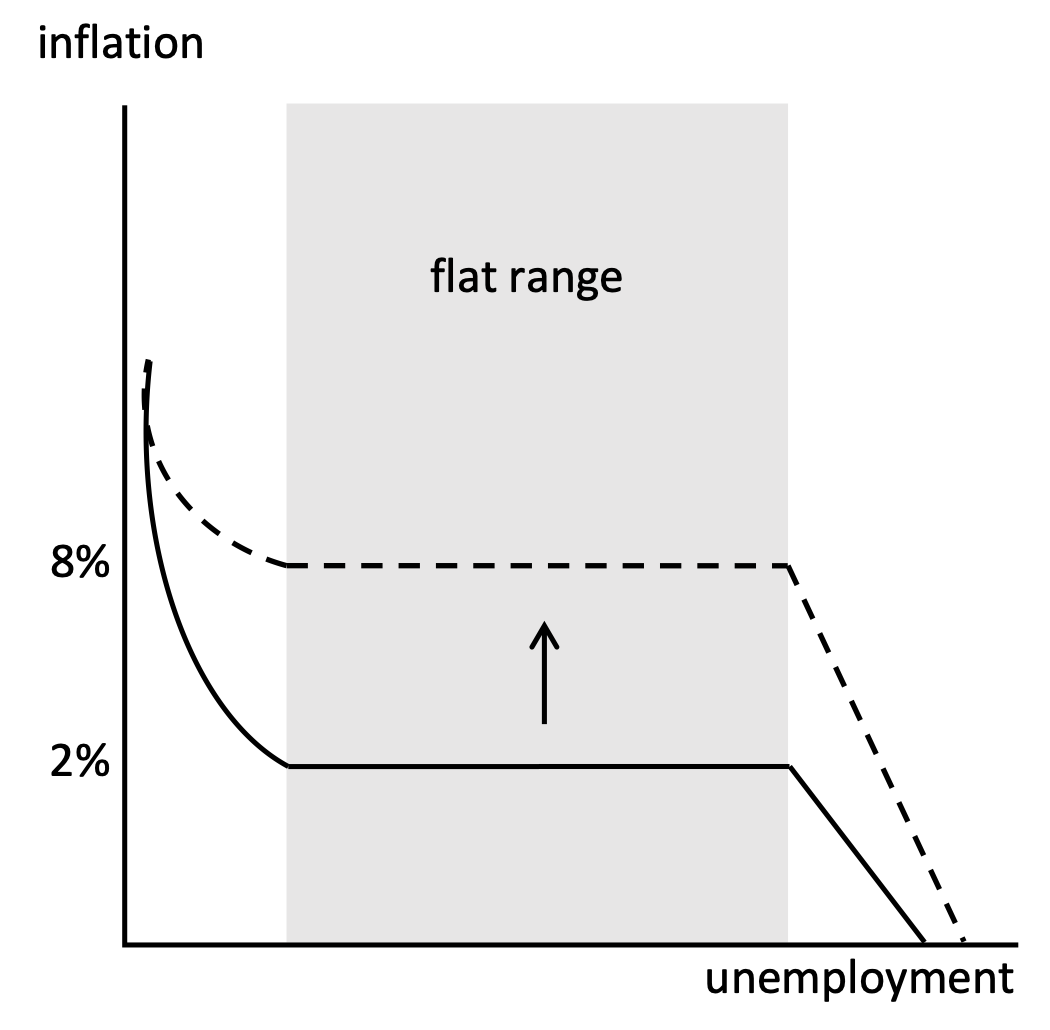

As shown in Figure 1 below, cost factors, such as international oil price shocks, can shift the whole curve upwards, but if we are in the broad flat range, the central bank cannot act on it to influence the current inflation unless it believes that the economy has reached the extremities of the curve (in this case at the extreme left). Indeed, as US Fed chair Jerome Powell has quite candidly admitted: “What [the Fed] can control is demand, we can’t really affect supply with our policies…so the question whether we can execute a soft landing or not, it may actually depend on factors that we don’t control.” (Jerome Powell (2022) cited in Shapiro (2022)). Although the paper by Ratner and Sim does not look at very recent evidence during the pandemic, the burden of proof rests on central banks to show (rather than assume) that the current inflation is primarily a demand-side one, where the economy now finds itself within the extreme left in the upward-sloping section of the Phillips curve.[iii] If the economy is still in the relatively flat range, and that all that has happened recently is that supply-side shocks have shifted the whole flat range of the curve to a higher range as firms have been marking up these sustained cost changes, then these interest rate hikes will merely slow down the economy with minimal impact on the overall inflation rate. [iv]

Figure 1: Phillips Curve with a Significant Flat Range

While appreciating much of what Ratner and Sim analyze, we do, however, have some further concerns. Up to this point perhaps anyone with some knowledge of Kaleckian economics would notice that the Ratner and Sim model is far from representing the core ideas of the celebrated Polish economist. First, the model sticks to Say’s Law in the sense that it is saving that determines investment as in a pre-Keynesian loanable funds world. Kaleckian economics, on the contrary, sticks to the Keynesian principle of effective demand, whereby investment is autonomous, saving is endogenous, and the rate of interest depends on central bank policy (Kalecki 1943). Thus, profits are determined by consumption out of profits and investment, assuming workers spend all their income. This important theoretical departure from New Keynesian economics led to the famous Kaleckian aphorism (wrongly attributed to Kalecki): “capitalists earn what they spend, and workers spend what they earn.” (Lavoie 2022, p. 332).

Furthermore, the technology assumed by the authors’ model depicts constant returns to scale and diminishing returns to labor and capital, implying increasing marginal costs. By contrast, Kaleckian models assume constant marginal costs (up to full capacity) and so “higher real wages will not necessarily entail a reduction in production and employment” (Lavoie 2022, p. 314) such that the labor demand curve would be upward sloping. Ultimately, output is constrained by demand both in the short and long run. In contrast, the model of Ratner and Sim (2022) entails that steady-state output and employment is supply constrained by the level of saving, in turn determined by workers’ and firms’ preferences and a natural rate of interest that would pin down the value of the NAIRU.

Finally, we suspect that Kaleckians might be uncomfortable in calling the paper’s curve a “Kaleckian” Phillips curve. While it is true that the degree of bargaining power affects the Phillips curve in the authors’ model, the former is just a parameter exogenously determined, i.e., given the bargaining power of workers, the NAIRU and the natural rate of interest are pinned down and are unique, which is inconsistent with Kaleckian economics. Kaleckians, and more generally post-Keynesian economics, explicitly reject the existence of a NAIRU or a natural rate of interest. Therefore, a genuine Kaleckian Phillips curve would portray a horizontal segment that might depend on the bargaining power of workers, among other institutional factors but, as remarked by Kalecki (1943) in his “Political Aspects of Full Employment”, the bargaining power depends on the rate of employment and monetary policy, which is itself influenced by class conflict as well.

As we have already discussed above, the shape of a genuine Kaleckian/Post-Keynesian Phillips curve could depict a flat part but surrounded by downward-sloping segments or even an upward-sloping segment given by a hypothetical full-employment situation, as suggested by Seccareccia and Khan (2019). It is also very likely that the trends in the unemployment rate have affected the bargaining power of workers and the conflict over the distribution of income (Seccareccia and Matamoros Romero 2022). Last, partly as a result and since monetary policy is embedded in the class conflict, the Volcker shocks, and the subsequent high-interest rates policies — up to the financial crisis of 2008-09 — should be seen as part of the policies that eroded the bargaining power of workers and not as an independent phenomenon, as Ratner and Sim seem to posit. Central banks would themselves be taking sides in the class struggle.

But there is more going on than just the conflict between workers and firms. As suggested by Seccareccia and Lavoie (2016) and Seccareccia and Matamoros Romero (2022), there are also the rentiers, much analyzed by Keynesian economists who may have conflicting interests that have long been understood by post-Keynesian economists. Rentier interests have played an important role in what occurred historically. Owing to the growing importance of the financial sector, we have seen how the rentier perspective hijacked monetary policy through the adoption and framing of inflation-targeting monetary policy regimes since the last major inflation of the 1970s and 1980s. In fact, much of the current political pressure to revive the “inflation first” monetary policy commitment through some formal adoption of an official Taylor rule reaction function in the United States is part of this rentier revival in the macroeconomic policy agenda that waned after the financial crisis.[v] Ratner and Sim (2022) are completely silent on this matter of rentier interests, which has been also of great concern to many non-mainstream economists and which transcends the traditional two-class analysis discussed in their paper.

References

Aujac, H. (1950). Une hypothèse de travail : l’inflation, conséquence monétaire du comportement des groupes sociaux. Économie appliquée, 3(2) (avril/juin), 279-300.

Bräuning, F., J. L. Fillat, and G. Joaquim (2022), Cost-Price Relationships in a Concentrated Economy, Current Policy Perspectives, Research Department, Federal Reserve Bank of Boston, (May 23), 1-9, https://www.bostonfed.org/publications/current-policy-perspectives/2022/cost-price-relationships-in-a-concentrated-economy.aspx .

Bolhuis, M. A., J. N. L. Cramer, and L. H. Summers (2022), Comparing Past and Present Inflation, National Bureau of Economic Research, Working Paper 30116 (June).

Costantini, O., and M. Seccareccia (2020), Income Distribution, Household Debt and Growth in Modern Financialized Economies, Journal of Economic Issues, 54(2), 440-49, DOI 10.1080/00213624.2020.1752537

Davidson, K. (2016), Yellen Objects to Proposed Rule for Rate Formula: Discussion of Legislation Opposed by the Fed Crops up during Wednesday’s Testimony, Wall Street Journal (February 10), https://www.wsj.com/articles/yellen-objects-to-proposed-rule-for-rate-formula-1455124921?mod=article_relatedinline

Del Negro, M., A. Gleich, S. Goyal, A. Johnson, and A. Tambalotti (2022), Disinflation Policies with a Flat Phillips Curve, Liberty Street Economics, Federal Reserve Bank of New Your (March 2), https://libertystreeteconomics.newyorkfed.org/2022/03/disinflation-policies-with-a-flat-phillips-curve/

Del Negro, M., M. Lenza, G.E. Primiceri, and A. Tambalotti, (2020), What’s Up with the Phillips Curve?, Brookings Papers on Economic Activity, (Spring), 301-357; https://www.brookings.edu/wp-content/uploads/2020/12/DelNegro-FINAL-WEB.pdfeven

Engemann, K.M. (2020), What Is the Phillips Curve (and Why Has It Flattened)?, Federal Reserve Bank of St. Louis, (January 14), https://www.stlouisfed.org/open-vault/2020/january/what-is-phillips-curve-why-flattened

Kalecki, M. (1943). Political Aspects of Full Employment. The Political Quarterly, 14(4), 322–330. https://doi.org/10.1111/j.1467…

Kalecki, M. (1971). Selected Essays on the Dynamics of the Capitalist Economy 1933-1970, Cambridge University Press.

Konczal, M., and N. Lusiani (2022), Prices, Profits, and Power: An Analysis of 2021 Firm-Level Markups, Working Paper, Roosevelt Institute (June), https://rooseveltinstitute.org…

Lavoie, M., and M. Seccareccia (2021), Going Beyond the Inflation-Targeting Mantra: A Dual Mandate, Max Bell School for Public Policy, McGill University (April 23): 5–40, https://www.mcgill.ca/maxbells…

Lavoie, M. (2022). Post-Keynesian Economics: New Foundations (2nd ed.) Cheltenham, UK: Edward Elgar Publishing. Retrieved Jun 10, 2022, from https://www.elgaronline.com/vi…

Peterson, N. (2022). Class War > Rate Hikes. Financial Times (June 7), Retrieved June 9, 2022, from https://www.ft.com/content/4e3…

Powell, J. (2022), Inflation, Soft Landings and the Federal Reserve. Interview by Kai Ryssdal, Marketplace Business News Podcast, NPR, (May 12). Audio, 27:38; https://www.marketplace.org/sh…

Ratner, D., and J. Sim (2022). Who Killed the Phillips Curve? A Murder Mystery, Finance and Economics Discussion Series 2022-028. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS….

Seccareccia, M. (2022), Can the Pursuit of Fiscal and Monetary Policies Achieve a Meaningful Full-Employment Objective without Inflation? Learning from the Canadian Historical Experience, including the Recent COVID-19 Crisis, Paper presented at the XXII Seminar of Fiscal and Financial Economics, Public and Private Credit: National and Global Experiences in the Current Crisis, National Autonomous University of Mexico, Mexico City (March 30).

Seccareccia, M., and M. Lavoie (2016), Income Distribution, Rentiers and their Role in a Capitalist Economy: A Keynes-Pasinetti Perspective, International Journal of Political Economy, 45(3), 200-223, DOI:10.1080/08911916.2016.1230447

Seccareccia, M., and N. Khan (2019) The Illusion of Inflation Targeting: Have Central Banks Figured Out What They Are Actually Doing Since the Global Financial Crisis? An Alternative to the Mainstream Perspective, International Journal of Political Economy, 48(4), 364-380, DOI: 10.1080/08911916.2019.1693164

Seccareccia, M., and G. Matamoros Romero (2022). Is There an Appropriate Monetary Policy Framework to Achieve a More Equitable Income Distribution or Do Central Bank Mandates Really Matter? Interest-Rate Rules versus a Full-Employment Policy, Journal of Economic Issues, 56(2), 498-507, DOI 10.1080/00213624.2022.2061831

Shapiro, A. H. (2022), How Much Do Supply and Demand Drive Inflation?, FRBSF Economic Letter, Federal Reserve Bank of San Francisco, (June 21), https://www.frbsf.org/economic…

Stansbury, A., and L. H. Summers (2020), The Declining Worker Power Hypothesis: An Explanation for the Recent Evolution of the American Economy, National Bureau of Economic Research Working Paper No. 27193 (October), https://www.nber.org/system/fi…

Storm, S. (2021) Cordon of Conformity: Why DSGE Models Are Not the Future of Macroeconomics, International Journal of Political Economy, 50(2), 77-98, DOI:10.1080/08911916.2021.1929582

Storm, S. (2022), Inflation in the Time of Corona and War, INET Working Paper No. 185 (May 30).

Yellen, J. L. (2019), Former Fed Chair Janet Yellen on Why the Answer to the Inflation Puzzle Matters, Brookings Report (October 3), https://www.brookings.edu/rese…

[i] In fact, the model by Ratner and Sim (2022, p. 17) predicts that a low inflation-low unemployment environment would be consistent with high vacancy rates. This is because labor bargaining power would be particularly low, thereby firms would have much higher incentives to increase job postings. Hence, following the model, the current high vacancy rates in the United States would be in line with a low labor bargaining power, and the inflation surge would be unrelated to any supposed tightness in the labor market.

[ii] We are grateful to Servaas Storm for raising this point. Also, to be fair, Ratner and Sim (2022, p. 16) recognize that the degree of bargaining power is made exogenous for simplicity, but assert it could potentially be made endogenous in a more sophisticated DSGE model, despite being a challenging task. However, we have serious doubts that doing this in a DSGE framework would retain the Kaleckian insight that a long-run fall in the bargaining power of workers would be affected by monetary policies that are biased against workers’ interests.

[iii] A recent paper by Shapiro (2022) defending the Fed’s policy of raising rates suggests that, perhaps, about one third of the recent inflation arises purely from the demand side while the rest would be either “ambiguous” or of a supply-side nature, or to quote Shapiro (2022): “These results showing that factors other than demand account for about two-thirds of recent elevated inflation …” In our opinion, this methodology is somewhat flawed and highlights why understanding Kalecki’s model is important. Despite the complicated technique based on rolling regressions to generate predicted monthly values for quantity and price, his theoretical framework seems to rest on an elementary textbook division whereby, if the actual monthly values of price and quantity are both above or both below their predicted values, then it’s a “demand-driven” phenomenon, while if the values are of opposite signs, this would be a “supply-driven” outcome, analogous to the elementary textbook demand/supply analysis. Unfortunately, this binary distinction could easily confound a cost-push inflation arising from increasing business markups with a pure demand-side inflation, as might be the case in recent times as the economy is recovering from the pandemic, where presumably price and output would be moving upward in tandem vis-à-vis their predicted values as well as the price markup! By contrast, Ratner and Sim (2022) allow for this Kaleckian markup effect in their specific model. Many recent studies suggest that rising markups are ubiquitous and have been rising also because of growing industrial concentration. See, for example, Bräuning, Fillat, and Joaquim (2022), Konczal and Lusiani (2022), and Storm (2022).

[iv] This flat range is certainly well recognized at the US Fed, as Yellen (2019) points out about the importance of the “sacrifice ratio” along the flat range: “It’s important to point out, however, that a flat Phillips curve has a downside, which is that it raises the so-called “sacrifice ratio.” The sacrifice ratio measures the cost in terms of higher unemployment to lower inflation should it rise too high. With a flat Phillips curve, it’s necessary for monetary policy to create a good deal of slack in the labor market to return inflation to levels consistent with price stability. … Finally, even if the Phillips curve is quite flat over some range, it’s conceivable that it could become a lot steeper if unemployment is pushed to very low levels: that is, it may be nonlinear at very low unemployment. There is some evidence of such nonlinearity, so it’s a significant policy concern.”

We believe that this describes reasonably well what has been said for years by post-Keynesian economists. What at the US Fed may not be understood is that flat anchor is not governed only by inflationary expectations impacting on wage growth, but also other supply-side/costs that can shift the whole curve as shown in Figure 1 above.

[v] This well-known Taylor rule is discussed, for instance, in Seccareccia and Kahn (2019), and was rejected by former chair Janet Yellen for possible adoption at the US Fed (see Davidson 2016). This pro-rentier “rule” rests on three elements: (1) a “natural rate” of interest that central banks would sustain over time, (2) a deviation between current inflation and the 2% inflation target, and (3) an output gap. Since the output gap is of concern to policy makers uniquely as a predictor of future inflation based on some standard Phillips Curve model, then monetary policy becomes focused solely on how to get the inflation rate back on target through interest rate policy, while preserving a stable positive real interest rate over time. As we have said, this pro-rentier Taylor rule policy framework would actually contravene the US Fed’s dual mandate since the so-called output gap in the equation is only of concern to policy makers for inflation-fighting purposes. Instead, the minimization of the unemployment rate towards a full employment level is not directly of any concern since it is not an independent policy objective within the Taylor rule framework unless one defines the NAIRU as full employment, which it is not.